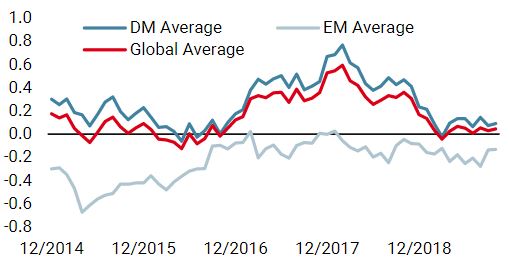

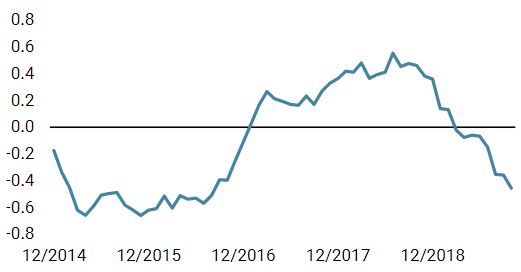

The Eurozone has been a source of concern to us for 20 consecutive months in light of alarming signs of broad-based deceleration. A lack of clear governance made Europe, and more particularly the Eurozone, the weakest link in the investment world, in our view. But things seem to be changing. We see (very) early signs of macro stabilisation and consumption growth looks firm. We also see too much pessimism in markets as these first signs of improvement surface. With the ECB’s new President pushing for more fiscal spending, an extremely low euro and a lower exposure to the trade war, we think European growth assets could become more appealing. We need to strengthen our faith here a little more, but we have already started reducing our defensive positioning. We have been worried about the European situation for almost two years now. Our European Growth Nowcaster reached a peak in January 2018, just like it did for the rest of the developed world. However, unlike the rest of the world, it has collapsed since then. The indicator was at 0.67 in January 2018, where zero represents growth in line with potential. From this extreme level, the fall has been sharp: by March this year, the indicator had plunged to -0.19, very close to our -0.3 recession threshold and indicative of growth being below potential. Historically, when an economy reaches that threshold, its GDP has typically started to contract: Canada and South Africa are recent examples. The Eurozone managed to remain above this threshold but this -0.19 level is concerning. Our Growth Nowcaster has only been lower 30% of the time: a clear sign of growth being at risk. Moreover, the fall was not just sharp, it was also broad-based, unlike other developed economies. Since February 2018, on average, across the 41 data series used to create our Eurozone Growth Nowcaster incorporating seven economic dimensions (such as consumption, production expectations, housing or investment), 65% of them were declining. In March 2018, this number increased to 81%, with its 30-year historical maximum at 90%. Little wonder we started feeling nervous about the European economy, with 2011 still fresh in our minds. There are early signs that things are finally stabilising, an unexpected but welcome breather after almost two years of economic slowdown. Four key elements are potentially turning this very bearish story into something more positive:“Got to Have Faith” – Europe, 2004

What’s Next?

Heading Towards 2011?

Macro: A New Hope

The final element we are seeing is excess pessimism across markets, which has caused hedging assets to become extremely expensive. This is even more the case for European assets.Sentiment/Valuation: Bearish Sentiment Overly Priced

Sentiment is negative now that markets have recovered from their Q4 2018 collapse, driving people to take profits and to hedge themselves. The equity skew is currently as high as in January 2018: a clear sign that investors are seeking protection. Also, portfolio positioning in European equities has steadily decreased, as shown when studying the beta of multi asset portfolios to US and European stocks. If investors only recently decreased their holdings in US stocks (basically since July 2019), they gave up on European equities in January 2018 and have steadily reduced their investments there since then (as measured from the beta of a pool of multi asset funds to the S&P 500 and to the Eurostoxx index).

We see this situation as more of an issue among regional equities where valuations look uneven. According to our estimates covering a large spectrum of valuation metrics such as price-to-book, earnings yield or sales-to-book ratios, there is now a large difference between the very expensive US stocks (above their 80th historical percentile) and the very cheap Japanese and emerging stocks (30th percentile).

Interestingly, European stocks are sitting in a higher range without being as expensive as US stocks (70th percentile). Historically (1990-2018), when they reached these values in terms of expensiveness, European stocks delivered a positive performance in the following three to six months. In addition, most of the metrics we use are based on forward-looking earnings/sales, which are currently very pessimistic for European stocks. Should these numbers improve in the upcoming earning season, these valuations could actually be even lower than where they stand today.

In our opinion, the case for European assets is still early, and we have only lightened our bearishness on them for now, gaining an exposure to global equities rather than regional ones. However, European equities contain a larger portion of value stocks and a macro bottoming in Europe could ignite a value rally that could help European stocks to outperform. If the macro situation does improve, this could become an interesting investment theme to add to our constructive positioning in growth assets.

Got to Have Faith

Our medium-term view is currently more constructive, as we are still overweight growth assets and underweight real assets. Given the current cost of hedging, we are using forex-based strategies exposures to hedge ourselves against adverse market conditions. Over the month of October to date, the Uni-Global – Cross Asset Navigator fund lost -0.63% versus 0.14% for the MSCI AC World index and -0.46% for the Barclays Global Aggregate (USD hedged). Year-to-date, the Uni-Global – Cross Asset Navigator has returned 9.51% versus 16.36% for the MSCI AC World index, while the Barclays Global Aggregate (USD hedged) index is up 8.26%.Strategy Behaviour

Performance Review

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Our world Growth Nowcaster increased last week, particularly in developed countries.

- Our world Inflation Nowcaster fell again last week, particularly in the US and the Eurozone.

- Market stress decreased after a more volatile period.

Sources: Unigestion. Bloomberg, as of 14 October 2019.

Navigator Fund Performance

| Performance, net of fees | 2018 | 2017 | 2016 | 2015 |

| Navigator (inception 15 December 2014) | -3.6% | 10.6% | 4.4% | -2.2% |

Past performance is no guide to the future, the value of investments can fall as well as rise, there is no guarantee that your initial investment will be returned.

Important Information

Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed by recipients to any other person. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in the investment vehicles to which it refers. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Please contact your professional adviser/consultant before making an investment decision.

Where possible we aim to disclose the material risks pertinent to this document, and as such these should be noted on the individual document pages. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors.

To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of this information. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Uni-Global – Cross Asset Navigator is a compartment of the Luxembourg Uni-Global SICAV Part I, UCITS IV compliant. This compartment is currently authorised for distribution in Austria, Belgium, Denmark, Finland, France, Germany, Ireland, Italy, Luxembourg, Netherlands, Norway, Spain, UK, Sweden, and Switzerland. In Italy, this compartment can be offered only to qualified investors within the meaning of art.100 D. Leg. 58/1998. Its shares may not be offered or distributed in any country where such offer or distribution would be prohibited by law.

No prospectus has been filed with a Canadian securities regulatory authority to qualify the distribution of units of these funds and no such authority has expressed an opinion about these securities. Accordingly, their units may not be offered or distributed in Canada except to permitted clients who benefit from an exemption from the requirement to deliver a prospectus under securities legislation and where such offer or distribution would be prohibited by law. All investors must obtain and carefully read the applicable offering memorandum which contains additional information needed to evaluate the potential investment and provides important disclosures regarding risks, fees and expenses.

All investors must obtain and carefully read the prospectus which contains additional information needed to evaluate the potential investment and provides important disclosures regarding risks, fees and expenses. Unless otherwise stated performance is shown net of fees in USD and does not include the commission and fees charged at the time of subscribing for or redeeming shares.

Unigestion UK, which is authorised and regulated by the UK Financial Conduct Authority, has issued this document. Unigestion SA authorised and regulated by the Swiss FINMA. Unigestion Asset Management (France) S.A. authorised and regulated by the French Autorité des Marchés Financiers. Unigestion Asia Pte Limited authorised and regulated by the Monetary Authority of Singapore. Performance source: Unigestion, Bloomberg, Morningstar. Performance is shown on an annualised basis unless otherwise stated and is based on Uni Global – Cross Asset Navigator RA-USD net of fees with data from 15 December 2014 to 14 October 2019.