Key Points

- Growth stocks have strongly outperformed other styles over the last decade.

- However, in the current market context, betting on their continued outperformance is not without risk.

- Despite the distinctive approaches of growth and low risk, they can complement each other in a broader equity asset allocation.

A Regime Shift

Growth investing is a well-known strategy in active management. The aim is to put together a portfolio of stocks that captures higher than average growth rates in share prices, profits, revenues or cash flows. The growth style has outperformed many others styles over the past decade, notably enjoying strong outperformance versus value, as demonstrated in Figure 1, and this despite the long run value premium. The relative attractiveness of growth stocks depends on many factors such as their perceived opportunities for financing and expansion, their borrowing costs, cash flows, profits and so on. Therefore, changes in interest rates, economic growth and market sentiment are all factors that can affect how they perform relative to value stocks.

Figure 1: Long Term Style Premium

Source: Bloomberg, MSCI and Unigestion. Data as at 31 January 2022.

Reading note: MSCI ACWI Net TR USD Index is used to represent market portfolio, MSCI ACWI Growth Net TR USD Index is used to represent Growth, MSCI ACWI Value Net TR USD Index is used to represent Value and MSCI ACWI Minimum Volatility Net TR USD Index in used to represent Low Risk.

Since March 2020, the Covid pandemic has amplified the demand for technology and related services, resulting in a surge in growth stocks (especially technology stocks). Specifically, we saw an increase in the need for online shopping, distance learning and home working – so much so that broadband, video conferencing, streaming, gaming and e-commerce are now seen as essential services. In developed markets, investors were particularly drawn to high-growth names such as the FAAMGs (Facebook, Amazon, Apple, Microsoft and Alphabet’s Google), while in emerging markets, e-commerce and internet technology stocks were the main attraction (e.g. Tencent, Alibaba, Meituan). Vaccine makers were also sought after, as there was pretty much no growth in other areas of the markets.

However, now, betting everything on growth stocks continuing to outperform, particularly when valuations are already so high, is not without risks. Growth stocks, reasonably long-duration assets, tend to benefit in a low-interest-rate environment and have enjoyed a fantastic run since the global financial crisis (GFC). However, with Federal Reserve tapering looming, it will be interesting to see how things develop.

After a spectacular run when vaccines were first announced toward the end of 2020, vaccine manufacturers have lost some of their sheen and sparkle in recent months. Moderna is a case in point, following the release of an underwhelming earnings report and lacklustre sales expectations for its vaccine products for the remainder of the year.

Then, just as investors were grappling with uncertainty over whether billions of dollars in sales would materialise as global economies reopen and other therapies are developed, the discovery of the Omicron coronavirus variant late last year reversed sentiment and markets dramatically, and volatility picked up sharply. To illustrate the point, Tesla’s outsized fluctuations make it among the most volatile of the US mega caps in recent months, its share price further impacted by stock sales by its founder and CEO, Elon Musk. After hitting a trillion dollar valuation last October and quickly peaking at more than USD 1.2 trillion, the company is now worth “only” USD 900bn after a 27.5% fall in its share price year-to-date (as at 28.02.2022). Investors may like many things about Tesla, but volatility is certainly not one of them.

Moving into January 2022, shares in Peloton, a fitness company best known for its exercise bikes and remote classes, crashed after the company cut its annual revenue forecast and announced a temporarily halt in the production of its bikes and treadmills. Unlike during the peak of the pandemic period, the company’s current supply output is meaningfully outpacing demand. So far in 2022, other once high flying mega tech growth stocks have also corrected sharply lower, with the likes of Netflix (-34.0%), Facebook parent Meta (-37.7%), Twitter (-16.7%) and Zoom (-28.0%) all suffering massive hits. (Prices as at 28.02.2022).

Conversely, low risk stocks might be considered as “boring” companies that typically do not make for “media darlings”. Moreover, due to often high recurring revenues and pricing power, there tends to be little variation in quarter-to-quarter or year-to-year growth. An example would be Novo Nordisk, where sales are driven by its robust diabetes products. However, its growth outlook is also encouraging and one of the strongest in the sector, given the potential product growth opportunities for Alzheimer’s disease.

Harmonious Coexistence

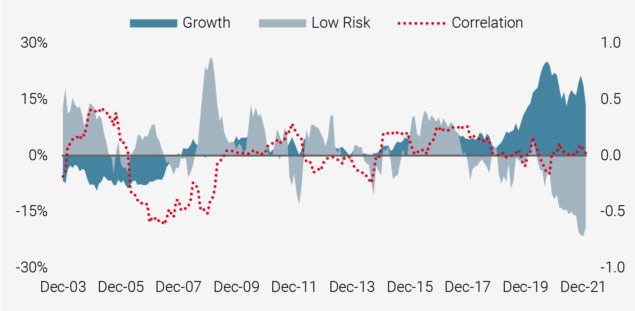

Despite the distinctive characteristics of growth and low risk, they can complement each other in a broader equity asset allocation. The low or negative return correlations often observed between the two styles have historically helped diversify some of the short-term risk and, as a result, the combination of both strategies in a single portfolio has often delivered smoother performance.

Figure 2: Long Term Style Premium

Source: Bloomberg, MSCI and Unigestion. Data as at 31January 2022.

Reading note: MSCI ACWI Net TR USD Index is used to represent market portfolio, MSCI ACWI Growth Net TR USD Index is used to represent Growth, and MSCI ACWI Minimum Volatility Net TR USD Index in used to represent Low Risk.

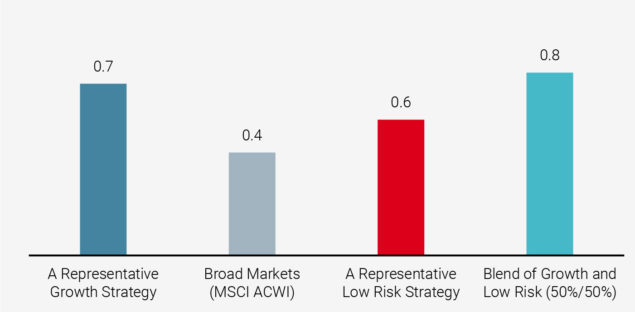

To quantify the effect of employing a low risk equity strategy alongside a growth strategy, we created a hypothetical portfolio plan that consists of two representative strategies at 50% each. As shown in Figure 3, such a balanced approach can deliver superior risk-adjusted returns.

Figure 3: Risk-Adjusted Performance – Sharpe Ratio

Source: Bloomberg, MSCI and Unigestion. Data as at 31January 2022.

Furthermore, as Figure 4 illustrates, this combination delivered a meaningful risk reduction of around 30% while maintaining a high growth rate of 15%. It has certainly helped enhance the return profile of a standalone low risk strategy.

Figure 4: Impact of De-risking with a Low Risk Equity Strategy

Source: Unigestion, MSCI World. Data for the period 31.12.1998 to 31.12.2020.

The Fed and other central banks have played their cards, and investors are already pricing in a series of interest rate hikes. In the event that they increase faster than expected, it is far from clear whether high growth stocks will continue to outperform low volatility stocks, as applying higher rates to future earnings may well hurt long-duration stocks. However, as we have clearly demonstrated, both growth and low risk stocks can play an important role in the diversified portfolios of long-term investors.

Important information

Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed by recipients to any other person. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in the investment vehicles to which it refers. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Please contact your professional adviser/consultant before making an investment decision.

Where possible we aim to disclose the material risks pertinent to this document, and as such these should be noted on the individual document pages. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Unigestion maintains the right to delete or modify information without prior notice. Unigestion has the ability in its sole discretion to change the strategies described herein.

Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors.

To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

No separate verification has been made as to the accuracy or completeness of the information herein. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of information from third party sources. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Legal Entities Disseminating This Document

UNITED KINGDOM

This material is disseminated in the United Kingdom by Unigestion (UK) Ltd., which is authorized and regulated by the Financial Conduct Authority (“FCA”). This information is intended only for professional clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients.

UNITED STATES

This material is disseminated in the United States by Unigestion (UK) Ltd., which is registered as an investment adviser with the United States Securities and Exchange Commission (“SEC”). All inquiries from investors present in the United States should be directed to clients@unigestion.com at Unigestion (UK) Ltd. This information is intended only for institutional clients and qualified purchasers as defined by the SEC and has therefore not been adapted to retail clients.

EUROPEAN UNION

This material is disseminated in the European Union by Unigestion Asset Management (France) SA which is authorized and regulated by the French “Autorité des Marchés Financiers” (“AMF”).

This information is intended only for professional clients and eligible counterparties, as defined in the MiFID directive and has therefore not been adapted to retail clients.

CANADA

This material is disseminated in Canada by Unigestion Asset Management (Canada) Inc. which is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario, Quebec and Newfoundland & Labrador. Its principal regulator is the Ontario Securities Commission (“OSC”). This material may also be distributed by Unigestion SA which has an international advisor exemption in Quebec, Saskatchewan and Ontario. Unigestion SA’s assets are situated outside of Canada and, as such, there may be difficulty enforcing legal rights against it.

SWITZERLAND

This material is disseminated in Switzerland by Unigestion SA which is authorized and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”).

Document issued March 2022.