The world economy is set to grow again in the next quarter. Signs of recovery are increasing and we believe the trajectory is clear. The situation is not without risk but, to us, the lack of enthusiasm expressed by many is unjustified. This return to growth is taking place in an environment of low interest rates and supported by broad fiscal stimuli implemented across a large number of economies. We believe that, during the summer, most 2020/2021 growth forecasts will therefore be revised upwards, motivating investors to look beyond the effect of falling interest rates. In addition, the equity risk premium remains intact, suggesting that equity markets will continue to rise. The “Summertime Sadness” will likely not last all summer.Growth Strikes Back

Summertime Sadness

This is the central question: are we, or are we not, witnessing a recovery commensurate with the shock we have just experienced? In view of the data we collect daily, we think it is beyond doubt. First of all, in terms of data, the economic recovery is shaking up a large number of countries, with the US in the lead. We regularly communicate the message delivered by our global Growth Nowcaster. Since the end of May, our indicator has recovered 60% of its fall in the space of a month and a half. Similarly, 78% of the data that make up our global indicator is improving. These figures alone should be enough to convince our reader that the recovery is well and truly underway, but the more skeptical will want more details. Our growth indicator for the US recovered 72% of its decline in one month, for the Eurozone, 40%; Switzerland, 98% and Australia, 38%. While some countries may leave room for doubt (Canada recovered only 20% of its capacity and the UK just 10%), it remains a safe bet that this is likely due to a delay in data collection (Canada) or late implementation of quarantine measures (the UK). The same applies to India, South Africa and Malaysia, which are also lagging behind. Everywhere else, the recovery is rapid and comprehensive. If there is still any doubt, one need only consider China’s recovery, which looks to be complete, according to our Growth Nowcaster. Having floundered at extremely low levels, our growth indicator now indicates that the economic situation has normalised. As of 7 July, 2020, our indicator for China has returned to positive territory, led by a recovery in consumption and a resumption of global demand. These various developments indicated by the 1,300 data series that are combined and analysed daily in our Nowcasters are clearly corroborated by other data sources: Whatever angle you look at it from, the answer is the same: the recovery is there and it is strong. This question deserves our full attention: is the average investor convinced by what is going on in the economy? We do not think so, and have already communicated widely on this subject: the recovery is in the numbers, but not in the portfolios. Is it any wonder that economists’ forecasts are still at half-mast? Take the case of the US. For private economists, the median forecast for US growth in 2020 is -5.7%, and +4% in 2021. The first of these consensus forecasts is a very mixed conclusion: the fourth quartile of these forecasts for 2020 sees growth at -6%. The upward dispersion is much greater and the first quartile of these forecasts anticipates -4.5% in 2020 and +5% in 2021, i.e. complete economic normalisation in two years. However, there are still a few economists in the US who foresee -9.5% growth this year and zero growth next year. What about the official economists? They too are generally pessimistic. Again, using the US as an example, the Fed is forecasting -6.5% for 2020, the OECD, -7.3% and the IMF, -8%. Overall, the economic forecasts are probably starting to become outdated, failing to incorporate two key elements: Analyst estimates for earnings also reflect wide dispersion among market participants. Currently, the average estimate for 2020 EPS for the S&P 500 is USD 128, with a standard deviation of USD 24.69. To put that number in context, it is nearly five times larger than the dispersion in estimates over the last couple of years and well above the dispersion seen in 2009: the standard deviation in 2019 EPS estimates in July 2019 was USD 4.89, while it was USD 5.41 for 2018 EPS in July 2018. Even in July 2009, the dispersion among analysts for EPS was just USD 9.09. In light of these various observations, it seems logical to expect two elements to support markets in the short term: (1) a marked recovery, and (2) macro data surprising to the upside. These two elements should continue to fuel an improvement in overall investor sentiment. It should be noted that skew in equity indices remains very high, the equity positioning of different types of investors remains low and credit spreads and volatility still have room for more enthusiasm. What is probably concerning many is the valuation argument: has the recovery train already passed? We have already communicated on this subject many times: growth assets have still not entered the expensive zone according to our valuation indicators. Another way of looking at it is to extract the equity risk premium from stock prices, i.e., the compensation required by investors to bear equity risk, once the impact of interest rates and credit spreads has been eliminated. In the case of the S&P 500, this risk premium averaged 3.5% across 2016-2020. It has soared since the end of 2018, from around 2.58% to 4.36% just before the recent crisis. Since then, this premium has moved only slightly and is still around 4%, close to January 2009 levels. This premium could contract by 1% over the next 18 months without any real surprise given the extent of the economic recovery, leading the S&P 500 to reach higher levels (+20%) provided that long-term interest rates change only slightly. With real 10-year yields remaining negative (-0.75%), the bond world is probably the most pessimistic market segment, and that is a good thing: a 1% rise in rates could cost growth assets and moderate the impact of the recovery. In conclusion, the signs are not all positive: the earnings season and the US elections could shake markets in the medium term. However, we do not think the investment community is sufficiently convinced of the recovery. By lowering rates, the Fed has partially convinced investors and markets have regained some colour, but the fiscal packages, their impact and the speed of economic normalisation leave investors unmoved for the time being. We believe that it won’t last and that this “summertime sadness” will have a happy ending.What’s Next?

The recovery is here, no doubt about it

Are we all convinced?

But stocks are already expensive!

Unigestion Nowcasting

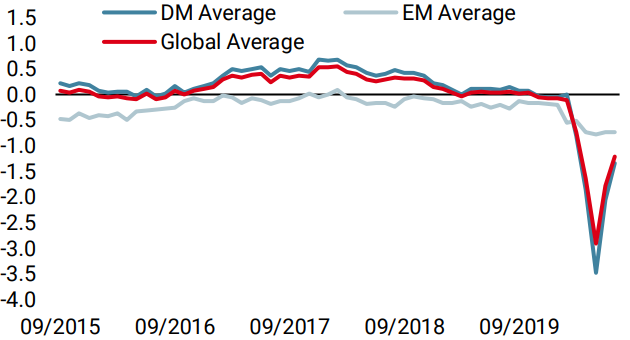

World Growth Nowcaster

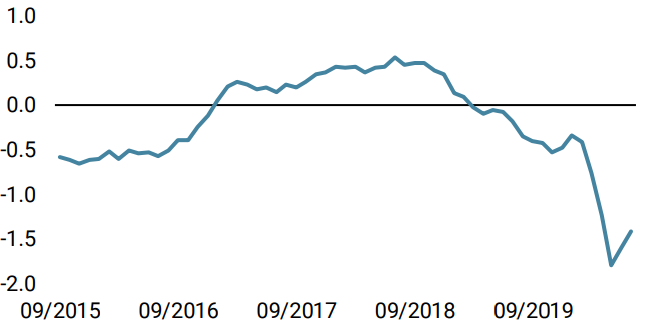

World Inflation Nowcaster

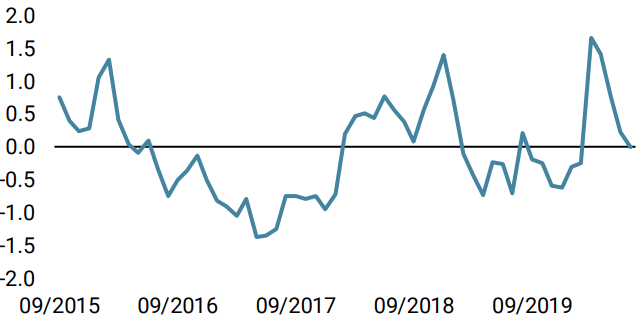

Market Stress Nowcaster

Weekly Change

- Our world Growth Nowcaster increased again last week on further improvement in growth-related data for all economies except Europe.

- Our world Inflation Nowcaster also increased but across a broader base than before. Europe continues to lag for now.

- Our Market Stress Nowcaster stabilised last week, with little movement in volatility and credit spreads over the past five days.

Sources: Unigestion. Bloomberg, as of 10 July 2020.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore (MAS). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).