After the surge in risk appetite that lifted risk assets in April, May, and early June, it seems like financial markets are pausing for breath to assess whether the recent recovery in asset prices and economic data can continue, or if optimism has become too extreme. Pockets of uncertainty remain and the subtle market recipe that mixes macroeconomic fundamentals and behavioural factors must be handled with care. In the wake of a considerable sell-off reversed by massive liquidity and fiscal support, and a subsequent beta party on hopes of a V-shaped recovery, a period of healthy consolidation seems rational and more likely to lead to a lasting recovery.Healthy Consolidation

One Step Back To Move Forward

At this stage in the recovery, it is essential to check repeatedly that the reasons for holding an overweight to growth assets remain. The first of these reasons is the robustness of the macro picture: is recession now at bay? The answer to this question still seems clear to us: the worst is behind us. From our macro indicators, we can see that the majority of data is showing further signs of recovery. In the US, 74% of the data that makes up our Growth Nowcaster is on the rise. In a single month, our US Growth Nowcaster has climbed by two standard deviations, a move that is as rapid as its collapse when entering into the crisis. We are not the only ones seeing this fast-paced US recovery: the Atlanta Fed’s and the New York Fed’s nowcasting indicators are both climbing rapidly from their trough. The latter saw a non-annualised bottom at -9% of GDP growth for the second quarter, which has now corrected back to -5%. The former bottomed at -13% and has now climbed to “just” -11%. It has clearly been a demanding period for most macro models. What we take from all this is the following: projections have started recovering, a sign that the situation is not as bad as many first thought. A second element is that this is not just a US thing, other economies are also exiting the trough. Australia and Switzerland, both small open economies, are recovering. China has now almost fully normalised its growth situation in spite of the challenges of a probable second wave. Europe is lagging for now, but this week’s European Commission numbers should deliver an essential and positive message on the growth prospects of the region. Recurring waves of small-scale lockdowns will make the road to normalisation bumpy without derailing it for three reasons. First, travel activities remain scaled down, limiting the spread of the virus globally. Second, governments now have some experience dealing with the pandemic and have acquired equipment to manage it better. Finally, given the scale of the monetary and fiscal stimulus, we stand a chance of exiting this crisis with limited economic damage: governments are likely to try to avoid another large-scale lockdown at all costs. In our opinion, 2020 will not be a year of positive GDP growth, but the damage will remain contained. What we expect in the coming months is a continuation of the current recovery, with periods of pause as new waves of the virus come and go. Surprise indices in the G10 world are now rising again after a period of stagnation while higher frequency data is improving again, as indicated by our Growth Newscaster. The speed and magnitude of the drawdown will go down in history, but so too will the pace of the recovery. Short-term momentum in growth-related assets such as equities and credit reached multiple standard deviations and peaked on 8 June. The acceleration in the second phase of the “post-Covid” rally bears similarities with the “post-GFC” market action: on a 30 days rolling basis, on average, equity markets dropped – 25% in the 30 trading sessions ending 10 October 2008, compared to -29% on 12 March 2020 over the same time frame. Similarly, rebounds have also been comparable in size and velocity, with two subsequent bursts in each period: +19% on 27 March and +12% on 8 August in 2009 versus +17% on 10 April and +13% on 8 June of this year. Although the resemblance is striking, what is different this time is that the non-systemic, temporary nature of the shock and swift support from policy makers helped to shorten the time between the two accelerations. Therefore, it is unsurprising to see sentiment fade over the short run after such solid gains. Taking a breath is healthy and does not preclude a continuation of the rally. If the GFC is any guide, it is worth noting that risk appetite and related market gains remained elevated for another six months until February 2010, although the second derivative of the rally (i.e., its pace) had diminished. Correlations have been nothing but tricky since the beginning of the shock, with large deviations from historical cross asset relationships during both the down and up swings. To help assess whether or not optimism in Wall Street has diverged too far from Main Street, a closer look at what other risk premia are saying is paramount. Starting with bonds, the current level of yields clearly indicate that not all risk taking has gone in the same direction, with duration seeing limited losses even though risk assets have thrived. The US 10-year yield is currently only 12bps higher than its all-time low of 0.54%, reached on 8 March of this year, and in spite of the massive supply needed to finance fiscal support. This is obviously due to the gigantic stimulus from the Fed and the related increase in its balance sheet to prevent a violent interest rate shock, which could dampen the recovery and throw markets into turmoil, but it also indicates that investors have not gone “all in” in the way money has been invested. Higher up the risk curve, credit has also gone through a reasonable adjustment phase, with spreads decompressing across segments from their recent overbought lows. In high yield, there has been a significant tightening, bringing US and European high yield CDS spreads close to their five-year average, recouping some of their underperformance versus stocks in the process. The consolidation phase occurred in the asset class too, as spreads decompressed by 75bps in Euro high yield and 100bps in US high yield. In the context of an average peak-to-trough tightening of 400bps since early march, this recent widening indicates some selectiveness and caution in the way investors have decided to express their optimism about a strong recovery. In our view, this is a strong sign that over the medium term there is still way to go in the rally even though the ride could be bumpier than over the past couple of months. Outside of bonds, implied volatility has remained elevated, with the VIX index trading around 33 and failing to drop meaningfully in stock rallies. This indicates that directional longs in equities have been accompanied by protection buying to cushion larger drawdowns in addition to the “central bank put”. Commodities have been painting an interesting picture with large dispersions. Gold has continued to attract significant inflows that have pushed the yellow metal to multi-year highs, fuelled by both speculative and physical demand. Oil has managed to consolidate at around USD 40 a barrel following large supply cuts that offer some short-term support in the hope that demand will pick up as economies re-open. Industrial metals as a whole have enjoyed a steady uptrend since their lows thanks to large disruptions caused by the lockdown. This has led to mine and smelter closures and created supply uncertainties, notably in LatAm. As discussed above, we remain of the view that the rapid improvement in macro fundamentals is here to stay, and that growth assets will continue to thrive, even though the tempo of the rise will slow. Consequently, our preference is for equities and credit, which, from current price and valuation levels, offer attractive expected returns over the medium term. However, we also believe that the risks of a downside surprise have risen recently on the back of a resurgence of Covid cases and local lockdowns. We have therefore decided to ramp up protection in our strategies to help cushion against any unexpected, meaningful correction.What’s Next?

Are we missing something on the macro front?

A sane pause?

What are other assets saying?

Still constructive over the medium run

Unigestion Nowcasting

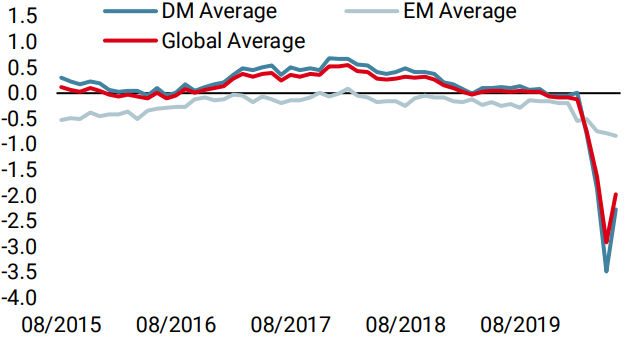

World Growth Nowcaster

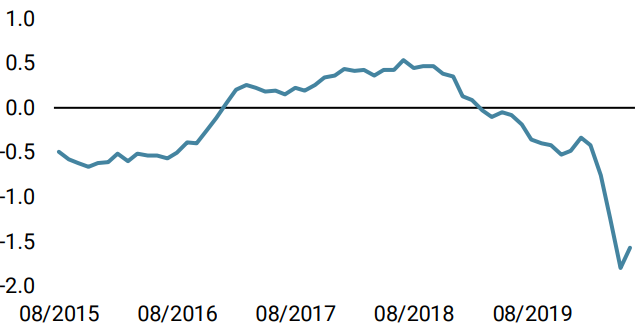

World Inflation Nowcaster

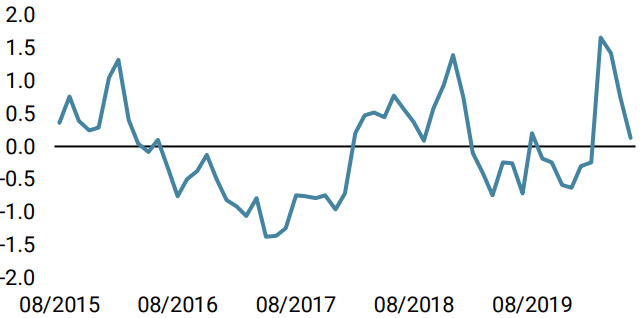

Market Stress Nowcaster

Weekly Change

- Our world Growth Nowcaster increased last week as US and emerging market data point to further macroeconomic improvement.

- Our world Inflation Nowcaster also increased but only US data is recovering. The rest of the data is deteriorating.

- Our Market Stress Nowcaster stabilised last week, rising at the end of the week as markets deteriorated.

Sources: Unigestion. Bloomberg, as of 29 June 2020.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore (MAS). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).