“HOUSE OF CARDS” – RADIOHEAD, 2007

Australia has the nickname the “Lucky Country”. It refers to Australia’s natural resources, weather, history, geographical location, but it also deserves its name for its recent history of prosperity. The country’s current period of expansion is nearing its 30-year mark and is now the longest in modern history. However, all good things must come to an end! This is evidenced by some disturbing trends over the past year and a half that we discuss below. Within the next two weeks, we will have more visibility on how the central bank and the newly elected governing party will try to stop the current negative growth trajectory.

What’s next?

The consistent expansion in Australia in recent history seems like an economic miracle. Despite many economists seeing recessions as inevitable in response to the 1997 Asian crisis, the 2000-2003 tech wreck, the GFC and the “end” of the mining boom, the Australian economy has managed to escape all of these globally synchronised declines. This has been thanks to a combination of economic reforms in the 1980s and 1990s, sound banking regulation, and bold policy responses. Robust growth in immigration, especially with its focus on skilled labour, helped the Australian economy to adjust to a rapid increase in demand for its mineral resources. Trade between China and Australia alone increased tenfold in the 2000s with China investing heavily in Australia.

The Australian economy has had 28 years to build up imbalances and the magnitude of these will come to light during the next crisis. Housing prices rose strongly during the late 1990s to early 2000s and between 2012 and 2017. These massive increases in real estate prices coincide with record low wage growth, record low interest rates, and record household debt, which now equals 130% of GDP. This clearly unsustainable rise ended in 2017 and since then the market had seen its 19th consecutive month of national price declines. The most recent housing data does not provide any evidence that the bottom in prices is nearing. Building approvals year-on-year are currently down 27.3% and have been negative for nine consecutive months. Auction clearance rates, a leading indicator for annual property price movements, fell from 80% in 2017 to below 50% in April 2019 indicating low auction interest, implying a buyer’s market. Additionally, there are many other factors supporting the case for lower real estate prices:

- Prices are still too high for the average worker. House prices have risen much faster than wages and affordability has been constantly shrinking.

- Consumer sentiment has soured as prices started falling and the magic of quick and easy wealth is gone.

- Foreign buyer activity has collapsed because China’s capital controls have started to click in.

- Household debt is excessive and the value of real estate collateral has been falling in price. The ratio of household debt to disposable income hit a new record of around 190%, among the highest in the world.

- Banks have tightened credit conditions after reports of problems in terms of quality of mortgages and the Reserve Bank of Australia (RBA) warned that the major banks risked amplifying the slump if they all pulled back credit at the same time.

- The ever-rising prices created a construction boom and the massive supply is coming with a lag to the market.

The entire economy is massively geared towards the real estate sector (two thirds of the country’s net household wealth is invested in real estates). Rising house prices created an enormous wealth effect, which has fed consumption. The government bodies are aware of the consequences of lower housing prices for the overall economy, however many investors are still in a state of denial. After the weak inflation figure for Q1 was released, the Australian stock market rose about 1 percent to an 11-year high despite having a massive weight of 32% in financials. Bad news is still good news! Equity investors are now hoping for more monetary and fiscal stimulus and a weakening of the Aussie Dollar.

During the last decade, shorting Australian banks became an infamous high conviction trade in the hedge fund industry. The money managers were highly convinced that a slowing domestic economy conjoined with a China slowdown would be the trigger for the house of cards to collapse and thus bring the financial industry the same pain and losses experienced by their European and American peers. However, the more conservative business model and the timing of the short trade became their undoing. The big four banks– National Australia Bank, Westpac Bank, ANZ, and Commonwealth – pay huge dividends and waiting for the day of reckoning has proved very expensive.

Our Australia Nowcasters highlight the fact that the economy is showing plenty of signs of weakness other than the very low inflation. GDP has sagged alarmingly, business investment as a share of GDP is at a 25-year low, but many investors are waiting for evidence that the slowdown is starting to feed through into the jobs market. Currently the market is focusing on the low unemployment rate of 5%: the lowest it has been in five years. However, the unemployment rate does not tell the full story. A worker only needs to be in paid work for as little as one hour a week to be considered employed. Contrary to the unemployment rate, the rate of underemployment has risen constantly and now sits at 8.2 per cent. Consumer confidence has been low and that does not bode well for a country where 60% of GDP comes from consumer spending.

We currently see three risks to our view. First, demand for exports could improve in response to China’s aggressive stimulus measures. Second, the election outcome in two weeks (18th May) is likely to result in a combination of tax cuts and increased spending under the Labor party. Third, the RBA is likely to cut interest rates twice this year to stimulate the economy and to support the real estate market. Each of these possibilities could result in a rosier view for the Australian economy than we currently hold.

Our team believes that Australian bonds will continue to outperform global bonds while the stock market, and especially banking stocks, will underperform their peers. Shorting the Aussie dollar might prove to be a very effective defensive strategy. Historically, such an exposure offered a very reliable and asymmetric hedge for equity market declines. Unlike a short bank trade, the short AUD/USD provides a positive carry and hence gives investors plenty of time for the day of reckoning to arrive.

HOUSE OF CARDS

Strategy behaviour

Our medium-term views remain cautious, and we are pairing an overweight in government bonds with an underweight in high yield corporate credit. We are also complementing our equity exposure with options to protect the portfolio in the case of equity drawdowns.

Performance review

So far in May, the Uni-Global – Cross Asset Navigator fund was down -0.16% versus 0.03% for the MSCI AC World Index and -0.04% for the Barclays Global Aggregate (USD hedged). Year-to-date, the Uni-Global – Cross Asset Navigator has returned 5.22% versus 16% for the MSCI AC World index, while the Barclays Global Aggregate (USD hedged) index is up 3.01%.

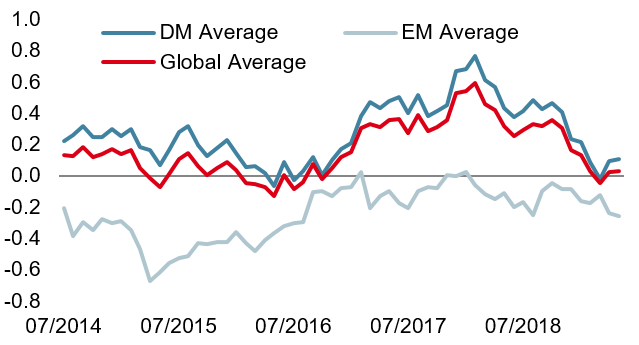

Unigestion nowcasting

World Growth Nowcaster

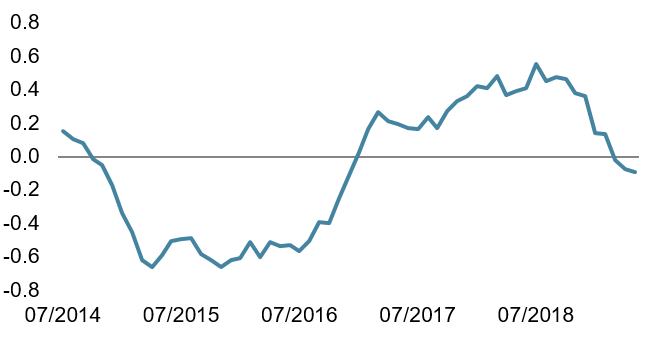

World Inflation Nowcaster

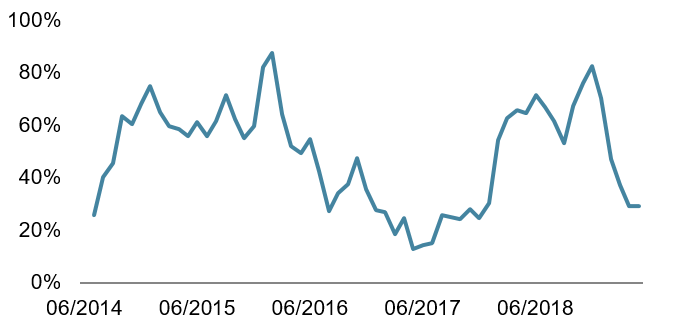

Market Stress Nowcaster

Weekly Change

- Our world Growth Nowcaster rose slightly last week, as DM countries continued printing better macro data.

- Our world Inflation Nowcaster marginally decreased again this week, as Canadian and European data followed the path led by the US over the past few weeks.

- Market stress remained unchanged over the week.

Sources: Unigestion. Bloomberg, as of 6 May 2019.

Navigator fund performance

| Performance, net of fees | 2018 | 2017 | 2016 | 2015 |

| Navigator (inception 15 December 2014) | -3.6% | 10.6% | 4.4% | -2.2% |

Past performance is no guide to the future, the value of investments can fall as well as rise, there is no guarantee that your initial investment will be returned.

Important Information

Past performance is no guide to the future, the value of investments can fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed by recipients to any other person. This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in the investment vehicles it refers to.

Please contact your professional adviser/consultant before making an investment decision. Where possible we aim to disclose the material risks pertinent to this document, and as such, these should be noted on the individual document pages. A complete list of all the applicable risks can be found in the Fund prospectus. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

These are not suitable for all types of investors. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. As such, forward looking statements should not be relied upon for future returns. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of this information. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice.

It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Uni-Global – Cross Asset Navigator is a compartment of the Luxembourg Uni-Global SICAV Part I, UCITS IV compliant. This compartment is currently authorised for distribution in Austria, Belgium, Denmark, Finland, France, Germany, Ireland, Italy, Luxembourg, Netherlands, Norway, Spain, UK, Sweden, and Switzerland. In Italy, this compartment can be offered only to qualified investors within the meaning of art.100 D. Leg. 58/1998. Its shares may not be offered or distributed in any country where such offer or distribution would be prohibited by law.

All investors must obtain and carefully read the prospectus which contains additional information needed to evaluate the potential investment and provides important disclosures regarding risks, fees and expenses. Unless otherwise stated performance is shown net of fees in USD and does not include the commission and fees charged at the time of subscribing for or redeeming shares.

Unigestion UK, which is authorised and regulated by the UK Financial Conduct Authority, has issued this document. Unigestion SA authorised and regulated by the Swiss FINMA. Unigestion Asset Management (France) S.A. authorised and regulated by the French Autorité des Marchés Financiers. Unigestion Asia Pte Limited authorised and regulated by the Monetary Authority of Singapore. Performance source: Unigestion, Bloomberg, Morningstar. Performance is shown on an annualised basis unless otherwise stated and is based on Uni Global – Cross Asset Navigator RA-USD net of fees with data from 15.12.2014 to 06.05.2019.