How Large Is The Inflation Premium?

Head of Macro and Dynamic Allocation, Cross Asset Solutions

For the first time since 2018, the Fed raised its main rates by 25 basis points to 0.5%. The US central bank revised its inflation forecast sharply higher for 2022 and 2023. Moreover, despite a gloomier global growth outlook beset by broader geopolitical risks, the Fed confirmed that fighting inflation was its priority. In that context, what is the current pricing of inflation risk? Should we expect some downside surprises on the inflation front, given that the related premium embedded in different assets is already high and the positioning somewhat crowded?

Too Much

What’s Next?

Fed consensus to fight inflation

The latest dot projections by the Fed, delivered in its March meeting, was hawkish and showed:

- A larger deviation of PCE inflation from its long-term target. The Fed now forecasts inflation to end at 4.3% in 2022 vs 2.6% last December, so 2.3% higher than the long-term target (2%).

- Lower activity this year, with a sharp downgrade of its GDP forecast, from 4% to 2.8%.

- Higher terminal rates, from 2.5% to 2.8%, above their long-term neutral rates (2.5%), meaning that it expects to implement a restrictive bias to curb inflation pressures.

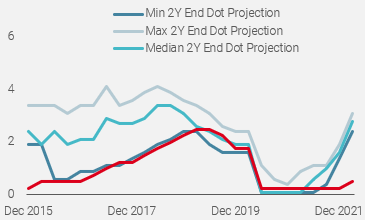

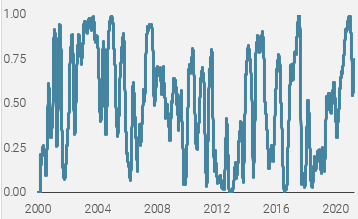

Combined, these changes reflect the shift in the Fed’s target, from “financial stability” and “growth support” to “inflation fighting”. This shift, broadly telegraphed over the last 3 months through different speeches, is clearly visible when we analyse the dispersion of dot projections for the 2yr forward Fed Fund rates. As shown in Figure 1, the spread between the “dovish” and the “hawkish” camp narrowed sharply and looks tighter than in previous hiking cycles, reflecting the strong consensus among Fed’s members now.

Figure 1: 2yr End Dot Projection Dispersion

Source: Fed, Unigestion. As of 18.03.2022.

This consensus formed as dovish members converged towards the hawks, when the minimum 2yr Fed rate, which reflects the most cautious members, moved from 0.1% to 2.4% between the June 2021 and March 2022 meetings. At the same time, the maximum 2yr Fed rate, representing the most hawkish members, increased from 1.1% to 3.1%.

Inflation premium pricing

With inflation currently at highs not seen since the 1980s (7.9% for US headline CPI), the Fed and economists expect a deceleration for the end of the year. Although current forecasts show inflation durably above the Fed’s long-term 2% target, the expected deceleration in inflation would reduce macroeconomic data volatility and do less damage to the economy than in the 1970s, where inflation stayed at record highs for many quarters. Does this mean that inflation hedges have become expensive?

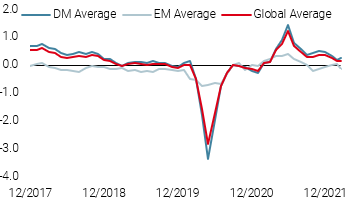

Looking at the current pricing embedded in various assets gives a good idea to what extend markets have repriced inflation risk over the last months. As reflected by the performances of Unigestion Macro Baskets that track the major macroeconomic risks, real assets outperformed massively, from growth oriented to defensive ones (Figure 2).

Figure 2: Macro Basket Performance

Source: Unigestion, Bloomberg

This repricing is also visible in forward inflation swaps. Regardless of tenor, maturity or country, breakevens are high and still rising along the short and long end of the curve. As an example, the current US 10yr breakeven swap is at 3% vs an average of 2% observed between 1998 and 2020. However, the forward 5yr5yr inflation swap remains below its long term 2.7% average, at 2.5%, reflecting the Fed’s credibility when it comes to lowering inflation pressures in the medium term.

Inflation thematic positioning

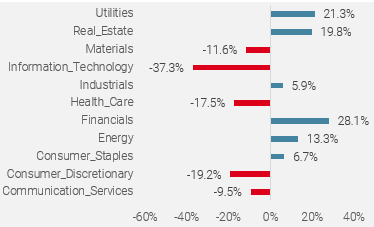

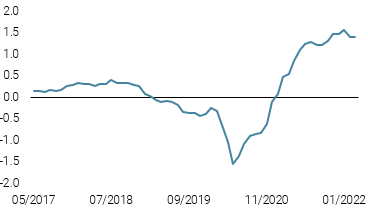

This repricing in the inflation premium also reveals investors’ repositioning in favour of real assets, be it cyclical commodities such as energy and industrial metals or inflation breakevens and energy stocks. This rotation in investor preferences manifests itself in the sector allocation for the Momentum equity factor. The change in the non-sector neutral equity factor computed by our equity team exhibits a large shift from IT and Discretionary to sectors positively correlated to inflation breakevens such as Financials, Real Estate and Energy (Figure 3).

Figure 3: Momentum Equity Factor: 1yr Sector Allocation Change

Source: Unigestion, Bloomberg

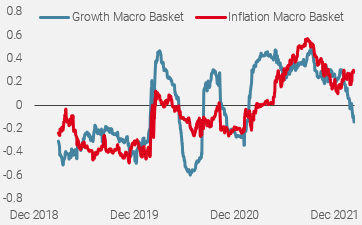

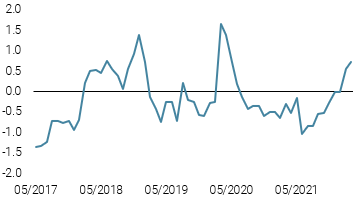

This repositioning is also visible through the correlation between the Momentum equity factor and Unigestion’s Macro Baskets. As shown in Figure 4, the correlation with the Inflation Macro Basket became positive during 2021 and stays historically high in 2022. The recent period also shows a clear rotation from the “growth” to the “inflation” thematic. This suggests that the equity market is pricing in a more negative inflation narrative, one driven by a supply shock rather than growth expansion.

Figure 4: Momentum Equity Factor and Macro Basket Correlation

Source: Unigestion, Bloomberg

To assess to what extent the current positioning in real assets could become crowded, we analyse the historical risk contribution of a naïve cross-asset trend following strategy. Currently, signals favouring real assets such as individual commodities and inflation breakevens are at their maximum for most individual contracts. In terms of risk proportion, given the recent jump in their implied and realised volatilities, real assets’ risk contribution has been regularly above the 75% percentile (Figure 5) recently and represents a large part of CTA strategies’ expected shortfall.

Figure 5: Real Assets Risk Contribution in Cross-Asset CTA Strategies (percentile)

Source: Unigestion, Bloomberg

These different elements reveal a very concentrated positioning for a large part of the investment community that favours only one thematic: high inflation for longer. Having detected the rise in inflation risk very early in 2021 and adjusting our portfolios accordingly (/insight/taming-the-inflation-beast-in-2022/), we know how to protect against a major macro risk. Nevertheless, we continue to think that the exceptional context on the supply and demand side explains the current overshoot and believe inflation will normalise sooner than investors currently expect. Consequently, given the current positioning and pricing of assets, we believe that the inflation premium is too high and expect surprises to the downside in the coming months.

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster rose slightly amidst divergent data, as improvement in developed markets offset a deterioration in emerging markets.

- Our World Inflation Nowcaster ticked slightly higher, as renewed upward pressures hit developed markets, particularly North America and the UK.

- Our Market Stress Nowcaster fell slightly, as spreads and volatilities declined.

Sources: Unigestion, Bloomberg, as of 18 March 2022

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).