How Long Can Oil Continue To Shine?

Oil is once again in the spotlight, reaching levels not seen since 2014. After having traded in negative territory when the pandemic took the world by surprise in 2020, we are now facing $100+ a barrel for Brent crude oil again. A tight market combined with rising geopolitical risk from one of the world’s top producers has created the perfect storm for the oil market. Some analysts say oil could reach $150 in the near future. Over the last few years, climate change policies, the shale oil boom, and the pandemic ensured that there was no shortage of oil and kept prices low, as demand took a hit and supply was ample. Interestingly the last two decades were also key factors that shaped the path towards today’s $100+ oil. Although oil might continue to shine in the near future, we doubt that prices will stay where they are throughout the second part of this year, as we see a number of supportive elements unfolding on the supply side.

Rising Seas

What’s Next?

The fundamental slump

To get a clear picture of how the world is once again facing $100 oil, we need to go a little back in time. There has been a quiet but crucial revolution taking place over the last few years, which is at the root of the supply side issues we are facing today: Climate change. With so much emphasis and pressure put on the oil and gas industry to the benefit of cleaner energy technologies, the sector went through massive underinvestment for years. Oil’s slump during the pandemic led to further capital spending cuts by most oil majors, further aggravating the problem.

Back in the late 2000s, a spike in oil prices to record highs triggered a huge wave of investments into the oil supply chain, which was at the root of the shale-drilling boom and changed the dynamics of the oil markets for decades to come. Given the current spike in prices, can we expect a similar outcome this time around? We believe that this time is different. Although a rise in capital expenditure is expected, a large majority will likely fund the energy transition and focus on renewable energy projects.

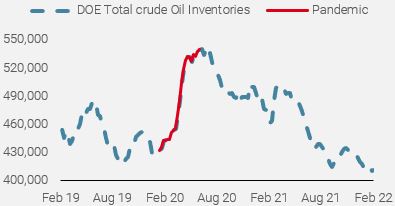

The pandemic of 2020 created a severe demand shock, as large parts of the world came to a standstill. Travel ground to a halt, while closing businesses softened demand for goods and services. Being at the source of most day-to-day life activities, oil demand thus took a direct hit. The result was a rapid rise in crude oil inventories across the globe. US Department of Energy (DOE) crude oil inventory data makes this clear in Figure 1.

Figure 1: US DOE total crude oil inventories in 1’000 barrels

Source: Bloomberg, Unigestion. As of 23.02.2022.

This supply/demand imbalance sent prices tumbling as the world was flooded with oil. Some headlines during the pandemic even suggested that storage in some parts of the world were rapidly filling up to full capacity limits. Towards the end of April 2020, US Oklahoma Cushing crude oil stocks reached close to 65.5 million barrels, leaving just under 15% of spare storage capacity.

This explains how the inconceivable happened, when crude oil traded in negative territory on April 20th, 2020. With nearby futures maturities expiring, long positions had to be liquidated in a thin market, triggering this historic crash.

OPEC and OPEC +

The Organisation of Petroleum Exporting Countries cartel and its members were also active players in the chain of events that shaped the crude oil market since the pandemic. In March 2020, OPEC and its allies (OPEC +) failed to reach an agreement on much needed production cuts. A price war emerged between Saudi Arabia and Russia, two of the world’s top five producers. This further worsened the supply/demand imbalance and became another headwind for oil. Eventually, members of OPEC agreed to cut production to a record low near 10 million barrels per day in 2020 (roughly 10% of global production), in an attempt to restore balance in the broken market.

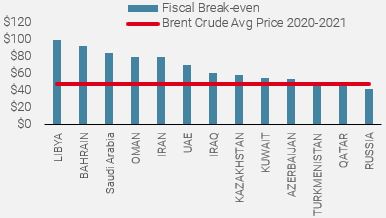

Looking at the fiscal breakevens for key producers and comparing those to the average Brent crude oil prices (world benchmark) for the 2020-2021 period, it becomes clear why something had to be done for the nations who are highly dependent on oil revenue. The fiscal breakeven oil price is the minimum price per barrel that an individual country requires to meet its expected spending needs while balancing its budget.

Figure 2: Fiscal breakeven for major oil producing nations

Source: Bloomberg, IMF, Unigestion. As of 23.02.2022

The U-Turn – from rain to sunshine

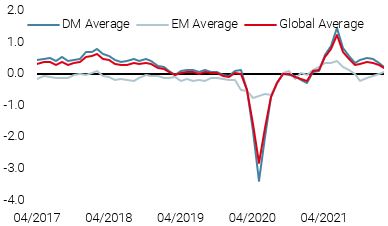

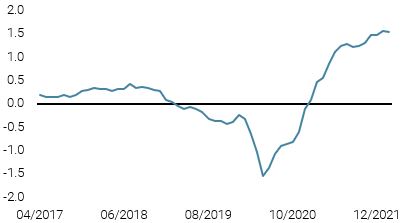

As the world emerged from the pandemic and the vaccine allowed economies to return towards normality, oil prices made a complete U-turn in yet another twist in the supply and demand balance. A number of events created the perfect storm for oil to break above $100 once again. As demand boomed, the supply imbalances quickly turned. Crude oil inventories started falling sharply, reversing their pandemic uptrend, as shown in Figure 1 above, and quickly fell below their seasonal average, fuelling the bullish rhetoric. Inflation surprise risk started to pick up quickly and created inflows, as many investors started to hedge that risk with long oil positions. Our proprietary Inflation Nowcaster, which systematically tracks inflation surprise risk, moved in tandem with Brent crude oil prices, as depicted in Figure 3.

Figure 3: Our World Inflation Nowcaster vs. Brent crude oil

Source: Bloomberg, Unigestion. As of 23.02.2022

Under increasing political pressure from the West and with prices recovering strongly, OPEC gradually started to raise output following the historic cuts made in 2020. However, it failed to keep up with the strong demand-pull by a large margin.

To make matters worse, unusually harsh winter conditions exacerbated peak seasonal demand. This came at an unfortunate time, as the climate and energy policies of the last decade further amplified the supply/demand imbalance. This also came at a time when many energy infrastructures were in maintenance and thus offline, notably in Europe.

The final hit came from geopolitics, which played a large part in the latest leg of the rally. Yemen Houthi rebels launched a series of drone and missile attacks on the UAE, threatening production. More recently, the deteriorating events between Russia and Ukraine sent oil and gas prices sharply higher, given Europe’s high reliance on Russian energy exports. Russia is one of the world’s top oil producers along with Saudi Arabia and the US. Last week’s, escalation pushed Brent crude oil above $100 a barrel.

What now?

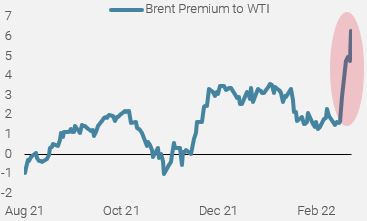

There is no question that the oil market is currently tight and that the rising geopolitical uncertainty in Ukraine should keep energy markets broadly supported. A good gauge for the recent stress is the WTI / Brent crude oil spread. The premium for Brent vs the US WTI market is once again at levels not seen since the pandemic.

Figure 4: Brent Premium to WTI crude oil in $ per barrels

Source: Bloomberg, Unigestion. As of 23.02.2022

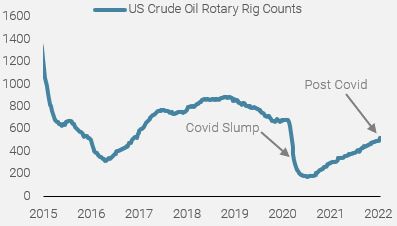

There is, however, some light at the end of the tunnel from a fundamental perspective. We are gently exiting the months of seasonal peak demand. Following the Covid slump, expected oil well start-ups and Rig counts have picked up. Although there is a lag between the time these projects are formulated and when oil physically starts to hit the market, we can expect more supply down the line.

Figure 5: US Baker Hughes Rotary Rig Count data

Source: Bloomberg, Unigestion. As of the 23.02.2022

Given the build-up leading up to the escalation in Ukraine, a good part of that risk premia is now in the price. One of our core scenarios for this year is that inflation is likely to peak, which should eventually lessen the inflation hedge premium currently built into long oil positions. Price shocks, such as the one we are currently experiencing, will also ultimately lead to demand destruction. The other very important element is Iran and the various sanctions imposed on its oil and financial services over the years. Negotiations between Iran and the US are nearing completion and could see these sanctions lifted, which would provide a huge relief for oil as considerable additional supply would make its way to the markets. In the current context, where most consumers are hard hit by the sharp rise in energy prices, the discussions between world powers and Iran are more likely to end in an agreement. The US also confirmed last week that they would release some additional oil from their strategic reserves.

Conclusion

We have been overweight energy markets all last year, as it reflected one of our core calls that inflation would not be transient. We have recently reduced our overweight in energy towards more neutral levels but continue to be overweight in real assets. As supply makes its way to markets in the latter part of this year, and assuming geopolitics do not deteriorate further, price pressures on oil are likely to ease.

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster was unchanged just-above potential levels.

- Our World Inflation Nowcaster was stable, with elevated inflation pressures persisting in most countries.

- Our Market Stress Nowcaster rose sharply, as liquidity deteriorated in a context of high volatility and wide spreads.

Sources: Unigestion, Bloomberg, as of 25 February 2022.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).