How To Build A Top-Performing Private Equity Portfolio In Uncertain Times

- Unigestion has developed a robust and proven investment strategy that is well-suited to all market scenarios.

- Our investment process focuses on seven core investment themes which are underpinned by long-term trends and less correlated to economic growth.

- Our success is built around our long history, our reputation and our exceptional network of over 700 global investment partners, which helps in the swift deployment of capital.

- An efficient set-up and the ability to leverage our vast network allows us to offer investors more attractive fee structures.

Overview

After arguably the longest running bull market in history, it is hard today to ignore the clouds looming on the horizon. Whether this will turn out to be a short-lived period of volatility, or the start of a more fundamental market correction – no one can know for sure.

For investors this poses a real challenge. The combination of an unprecedented market environment coupled with the need to continue to invest means that many LPs are finding it difficult to move forward with much confidence. Should we expect a soft landing, or rather prepare for a hard landing? The question one needs to answer is how to build a topperforming portfolio in the face of extreme uncertainty – one that is able to withstand the current headwinds. At Unigestion, this is a question we ask ourselves every day.

Our Strategy Plays Well in This Environment

With over 30 years of private equity investing experience, Unigestion has developed a robust and proven investment strategy that is well-suited to all market scenarios. For our direct investment programme, we aim to build exciting portfolios of top-performing, hard-to-access, mid-market companies. Furthermore, through the swift deployment of capital and a cost-efficient structure, we are able to further add value, making the final offering highly attractive.

Our Investment Themes

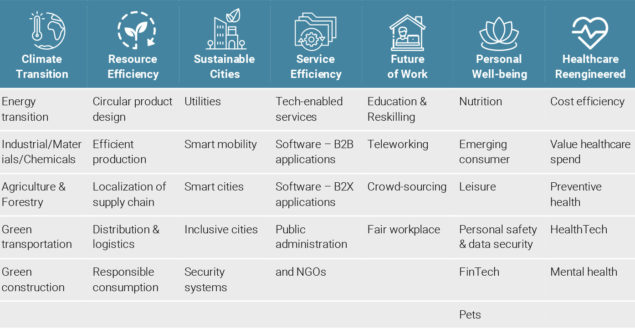

The first step of our strategy is to clearly define our investment themes. We pursue a theme-based, top-down analysis in which themes are regularly defined that give our target investments a structural “tailwind”, making them less dependent on the general economic environment. These themes are defined as growth areas underpinned by long-term trends – see Figure 1.

Another key differentiator of our approach is that it is truly global, targeting a 40-40-20 allocation to North America, Europe and Asia. It is not just geographic exposure, but we also overlay our investment themes with “bottom-up” local regional knowledge. For each region, we prioritise the themes which are most relevant and impactful on performance, leading us to the most compelling opportunities. In times of uncertainty, it is even more important to have a strong global view as different regions will be affected in different ways, requiring a tailored response.

Figure 1: Our Seven Core Investment Themes

Source: Unigestion. Data as at June 2022.

Our focus is on identifying companies that can thrive in any macro environment

Building a Winning Portfolio

In a second step, we look for companies within these investment themes with specific characteristics. Using our proactive bottom-up search process, our focus is on companies we expect to thrive in any macro environment.

The three main risks we are currently trying to address include:

- Slowing economic growth rates. With growth rates in decline globally, it would be unwise to invest in companies where the investment case is based mainly on GDP growth. Our approach has long been to look for companies where growth is uncorrelated to GDP and rather driven by long-term sector trends and increased efficiencies.

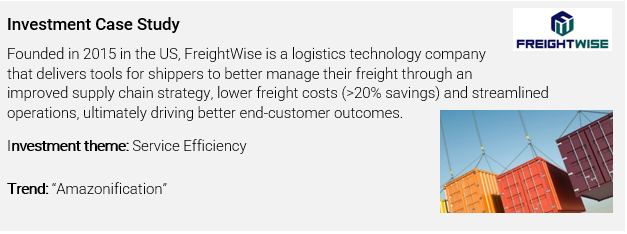

A good example of a recent deal is Freightwise, in the US. In today’s e-commerce-driven world, shipping is no longer just a function, but can become a competitive advantage. FreightWise helps its clients navigate logistics with an easy-to-use cloud-based software that streamlines processes, automates tasks, provides cost-saving insights, and improves customer experience. The significant cost savings that can be achieved lead to real benefits for customers independently of the general macro environment. Indeed, the demand for FreightWise’s offering is reinforced in a downturn as customers seek lower operating costs.

- Inflationary pressures. Another imminent risk is global inflation. The combined effects of the Covid pandemic and the conflict in Ukraine are posing a huge challenge to energy prices, commodities, and overall supply chains, leading to rising prices pretty much across the board. This poses a significant threat to many business plans. We aim to counter this risk by focusing on innovative, service-oriented companies with strong pricing power in resilient sectors.

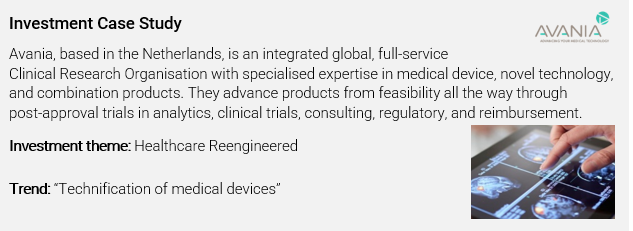

Avania, with headquarters in Europe, is a good example. As a full service outsourced Clinical Research Organisation (CRO) for medical devices, IVDs, biological and cell-based products, Avania’s core offering spans regulatory and strategy consulting, reimbursement, clinical operations, data management and biostatistics, medical writing and medical services to the fast-growing medical devices sector. Tightening regulations and outsourcing trends are supporting attractive growth. This is a trend very much in line with our Healthcare Reengineered theme, as the medical devices industry is fast converging toward the pharma industry business model where larger, branded players focus on marketing and distribution and the rest is left to outsourcing partners.

- Increasing interest rates. The third major risk we see is increasing interest rates. After having been spoiled with unprecedentedly low rates, we are now facing rates that are on the rise – and it might be just the beginning. The use of leverage has never been a core part of our investment strategy, but rather we focus on finding truly exceptional businesses.

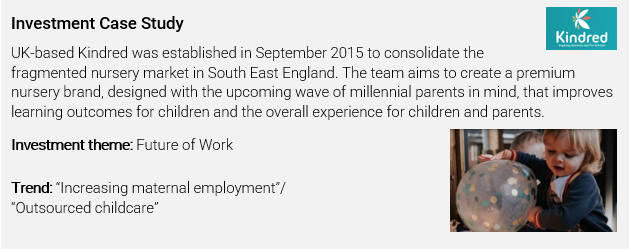

Kindred in the UK illustrates this well. In an effort to avoid additional balance sheet stress while initially strengthening the group and making first acquisitions, we operated without leverage. This helped the company to get through the pandemic and allowed for a more friendly stance towards staff and clients, meaning no layoffs and the ability to offer some flexibility in monthly tuition fees during Covid lockdowns. This paid off further in that the nurseries were fully staffed and quickly back in business after the lockdowns ended, and are today approaching pre-Covid enrolment levels.

Sourcing Unique Opportunities

Investing in attractive companies as highlighted above is key to being successful, but how does one find these opportunities? For us, it’s all about having the right investment partners. At Unigestion, we can rely on our long history of investing in the market, our reputation, and our exceptional network built-up over decades.

Figure 2: Our Investment Partner Network

Source: Unigestion

Today there are 700+ members in our investment network that support us in putting into practice our global mid-market strategy. Not only do they help in sourcing, but they are also crucial in assessing the investment opportunities and helping to add value to our portfolio companies. So when you invest with us, you are not just buying into our team, but into our global partner network, which is an integral part of our value proposition.

When you invest with Unigestion, you are not just buying into our team, but into our global partner network, which is an integral part of our value proposition.

Equally important is our team, which has grown steadily with the addition of specialist investment professionals and portfolio managers across primaries, secondaries and direct investments. Today, we have professionals across five different global offices, representing over 15 nationalities and complementary skill-sets. We believe that this has been vital to ensuring the creation of a broadly skilled and experienced team with large complementary networks and the combined ability to source deals and nurture relationships in all of the key markets across Europe, North America and Asia.

Swift Capital Deployment

A common frustration for investors is that private equity can be a sluggish asset class, taking several years to build up the desired exposure. This can be exacerbated during uncertain times, though it is extremely important to continue investing through all market cycles. In fact, downturns often provide some of the best opportunities due to market dislocation – the key is experience.

At Unigestion, we aim to build exposure for our clients as efficiently as possible and deliver top returns without sacrificing quality. How do we do this? Largely through our experience and unique access to many investment opportunities. We see 450–500 deals that cross our desks annually, all of them warm leads that have been pre-screened and selected from thousands of deals seen by our partners. For most of these opportunities significant due diligence has already been done and broad agreement on terms already negotiated, meaning that we can be much more efficient in our own diligence and spend less time and resources on deals that don’t make the cut.

The final step in our investment process is the application of our proprietary AIpowered tool which we have been developing over the last few years. The model makes predictions on deal outcomes by applying machine learning techniques to over 40 variables across more than 1,400 deals in our deal database. The results to date have been extremely encouraging, allowing us to leverage our extensive database to help us make even better-informed decisions

Our proprietary AI-powered tool applies machine learning techniques to over 40 variables across more than 1,400 deals in our database, leading to better-informed decisions.

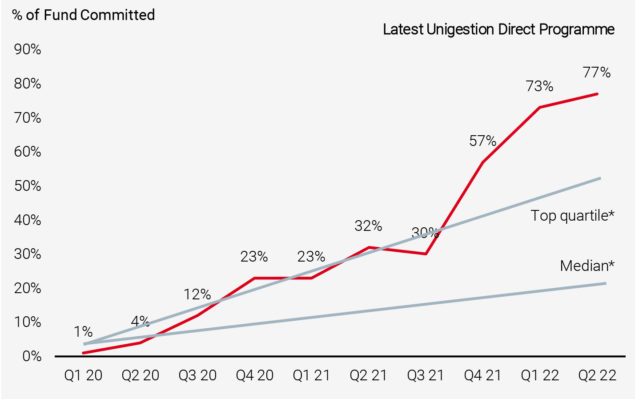

A concrete example of our deployment pace can be seen in Figure 3. We show a comparison of our most recent Direct programme in relation to the top quartile and median funds in our vintage year, where the effect is clearly seen. The benefit of this is a more efficient and cost-effective use of capital, which is further supportive of returns.

Figure 3: 70% of Our 2020 Direct Programme Deployed After 2.5 Years

Source: Unigestion. Data as at March 2022 for our most recent Direct programme.

*Source: Prequin – all 2020 vintage buyout and growth funds by deployment.

Cost Efficient and Aligned With You

The final piece of the puzzle is managing costs. Private equity is renowned for being expensive. Many investors would love to access great deals, but are frustrated with the high fees often associated with the asset class. At Unigestion, our fees are half those of traditional managers, and our carry specifically has a tiered feature, starting low and increasing only if a specific performance threshold is met1. In an uncertain environment, investors would much rather have this enhanced alignment, which translates into an additional performance boost compared to standard private equity fund offerings. We are able to offer this thanks to our efficient set-up and the ability to leverage our vast network of GPs.

Our lower fee structure translates into an additional performance boost compared to standard private equity fund offerings.

Conclusion

While taken individually, the key steps in our investment strategy may not appear to be unique, but we believe that the combination, and its execution, make the final offering extremely unique and compelling for investors.

At Unigestion, we have been successfully executing our private equity strategy since the 1990s. While some of our team members have been with the firm longer than others, the combined knowledge and intelligence has become ingrained in our culture, giving us a collective long-term memory. We have learned how to manage companies through turbulent periods such as the dotcom crash or the GFC. And we remember how to invest and protect against higher inflation and interest rate environments like those we last saw 15 years ago.

This collective experience has allowed us to develop extremely resilient portfolios which have been particularly tested in recent periods of uncertainty and make us well equipped to face any challenges that may lie ahead.

1A typical private equity fund charges a 2% management fee and a 20% carried interest with an 8% hurdle rate. At Unigestion, our latest direct programme has a 1% management fee and a 10% carried interest with an 8% hurdle rate, and 15% carried interest with a 15% hurdle rate.

Important information

Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed by recipients to any other person. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in the investment vehicles to which it refers. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Please contact your professional adviser/consultant before making an investment decision.

Where possible we aim to disclose the material risks pertinent to this document, and as such these should be noted on the individual document pages. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Unigestion maintains the right to delete or modify information without prior notice. Unigestion has the ability in its sole discretion to change the strategies described herein.

Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors.

To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

No separate verification has been made as to the accuracy or completeness of the information herein. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of information from third party sources. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Legal Entities Disseminating This Document

UNITED KINGDOM

This material is disseminated in the United Kingdom by Unigestion (UK) Ltd., which is authorized and regulated by the Financial Conduct Authority (“FCA”). This information is intended only for professional clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients.

UNITED STATES

This material is disseminated in the United States by Unigestion (UK) Ltd., which is registered as an investment adviser with the U.S. Securities and Exchange Commission (“SEC”). All inquiries from investors present in the United States should be directed to Clients@unigestion.com at Unigestion (UK) Ltd. This information is intended only for institutional clients and qualified purchasers as defined by the SEC and has therefore not been adapted to retail clients.

EUROPEAN UNION

This material is disseminated in the European Union by Unigestion Asset Management (France) SA which is authorized and regulated by the French “Autorité des Marchés Financiers” (“AMF”).

This information is intended only for professional clients and eligible counterparties, as defined in the MiFID directive and has therefore not been adapted to retail clients.

CANADA

This material is disseminated in Canada by Unigestion Asset Management (Canada) Inc. which is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario, Quebec and Newfoundland & Labrador. Its principal regulator is the Ontario Securities Commission (“OSC”). This material may also be distributed by Unigestion SA which has an international advisor exemption in Quebec, Saskatchewan and Ontario. Unigestion SA’s assets are situated outside of Canada and, as such, there may be difficulty enforcing legal rights against it.

SWITZERLAND

This material is disseminated in Switzerland by Unigestion SA which is authorized and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”).

Document issued July 2022.