Imagining the future: Alternatives 2.0 with Unigestion

In a world where growth is fragile at best and interest rates are likely to remain low for an extended period, there’s a growing consensus that returns from traditional asset classes will come under pressure in the years ahead.

For many investors, an allocation to alternatives still offers potential for attractive risk-adjusted returns as well as valuable portfolio diversification. However, the low interest-rate environment has also depressed returns for many hedge fund strategies and thrown the issue of fees into stark relief.

There is little doubt from our experience that skilled hedge fund managers can still provide a valuable source of uncorrelated alpha for long-term investors. Yet, advances in quantitative modelling have challenged traditional definitions of alpha and raised the possibility of accessing alternatives in a more cost-effective way.

Our research shows that it’s possible to build a robust alternatives solution around a core exposure to alternative risk premia, which provide investors access to the same broad, diversified set of risks embedded in many hedge fund strategies with greater liquidity, more flexibility, more transparency and at a lower cost.

This can then be complemented by investment in a number of carefully selected diversifying hedge fund managers able to deliver alpha uncorrelated to risk factors. Together, this makes an integrated alternatives solution we call “Alternatives 2.0”.

Risk management will be essential to generate returns and navigate volatility in such an environment. Key skills include expertise in harvesting individual alternative risk premia, the dexterity to allocate between them as economic regimes change, and the ability to identify and get access to the most skilled hedge fund managers.

At Unigestion, we are able to draw on deep experience in these areas from our investment teams. We have significant expertise in the management of risk premia, risk-based asset allocation, and a long history of working with hedge fund managers.

We also have extensive experience of working with clients to co-create the investment solution which is right for them. The result is a holistic alternatives solution which addresses the challenge of costs, liquidity and transparency in a uniquely modular and flexible format.

By Fiona Frick, Chief Executive Officer, Unigestion

Decomposing hedge fund returns

Academic research conducted over the past decade has challenged the idea that hedge fund returns can be attributed to market beta and alpha, less fees.

The reality is more nuanced, with much of what was previously thought of as alpha proven to be due to the existence of differentiated risk premia which can be captured through liquid investment strategies. There is still room for true alpha, but this opens up the possibility of a new way of accessing alternative investment returns.

If we take market beta out of the equation, a more efficient way of generating alternative investment returns can therefore be said to be a combination of:

- alternative risk premia, available through liquid investment strategies, and

- alpha, from carefully selected hedge funds and attributable to manager skill.

More than this, with a thorough understanding of the components of hedge fund returns comes the ability to construct a truly diversified portfolio, with a core exposure to alternative risk premia complemented by individual hedge fund managers able to generate real uncorrelated alpha in the portfolio.

With a thorough understanding of the components of hedge fund returns comes the ability to construct a truly diversified portfolio

At the heart of risk premia investing is the idea that investors are compensated not for holding assets but for assuming risks. These range from market beta, or the return from being invested in the equity market, through to alternative risk premia, which provide systematic explanations for returns which were previously thought of as alpha.

Theory has become practice with the advent of more sophisticated quantitative models and factor analysis tools, and views have changed in the wake of the 2008 financial crisis. The boundaries between traditional and alternative asset classes have blurred, and a growing number of investors now think of diversification as coming not from investing in different asset classes but from investing in the different risk factors that drive these asset classes.

Our Alternatives 2.0 solution

We believe that harvesting risk premia and the generation of alpha are best viewed as separate categories, to reflect very different liquidity terms and pricing structures.

Drawing on our expertise in this area, we combine a directly managed allocation to alternative risk premia with a number of carefully selected diversifying third-party hedge funds, selected for their ability to generate uncorrelated alpha.

The result is an integrated alternatives solution, with the characteristics many investors are looking for and which can also overcome many of the challenges associated with traditional approaches such as high costs, liquidity and transparency.

We believe this sets us apart from hedge fund managers, who will tend to treat alternative risk premia as alpha, producing a very different portfolio composition. Our approach is also quite different from pure quantitative managers, whose models tend to rely on historical correlations and which can prove less reliable at times of inflection in the markets.

We believe this sets us apart from hedge fund and pure quantitative managers

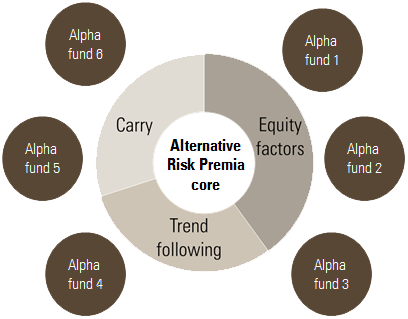

(i) Constructing the Alternative risk premia core

Not every risk commands a premium, and considerable work is required to establish which risk factors deliver sustainable and economically meaningful risk premia. Today, our knowledge and experience lead us towards long/short equity factors, trend following and carry strategies, although we keep this under constant review.

We then apply Unigestion’s risk-management process to create liquid and investable portfolios with attractive risk characteristics. Since alternative risk premia bear specific risks typical of long/short strategies, our proprietary risk models go beyond volatility, taking into account asymmetry, tail risk and illiquidity risk. It is our long-held belief, backed by experience, that risk management is a key driver of sustainable long-term performance.

Based on our understanding of the macroeconomy and the sensitivities of alternative risk premia to the business cycle, we then define the most efficient capital allocation to create well-balanced exposure to macroeconomic regimes and manage it dynamically.

(ii) Adding uncorrelated alpha from hedge funds

While alternative risk premia can be harvested efficiently in this way, genuine alpha, which cannot be explained by risk factors, remains valuable for portfolios as a source of uncorrelated returns.

We strongly believe that top hedge fund managers can deliver a substantial degree of alpha. Manager selection is crucial here, and Unigestion has a 30-year track record of researching and selecting high quality managers. As one of the first in the industry to establish a dedicated operational due diligence team, we believe that our experience in this field and in-depth understanding of each manager we invest in leaves us well placed to identify suitable managers to complement the core exposure to alternative risk premia.

Manager selection is crucial here, and Unigestion has a 30 – year track record of researching and selecting high quality managers

Key to this is a comprehensive analysis of the sources of return of each manager using the advanced modelling tools we have developed, to ensure low correlation with alternative risk premia as well as low cross-correlation between the different managers we select for each investor to ensure robust portfolio construction.

The best of Unigestion

Our strategy draws on deep experience across our equity, multi asset and alternatives teams to offer investors access to the “best of Unigestion”

The past is not always a good guide to the future. In a world where traditional investments may come under pressure, active risk management is required to navigate markets and interest in alternatives remains high, but a new way of accessing these returns is needed.

We believe Alternatives 2.0 is the right solution for many investors. Carefully selected expert hedge fund investments complement a core exposure to liquid alternative risk premia. With good levels of diversification and an approach which permits asset allocation as regimes change, our strategy draws on deep experience across our equity, multi asset investment and alternatives teams to offer investors access to the “best of Unigestion.”

Our Alternatives 2.0 solution draws on Unigestion’s experience

Important Information

This document is addressed to professional investors, as described in the MiFID directive and has therefore not been adapted to retail clients. It is a promotional statement of our investment philosophy and services. It constitutes neither investment advice nor an offer or solicitation to subscribe in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Data and graphical information herein are for information only. No separate verification has been made as to the accuracy or completeness of these data which may have been derived from third party sources, such as fund managers, administrators, custodians and other third party sources. As a result, no representation or warranty, express or implied, is or will be made by Unigestion as regards the information contained herein and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Past performance is not a guide to future performance. You should remember that the value of investments and the income from them may fall as well as rise and are not guaranteed. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.