Industrial Metals In The Spotlight

Commodity markets continue to be in the spotlight as the bull market shows little signs of abating. Industrial metals, historically an important gauge reflecting macroeconomic activity, attracted widespread attention when the Nickel market recently broke down. Prices reached $100’000 a ton in early March from just $21’000 earlier this year, before the exchange wiped out certain trades and implemented measures to curb the excess volatility. Following the Covid 19 crisis, commodity markets were already rallying due to supply side disruptions and the resulting uncertainty about supply/demand imbalances for many of these underlying commodities. Inflation returned with a vengeance, leaving many investors chasing hedges, while the recent rise in geopolitical risk added further fuel to an already burning fire. What can we expect from industrial metals going forward?

Black Metal

What’s Next?

Rational and irrational exuberance

The driving forces behind the post Covid 19 commodity bull-run have been well documented. Booming economic activity and a high inflation risk regime, combined with supply side disruptions, were behind the “rational” commodity price pressures we experienced since the pandemic.

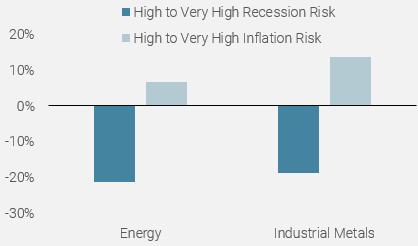

As shown in Figure 1 below, commodity markets, and particularly industrial metals, tend to perform well during “high” to “very high” inflation regimes. In contrast and unsurprisingly, they underperform during “high” to “very high” recession risk regimes. From a macro perspective, commodities markets were therefore in a sweet spot since the latter part of 2020, when our proprietary indicators oscillated between “high” to “very high” for inflation surprise risk and between “very low”, “low” and “neutral” for recession risk.

Figure 1: Average annualized historical excess returns of Energy and Industrial Metals during Recession and Inflation regimes

Source: Bloomberg, Unigestion (1985 – 2022 period)

In recent years, the focus on the “green revolution” has also played a crucial role in the supply / demand patterns for commodities. Fundamentals, however, remain the key driving forces for commodity markets. Although wild price swings occurred over the years, leading to overshoots and undershoots because of excess supply or demand, short squeezes, weather or geopolitical events, prices do tend to normalise over time. In other words, the irrational exuberance is short lived, as the initial low elasticity of supply and demand eventually corrects itself over time.

A recent good illustration is the nickel market, which experienced a historical price rally last month, forcing the London Metal Exchange (LME) to step in and go against what used to be a free market system. Heavy short positions accumulated by Chinese steel producers, representing a large portion of open interest, got squeezed aggressively, pushing the nickel market to rally +400% in the space of a couple of days. Sadly, this is one of the limitations of so-called “hedgers”. They have little choice other than to use proxies to hedge, but are unable to make physical deliveries against their derivatives short positions, leaving them exposed to squeezes. Such exuberance was short lived, as the LME cancelled all trades above $55’000 and suspended trading in the nickel market, before introducing daily price limits for the first time, a practice initially used for agricultural derivatives. The market eventually re-opened and fell sharply, as nickel resumed trading, much more in line with rational fundamentals drivers, which remain unquestionably supportive.

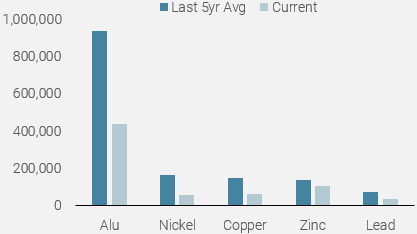

Supply is tight in many commodity markets right now. Looking at industrial metals, which is our focus here, inventory levels remain low and well below their last 5yr averages. The situation has been made worse by the ongoing Ukraine conflict, as Russia is one of the top three producers and accounts for approximately 10% of the world’s nickel production. Aluminium is also greatly affected, as the Russian company Rusal (the world’s top aluminium producer outside of China) halted production at its Ukrainian alumina refinery and is facing logistical issues in getting metal to the market, following the direct and indirect sanctions imposed on Russia by the Western world. LME Aluminium stocks hit a 15yr high in February, an indication of how tight the market currently is. Figure 2 below illustrates the dearth of available physical metals compared to their last 5yr average. For warrant metals, which are readily available for delivery against LME derivatives contracts, the picture is clear and unanimous across the sector.

Figure 2: Base Metals available on warrant in metric tons vs their last 5yr average:

Source: Bloomberg, Unigestion as at 25.03.2022

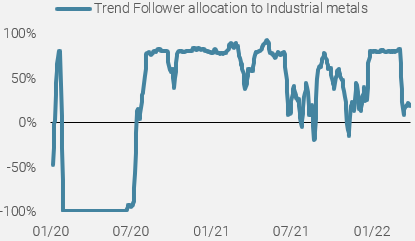

Since the beginning of the year, there have been few places to hide in terms of asset allocation, with most asset classes and sectors suffering some hefty losses. The commodity sector has been shielded and posted some phenomenal returns, with both systematic strategies such as CTA’s and macro funds heavily long the sector as a means to ride the inflation theme, which has dominated the news flows and central bank communications.

Figure 3: Trend following strategies’ allocation to industrial metals

Source: Bloomberg, Unigestion as at 25.03.2022

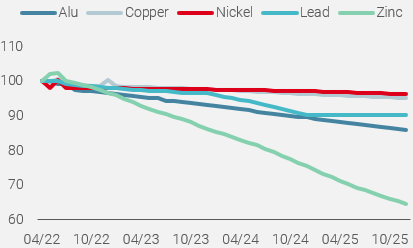

Commodities are usually the asset class most positively correlated with inflation, and the current geopolitical events have made the sector even more attractive from a valuation / carry perspective. Historically, most commodity markets tend to be in a contango (upward sloping forward curve), reflecting that distant delivery months trade at a premium to nearby ones, as in normal market conditions the futures price takes into account the cost of carry (storage, insurance, financing, etc…). However, most industrial metals are currently enjoying steep backwardation, offering investors a positive carry / roll yield, another element supporting the industrial metals complex.

Figure 4: Industrial metals forward curve (rebased to 100):

Source: Bloomberg, Unigestion as at 25.03.2022

What can we expect going forward?

In the short term, low inventory levels and high uncertainty on the supply side, given the ongoing conflict between Russia and Ukraine, should continue to support industrial metals and commodities more broadly. It is also worth keeping in mind that exchanges have adapted to the higher volatility by introducing increased margin requirements, which mechanically tames price volatility by pushing investors to reduce their holdings, given the higher cost incurred. It seems clear that in the short term, little changes are to be expected on the supply front, given the low supply elasticity of most industrial metals.

However, we believe that the demand side of the equation can make the difference. The decelerating growth momentum we have witnessed since the beginning of the year, combined with the strong commodities price pressures will ultimately result in demand destruction. China, the world’s largest consumer of commodities, is also facing its own challenges to stimulate its economy while battling with Covid and implementing lockdowns, given its zero Covid policy, which will also reduce its appetite for industrial metals. The crackdown on Chinese property developers following the default of Evergrande will also naturally reduce demand for industrial metals, as we are less likely to see a property construction boom.

We continue to believe that we have likely seen the peak in inflation, although the timing of that scenario has become more uncertain, given the ongoing geopolitical tensions. If our scenario is correct, we are likely to see a reduction in hedges from the investor community. If the Federal Reserve delivers on its hawkish pricing of monetary policy, we could see a further decline on the growth front, which could push us into recessionary territory, an environment we know to be negative for commodity markets and particularly industrial metals.

Conclusion

Commodity markets are a good way to diversify and therefore play an important role within a multi-asset portfolio. The emphasis on the net-zero carbon goal has also left many commodity markets at risk on the supply side, with mining projects particularly affected. We continue to remain on the cautious side, given the high geopolitical uncertainty and hawkish central banks in an environment of decelerating growth. Markets continue to be very volatile and despite improving sentiment on the back of recent positive headlines from the Ukraine conflict, we know that things can quickly change and that any material resolution will take time. Commodity markets are likely to stay “hot” for now, but the longer term picture is a lot more uncertain, as it depends on how long surging demand will continue to outstrip supply. We view demand destruction as a clear risk to the commodity bull run.

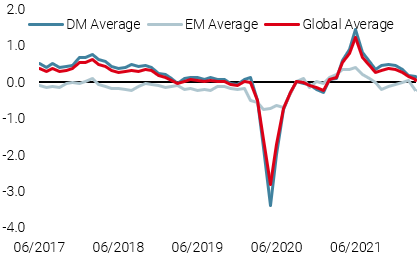

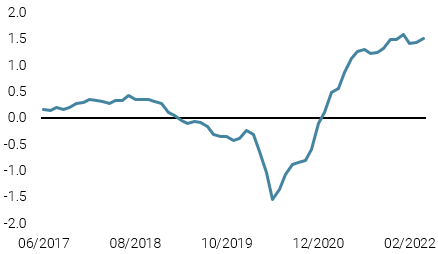

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster moved meaningfully lower, as European and Chinese data deteriorated further.

- Our World Inflation Nowcaster ticked higher, as inflationary pressures in the US continued to build.

- Our Market Stress Nowcaster was steady, as tighter spreads were offset by decreasing liquidity.

Sources: Unigestion, Bloomberg, as of 4 April 2022

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).