In the space of a few weeks, an increasing amount of data has started to indicate a significant shift in the macro forces influencing financial markets. Inflation risk has gone from neutral to high as our Inflation Nowcasters and Newscasters climbed sharply. This in itself is not a negative message for equity markets: inflation remains a sign of growth. However, current valuation levels and extremely positive sentiment blur the outlook over the short term, preventing us from going to the maximum of our pro-growth allocation. For that, we need to wait.

Still I Wait

What’s Next?

Inflation risk continues to rise in the US

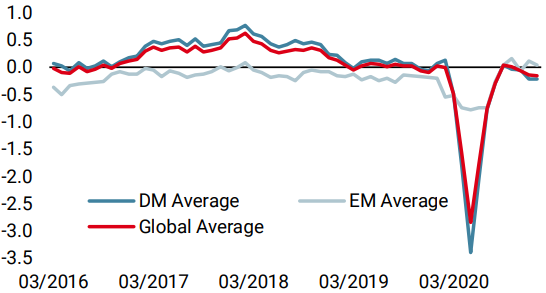

Our global Inflation Nowcaster turned positive on 18 January after almost a year spent around negative territories, and in sharp contrast to May lows, a level that historically appears only 5% to 10% of the time. To explain this increase, various US inflation surprise triggers have started to rise rapidly. Our US inflation indicators became positive again in mid-December before accelerating their rise in the first few days of January. We believe that this acceleration is worthy of note as its composition reflects the challenges of the current situation. First of all, the speed of the recovery has shifted pricing power from consumers to producers. This has led to a rapid acceleration in the “supply shock” component of our inflation surprise indicator. Demand is strong and supply is limited by the consequences of the pandemic, and this should push inflation numbers up further.

At the same time, inflation expectations continue to recover. While inflation breakevens have already risen quite significantly, it is now the turn of consumer surveys to flag inflation risk. Surveys from the University of Michigan and the Cleveland Fed are all indicating that inflation could surprise in the coming months. Interestingly, the Cleveland Fed’s indicators anticipate rising inflation in the medium term but low inflation in the short term. Inflation therefore does not appear to be a short-term hurdle in the coming weeks, but rather a part of the broader picture for 2021 and possibly 2022. A similar situation is arising for the rest of the developed world: all of our country-level news and nowcasters are now showing high readings. The US ones appear to be paving the way with the others playing catch-up.

In emerging countries, signs of supply and demand imbalances are accumulating

Inflation also seems to be rising in the emerging world, particularly in China and Brazil. There are two main reasons for this, both of which are essential in the current times. First, production costs have been rising recently. This has less to do with the impact of oil prices and more to do with the rise in industrial metals. The price of copper has risen by 70% since its low point in March 2020, reaching levels last seen in 2017. With pricing power shifting to producers, this increase in production costs is not good news: it basically means higher prices in the medium term, should demand remain strong. Food inflation is also showing strong momentum. Anecdotally, the prices of soybeans and rice show a strong increase in January (+5%) while garlic (an ingredient widely used in Asian food) has seen its price soar by 15% since its lows in 2020. Here again, demand is on the rise and supply is limited. While we would normally attach little importance to food inflation in emerging countries from an investment perspective, we believe that this is a further indication of the limits that supply is currently encountering and the risks that this poses for future inflation.

Exuberant market sentiment

Increasing inflation risk is not in itself a negative message for growth assets as a whole. It seems to be an issue for the fixed income world, as credit generally suffers during these periods of revaluation of inflation risk with current Sharpe ratios hovering around -0.5. However, as discussed last week, this is not necessarily a negative message for equities (with a Sharpe ratio close to zero during such periods). What persuades us to keep a certain restraint in our pro-active growth bias is the mix of market exuberance and high valuations.

While January is historically positive for equity markets – January 2018 and its consequences will be long remembered – January this year seemed to show a certain exaggeration, in line with last December. Over the period 1999-2021, the S&P 500 and the MSCI AC index saw respectively 55% and 54% of days with positive returns in January. In January 2021, this figure rose to 70% and 73%, respectively. We saw only a quarter of a day of negative trading at the beginning of the year, a sign of investors’ somewhat unreasonable infatuation with the equity markets. This, coupled with high valuations and very strong growth expectations for 2021, raises questions. Analysts expect 8% sales growth in the S&P 500 universe in 2021, 2% more than in 2017, while the pandemic seems far from being behind us for the moment.

This “pricing perfection” means that we should not add much more to our pro-growth bias in our allocation. We are maintaining and accentuating our positive bias, in line with strong macro fundamentals, but valuation and sentiment are increasingly weighing on our minds. The macro situation remains good, but not like 2017 yet, and this is what our dynamic positioning reflects to date.

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

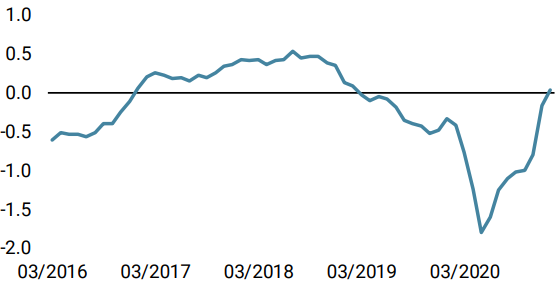

- Last week, our World Growth Nowcaster declined again across most countries with the exception of China and the UK.

- Our World Inflation Nowcaster continued to increase: the change in the level of inflation risk has been a major driver to our strategies’ positioning over the past four weeks.

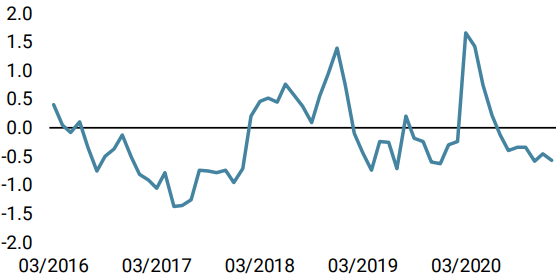

- Our Market Stress Nowcaster decreased as volatilities and credit spreads declined. In spite of Friday’s bearish turn of events, our stress gauge remains in very growth-oriented territories.

Sources: Unigestion. Bloomberg, as of 25 January 2021.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore (MAS). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).