Inflation to Normalise in 2022

From “Low and Rising” to “High and Falling”

In 2021, the fiscal stimulus – first used by households and companies as precautionary savings, then as consumption – added a demand effect to the initial supply shock, resulting in a monumental inflation surprise. Our Nowcasters, combined with a thorough analysis of the post-Covid supply chain – which exhibited low inventories and an overdependence on certain geographical areas and specific components – revealed at a very early stage that the risk of a supply shock would be the most important factor for inflation in 2021. This reflation narrative has persisted over the last twelve months, morphing into a full-blown “inflation” story, with real assets outperforming growth assets and most fixed income products delivering negative returns for the first time in a while.

Will inflation continue to soar in 2022?

We do not believe it will, as next year should be the year of inflation normalisation. As such, our central scenario for 2022 calls for an easing in supply bottlenecks, lower growth, and a tighter policy mix, which in turn should weigh on inflation momentum. The inflation thematic, which has unleashed a significantly large and broad rotation in 2021, is unlikely to persist, as a commensurate rise of its most volatile contributors in 2022 looks implausible from these levels. Indeed, food, energy and other commodities are responsible for over half of headline inflation this year while less volatile components such as shelter and medical care grew at an elevated but more sustainable pace and only contributed 1.9% to the 6.2% y/y rise in the CPI. Absent an extraordinary surge in these core components, food and energy prices would need to see another upswing like the one in 2021 to keep inflation at these levels, implying oil trading at over 125 USD/bl. Indeed, market pricing suggests that commodity prices are set to fall in 2022, which aligns with lower demand and increased supply expected next year.

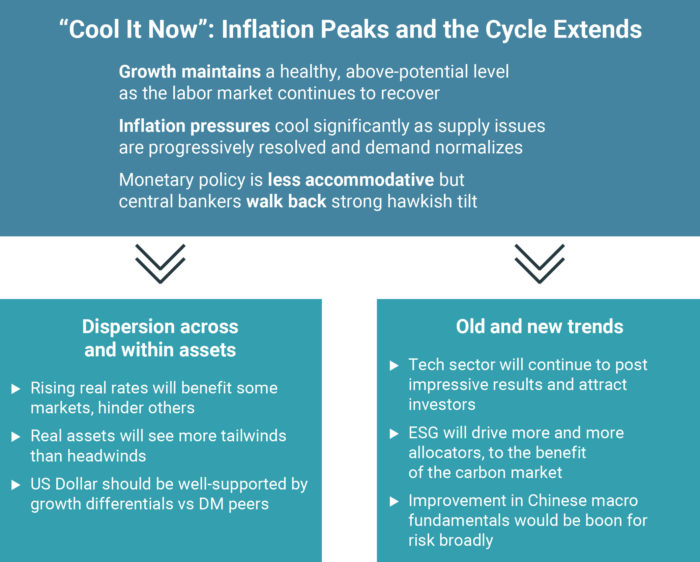

Our Core View for Next Year: Inflation Normalizes

In 2022, monitoring real rates and the US yield curve will be key to assess to what extent the expected tightening by the world’s major central banks could derail the bullish trend in both earnings growth and returns for growth and real assets. A combination of faster tapering and inflation deceleration would push real rates higher and would weigh on valuations for growth-oriented assets.

As a result, we see next year as more challenging for beta, hampered by tighter financial conditions combined with waning fiscal and monetary support, as well as higher growth uncertainty due to the uneven sanitary crisis.

Against that backdrop, we would prefer:

- Quality segments in equities that offer solid earnings growth and higher visibility in terms of profitability

- US equities versus the rest of the world thanks to higher flexibility in the US policy mix and its corporate leadership

in key sectors - A US Dollar that should benefit from stronger US GDP and higher liquidity in its capital markets, both of which should drive flows into US assets

- We would also be less exposed to real assets than we were in 2021, as current pricing in both inflation breakevens and energy prices reflect a durable expansion period in the global cycle, which in our view, given the potential headwinds identified for next year, is now too optimistic.

What if we are wrong?

We see two potential scenarios that could derail our core views for 2022:

1. The dreaded “Monetary Policy Mistake”

In this scenario, inflation peaks later than we anticipated, leading central banks to tighten earlier and more than expected. Worse, central banks could slam on the breaks even sooner, shifting to a narrative of “durable” inflation, even though it has already peaked and is starting to fall. As a result, bond yields would rise across the board, punishing growth assets, triggering a vicious cycle of position liquidation and deleveraging.

2. Covid lingers, gets worse

Vaccine effectiveness could wane, new and more dangerous variants would appear, leading to increased lockdowns and restrictions on a global scale. Households and companies would then pull back into “precautionary savings” mode, while central banks start stimulating massively again to avoid deflation and cascading defaults, pushing bond yields significantly lower. Meanwhile, governments ramp up fiscal stimulus again, issuing huge amounts of debt.

Figure 1: Risk scenario

What if we are wrong?

Two alternative scenarios that would challenge our core view

Figure 2: 2022 Asset Allocation views

Important information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).