- Inflationary pressures, rising interest rates and the Russian invasion of Ukraine have combined to take the shine off growth stocks this year.

- There has been a notable rotation within markets, with value and low risk significantly outperforming.

- However, regional discrepancies exist, and Europe has been the notable underperformer for low risk, while emerging markets fared best.

- Our analysis indicates that it may be time for investors to reaffirm their faith in low volatility as a driver of long-term outperformance.

After several quarters of rhetoric citing inflation as transitory, major central banks changed their tune at the start of 2022, delivering more hawkish messages as they vowed to tame inflation, sending interest rates markedly higher. Since then, Russia’s invasion of Ukraine and the subsequent sanctions imposed on the country have sent energy prices rocketing, adding to already strong inflationary pressures, and equity markets have been highly volatile.

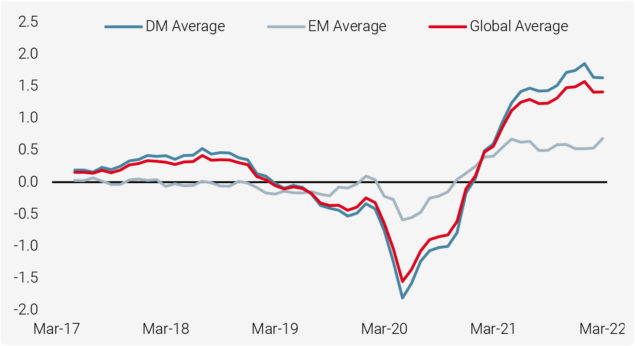

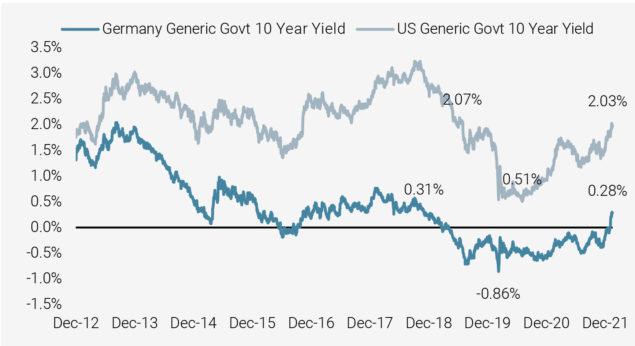

Figure 1 charts the steep trajectory of these inflationary pressures since their lows in 2020, which have pushed key interest rates to two (US) and three (Europe) year highs, as shown in Figure 2.

Figure 1: Inflationary Pressures Have Plateaued at Elevated Levels

Source: Bloomberg, Unigestion. Data as at 23.03.2022.

Figure 2: Sharp Rebound in US and German 10-Year Yields

Source: Bloomberg, Unigestion. Data as at 15.02.2022.

Low volatility and value are once again providing the downside protection for which they are usually known

Against this changing macroeconomic backdrop, growth stocks, long the darlings of investors, have been among the hardest hit. Even before Russia’s actions, they had begun to lose some of their sparkle, as investors assessed the impact of higher inflation and rising rates on their growth prospects. At the same time, we saw the traditional low volatility and value sectors outperform significantly and provide the downside protection that they are usually known for but that many had been questioning over the last couple of years.

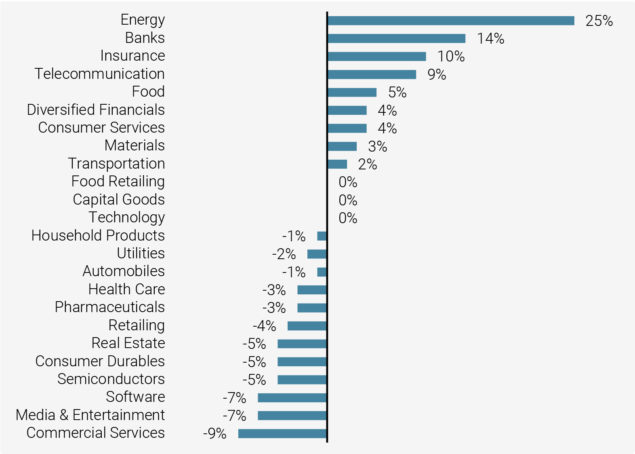

Figure 3 details the sector hierarchy year-to-date and highlights these stark differences. As can be seen, cyclical value sectors such as Energy and Banks have outperformed significantly, while growth sectors have suffered. It is also interesting to note that some traditional bond proxies, such as Telecoms, have not suffered due to rising rates, supported instead by relatively attractive valuations.

Figure 3: Year-to-date Sector Performances for MSCI World (in USD)

Source: Bloomberg, Unigestion. Data as at 17.03.2022.

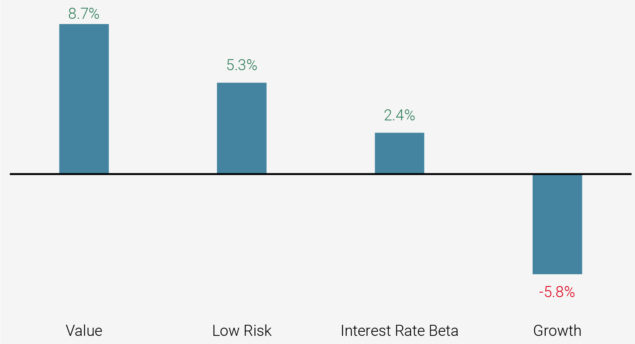

The discrepancies become even more obvious when we look at the factor performances in Figure 4.

Figure 4: Year-to-date Factor Performances

Source: Bloomberg, Unigestion. Data as at 28.02.2022. Unigestion Global (ACWI) Equities Factor Model.

We believe that central banks’ policies and the Russia/Ukraine conflict may have triggered a longer-term shift in equities

Looking ahead, we believe that central banks’ policies and the Russia/Ukraine conflict may have triggered a longer-term shift in equities, signalling a prolonged period of uncertainty, price volatility and lower growth. Against the current backdrop and outlook, our analysis indicates that it may be time for investors to reaffirm their faith in low volatility as a driver of long-term outperformance.

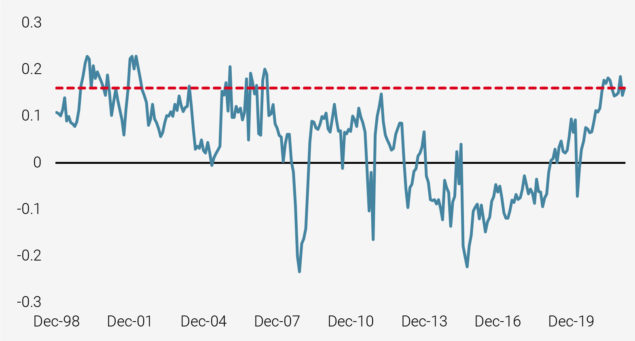

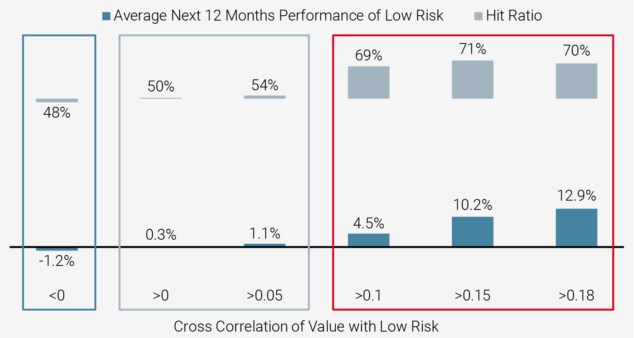

Figure 5 highlights how low risk and value are once again starting to move in sync, with their strongest cross-sectional correlation levels since 2007. And, as illustrated in Figure 6, historically, the stronger this correlation, the stronger the performance of the low risk factor over the next 12 months. When the correlation is above 0.18, a level close to where we stand currently, the low risk factor has historically delivered positive performance over the next year 70% of the time, with an average next 12 month return of 12.9%.

Figure 5: Cross Correlation of Low Risk and Value Scores (for MSCI ACWI)

Source: Bloomberg, Unigestion. Data as at 28.02.2022.

Figure 6: Average Next 12m Performance of Low Risk

Source: Bloomberg, Unigestion. Data as at 28.02.2022.

Regional Discrepancies

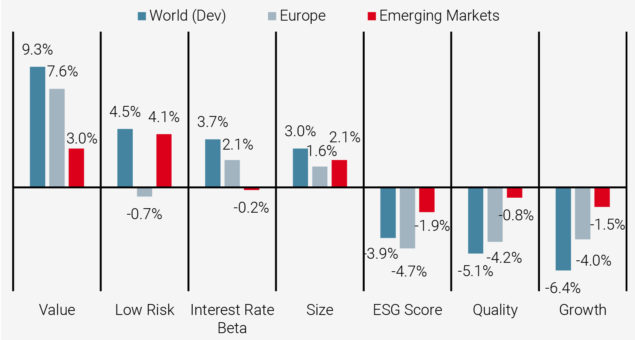

So far in this paper, we have demonstrated the good downside protection shown by the low risk factor year-to-date within global equities. However, there have been significant differences across regions, notably with European equities, where low risk has been particularly disappointing in terms of capital protection. As Figure 7 shows, EU low risk has actually delivered a negative return so far this year. Looking at the behaviour of other factors, we can see that value has also underperformed in Europe relative to global equities, while growth has suffered less. Companies with solid ESG credentials have also underperformed more in Europe compared to the rest of the world. It is a similar story with size, with the performance of mid-caps (in which low risk often finds a sweet spot) being more muted than large caps.

Europe has been the notable underperformer for the low risk factor

Figure 7: Year-to-date Factor Performances Across Regions

Source: Bloomberg, Unigestion. Data as at 28.02.2022.

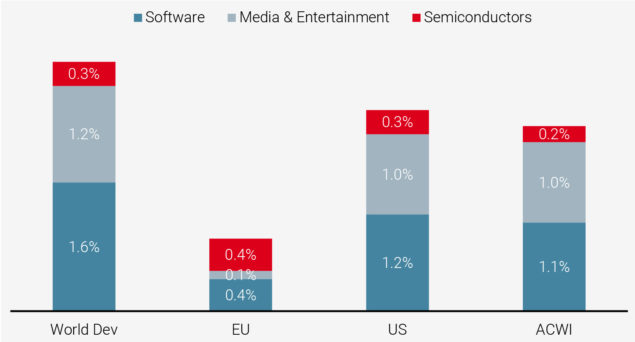

In terms of sectors, the less pronounced lag of growth stocks in Europe, combined with a lower weighting of growth sectors such as Software, Media and Semiconductors in European indices, led to a much less pronounced positive impact of the traditional underweight of low risk strategies in growth exposures. We estimate this impact to be only 0.9% in Europe, while it provided between 2.3% and 3.1% of relative returns in our other regional strategies, as shown in Figure 8.

Figure 8: Year-to-date Total Relative Contribution in Growth Sectors

Source: Bloomberg, Unigestion. Data as at 28.02.2022. Regional representative accounts on World ACWI, World Developed, Europe and USA vs their respective benchmarks: MSCI ACWI TR Net USD, MSCI World TR net USD, MSCI Europe TR Net EUR, MSCI USA TR net USD. Performance is stated gross of fees.

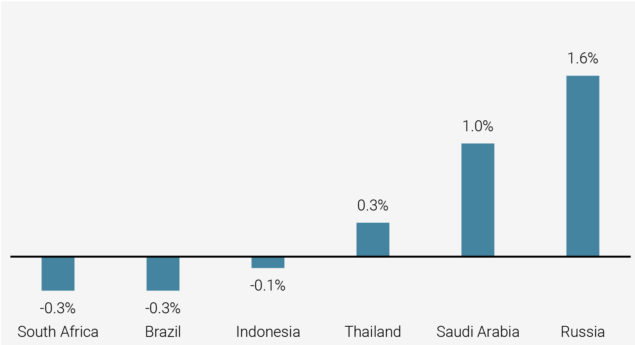

Contrary to Europe, emerging markets have been the best place to be invested in the low risk factor year-to-date

Contrary to Europe, emerging markets have been the best place to be invested in the low risk factor year-to-date. Russia’s invasion of Ukraine has had a significant negative impact on both Russian stocks and the rouble. We estimate that the relative performance contribution of our divestment from Russia, which was implemented in early December 2021 on the back of the growing geopolitical risks, to stand at approximately 1.6% so far in 2022. Combined with our exposure to more defensive countries such as Thailand and Saudi Arabia, our geographical allocation, which is a consequence of our low risk approach and our active management of the Russian risk, has proved very successful, as shown in Figure 9.

Figure 9: Year-to-date Key Country Allocation Impacts – Emerging Markets Strategy

Source: Bloomberg, Unigestion. Data as at 28.02.2022. Representative account on Emerging Markets vs MSCI Emerging Markets TR net USD. Performance is stated gross of fees.

Conclusion

Over the last three years, low risk strategies have been something of a disenchantment for investors. However, it is now time for investors to reassess the place of such strategies in their equity asset allocations. In an inflationary, low growth and uncertain environment, valuations of growth stocks are likely to come under continued pressure, while low risk names with attractive valuations, good credit quality and solid visibility on earnings should attract investors and could deliver above average results. Combined with risk characteristics more favourable than market averages, risk managed strategies will likely find a suitable environment to strive in the coming years. Having said that, low risk alone will not be enough, and investors will need to carry out a full 360-degree risk assessment, addressing factors such as fundamentals, interest rate sensitivity and ESG.

Important information

Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed by recipients to any other person. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in the investment vehicles to which it refers. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Please contact your professional adviser/consultant before making an investment decision.

Where possible we aim to disclose the material risks pertinent to this document, and as such these should be noted on the individual document pages. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Unigestion maintains the right to delete or modify information without prior notice. Unigestion has the ability in its sole discretion to change the strategies described herein.

Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors.

To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

No separate verification has been made as to the accuracy or completeness of the information herein. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of information from third party sources. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Legal Entities Disseminating This Document

UNITED KINGDOM

This material is disseminated in the United Kingdom by Unigestion (UK) Ltd., which is authorized and regulated by the Financial Conduct Authority (“FCA”). This information is intended only for professional clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients.

UNITED STATES

This material is disseminated in the United States by Unigestion (UK) Ltd., which is registered as an investment adviser with the United States Securities and Exchange Commission (“SEC”). All inquiries from investors present in the United States should be directed to clients@unigestion.com at Unigestion (UK) Ltd. This information is intended only for institutional clients and qualified purchasers as defined by the SEC and has therefore not been adapted to retail clients.

EUROPEAN UNION

This material is disseminated in the European Union by Unigestion Asset Management (France) SA which is authorized and regulated by the French “Autorité des Marchés Financiers” (“AMF”).

This information is intended only for professional clients and eligible counterparties, as defined in the MiFID directive and has therefore not been adapted to retail clients.

CANADA

This material is disseminated in Canada by Unigestion Asset Management (Canada) Inc. which is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario, Quebec and Newfoundland & Labrador. Its principal regulator is the Ontario Securities Commission (“OSC”). This material may also be distributed by Unigestion SA which has an international advisor exemption in Quebec, Saskatchewan and Ontario. Unigestion SA’s assets are situated outside of Canada and, as such, there may be difficulty enforcing legal rights against it.

SWITZERLAND

This material is disseminated in Switzerland by Unigestion SA which is authorized and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”).

Document issued April 2022.