The macro context has been changing fast lately. Over the past few months, a ‘goldilocks’ environment with record growth, supposedly temporary inflation pressures and highly accommodative central banks has turned into a slowing recovery with higher inflation and decreased monetary support. Risk assets have finally started to reflect this planetary misalignment. Increased macro and political uncertainties have begun to weigh on sentiment as investors try to assess whether these developments are merely a glitch in the macro matrix or if they could lead to a more concerning “stagflationary” backdrop.

Inertia

What’s Next?

What is the Data Saying?

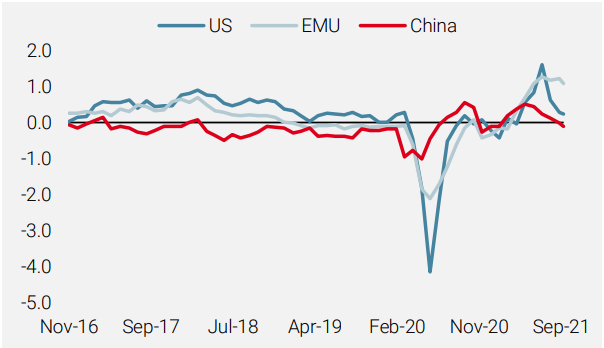

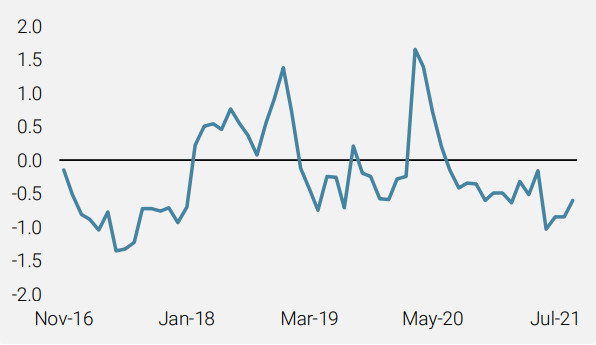

Our proprietary Growth Nowcasters started decelerating in July, indicating that the recovery had peaked in June. The deceleration gained traction over the summer as a natural mean reversion from extreme levels; not so concerning per se, but the continuation of the downward trend caught investors’ attention in September, including ours. More importantly, the two major economies driving the trend are China and the US, which is far more worrying. The deceleration spiral sequence is following the same pattern as the post-Covid recovery: China, followed by the US, followed by Europe. Our Chinese Nowcaster has now turned slightly negative, indicating below-potential growth for the first time since January 2020. It took just three months for China to turn from an economy running above potential to the current level, so the next quarter will be critical to assess whether Chinese growth will stabilise around its long-term potential or if it dips further towards recessionary levels. The same phenomenon has been observed in the US, despite starting from a higher base. The pace of the slowdown has been meaningful: for the past two months, on average, 67% of growth-related data has deteriorated versus previous readings. The level of the US Nowcaster has dropped to almost zero, indicating that the US economy is now growing at its long-term potential. In Europe, it looks like growth peaked recently and will likely mean revert as well.

Figure 1: US, China, and Eurozone Growth Nowcasters

Source: Bloomberg, RavenPack, Unigestion, as of 14.09.2021

On the inflation side, higher pressures for longer now seems to be a commonly accepted expectation among market participants, less so by central bankers. Examples of rising prices pour in every day and their common denominator is the imbalance between supply and demand, especially on the supply side. PPI and CPI indices have been rising in concert, although the former is outpacing the latter. The spread between PPI and CPI has not been so wide since the oil crises in the mid-1970s. Examples of skyrocketing input prices are legion: aluminium and coal prices are up 50% since their pre-Covid levels, transportation costs to move a container from Shanghai to Los Angeles have increased seven times over the same period, electricity prices by a factor of five – the list goes on.

Consequently, the combined forces of decelerating growth and higher-for-longer inflation could lead to stagflation, pushing policy makers to adjust monetary policies accordingly.

Figure 2: US CPI/PPI Differential

Source: Bloomberg, Unigestion, as of 14.09.2021

Sentiment is Shifting

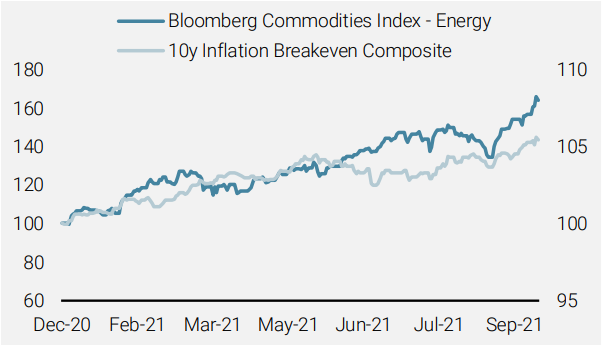

The Goldilocks environment has probably come to an end and the planets are now out of alignment. Recent market action on and below the surface indicates that investor complacency has eased but not disappeared. The MSCI AC World index is down 2% from its 6 September peak. Although it looks like another dip in the rally, other more pro-cyclical markets such as the US Russell 2000 index of smaller companies are down twice as much, reflecting growth concerns. Volatility spiked too as the VIX index traded above 20 for the first time since mid-August. Rotation-wise, the outperformance of growth stocks against value stocks has finally stabilised. Inflation-related assets have continued to perform strongly, especially inflation breakevens and cyclical commodities.

Figure 3: Inflation Breakevens and Energy Total Returns – YTD

Source: Bloomberg, Unigestion, as of 14.09.2021. Inflation composite is an equal weight US, European and UK Inflation Swaps returns

Selectively Constructive

We believe that current market action makes sense given the uncertainties that have emerged recently on both macro and political fronts. The momentum observed up until September had turned from what we considered “rational exuberance” into complacency, leading us to become more cautious and reduce allocation to riskier assets. Nevertheless, our assessment of the current environment remains positive, albeit with more discrimination. We expect both macro and market volatility to run at a higher pace than earlier this year, but we expect growth to stabilise around its long-term potential. Continued improvements in vaccination campaigns will keep demand afloat, and imbalances in the US jobs market should normalise sooner rather than later, now that the special Covid compensation benefits are being terminated. In the meantime growth uncertainties should relieve pressure on central bankers to taper and provide accommodation for longer, but probably at a reduced pace. We therefore continue to favour reflation assets, which play a key diversification role in the current environment.

Unigestion Nowcasting

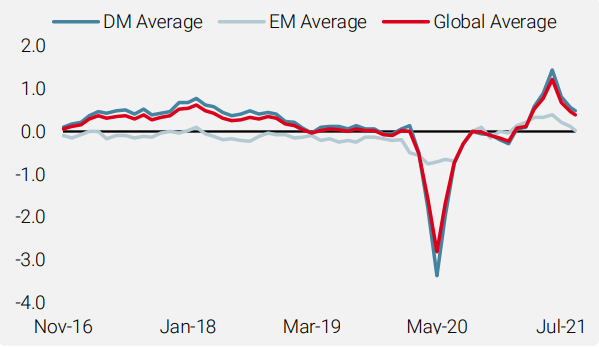

World Growth Nowcaster

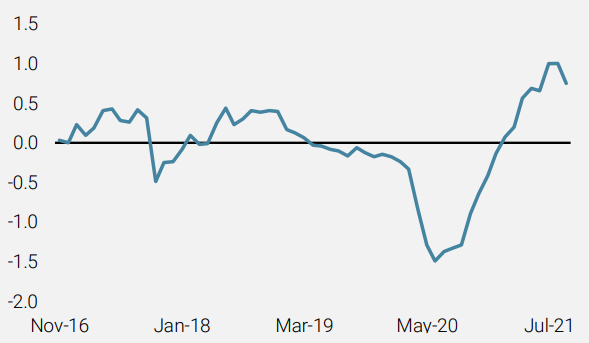

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster was steady as most major economies saw stable growth data.

- Our World Inflation Nowcaster rose slightly led by higher inflationary pressures in the developed world, in particular the UK and Canada.

- Our Market Stress Nowcaster finished the week where it started.

Sources: Unigestion, Bloomberg, as of 17 September 2021.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).