With the revival of trade war tensions, global equities experienced their largest drawdown of the year last week. After an impressive rally year-to-date, exceptional in terms of both amplitude (one of the strongest starts to the year since 1970) and path (one of highest hit ratios in history), global equities fell by 2.5%. Does this signal the end of the beta party that was triggered by the US Federal Reserve’s accommodative turn last December or will the market continue to dance? And against this backdrop, has diversification and hedging proved effective? As is usual during market stress events, contagion to other risky assets has been large with rising implied volatility, widening credit spreads and falling cyclical commodities. Within this market environment, classic defensive assets have failed to protect diversified portfolios. Global sovereign bonds were slightly positive, while precious metals declined slightly and systematic hedge fund defensive strategies, such as CTA, posted negative returns over the period. Although the period under review was too short and the trigger too noisy to create a large ’flight to quality’, it does challenge the benefits of using these kinds of defensive assets in a multi asset portfolio.“LET’S DANCE” – DAVID BOWIE, 1983

What’s next?

Classic diversifiers have not delivered expected protection

Firstly, the drawdown follows a very poor year for diversification. Indeed, a distinctive feature of 2018 was the lack of benefits from diversification, which is one of the key pillars of multi asset strategies to deliver smoother returns over time. Most of the ’usual’ defensive assets posted poor returns over the year and were significantly lower compared to previous equity market corrections. We have analysed the performance of these classic hedges (global sovereign bonds, defensive hedge fund strategies, commodities) in the years when the MSCI World AC index posted a negative annual return. Our findings show that diversification did not play its role in 2018, with an average hedge performance of -3.9% versus an annual average of +4.4% for the period 2000 to 2017. Some usual defensive strategies helped to smooth the return last year such as low volatility equities but, overall, with a higher frequency of large moves, 2018 delivered one of the largest correlation shocks in many years.

Secondly, if correlation across assets and correlation between defensive assets and macro regimes are changing, we need to adapt our dynamic risk management. It is crucial at this stage of the economic cycle to dissociate 1) diversifiers, such as sovereign bonds or gold, which provide positive carry but uncertain protection due to changing correlations, and 2) hedges, such as long volatility or optional strategies, which are more certain but have a negative carry. We believe in both diversifiers and hedges, which would allow us to dance until the very last song.

Quantitative easing (QE) has modified the impact of central bank action on both asset returns and asset behaviour. Before the great financial crisis, central bank easing had an impact on long-term rates through the forward curve and on risky assets via discount rates. The correlation between sovereign bonds and equities turned from positive to negative in the 1990s for Japanese assets and from 2000 for US ones. In the US, this was referred to as the ’Fed put’ – the Fed’s willingness and ability to adjust monetary policy in a way that was supportive for stock markets.The new central bank put: from rates channel to volatility channel

Since the financial crisis, the role of central banks is no longer to ease financial conditions but to suppress volatility shocks. Liquidity injections and low rates for longer periods pushed investors to take on more risk via longer duration, higher leverage or lower credit ratings. The rising ratio of central bank balance sheets to GDP has lowered realised and implied volatility for financial assets and macro data. Whatever the news, that is good for risk because central banks are and will be there.

In the past, central banks would surprise markets to prove their independency and increase their credibility, but in 2013 we had the famous ’taper tantrum’ episode. Since then, we have guidance and dot projections and this has helped reduce any element of surprise. But what does this mean for diversifiers and for hedges?

Firstly, it is counterintuitive. It increases the cost of hedging because selling volatility becomes more and more profitable, while carry costs of being hedged become more and more expensive. Secondly, if the probability of or if the amplitude of shocks become lower, the need for hedges declines. We then enter a vicious cycle where lower implied volatility creates higher risk taking, leading to bigger drawdowns when there are unexpected shocks, which in turn leads to closer central bank monitoring to avoid financial instability, triggering lower realised volatility.

That last implication of QE is the low level of interest rates. If we consider that there is a floor for negative rates, the cushion provided by bonds with negative rates becomes lower.

Against this new backdrop, we believe that strategically encompassing new sources of return in order to diversify protection is key to delivering smooth returns. Using FX strategies is one way because they react to macro risks and central bank actions, they are liquid enough to be flexible and they are not as constrained as bonds with negative yield. We have developed two defensive strategies to expand the universe of diversifiers beyond traditional ones, such as sovereign bonds and low volatility equities. Our FX value strategy, which is long undervalued FX versus overvalued FX, has delivered positive absolute returns over the last five years but, importantly, it has posted positive returns during periods of market stress. We have also developed a defensive FX strategy to increase our equity protection. Mixing different criteria such as correlation to equities, high hit ratios when equities decline or constraints on the cost of carry, the strategy aims to deliver positive returns with higher asymmetry than sovereign bonds when risk assets suffer. These FX strategies worked very well in 2018 and also posted positive returns last week. We like going to the dancefloor and listening to the ‘new’ music of central banks. However, we prefer to dance with a large spectrum of diversifiers and intensify our dynamic hedging through optional strategies because when the music stops, correlations and asset returns shift to the negative, leading to lower realised protection compared to expectations.Diversifying the protection

Let’s Dance

Our medium-term views are fairly neutral, with selective overweights in risky assets including investment grade and emerging credit. We continue to protect the downside from an equity sell-off via options as we see challenging conditions for global equities. Month-to-date, the Multi Asset Risk Targeted Strategy* is down 1.0% versus a fall of 2.5% for the MSCI AC World index and a rise of 0.2% for the Barclays Global Aggregate (USD hedged). Year-to-date, the Multi Asset Risk Targeted Strategy has returned 4.4% versus 13.0% for the MSCI AC World index, while the Barclays Global Aggregate (USD hedged) index is up 3.3%. * The Multi Asset Risk Targeted Strategy performance is shown in USD net of fees for the representative account of the Multi Asset Risk Targeted (Medium) USD Composite and reflects the deduction of advisory fees and brokerage commission and the reinvestment of all dividends and earnings. Past performance is not indicative of future performance. This information is presented as supplemental information only and complements the GIPS compliant presentation provided on the following page.Strategy behaviour

Performance review

Unigestion nowcasting

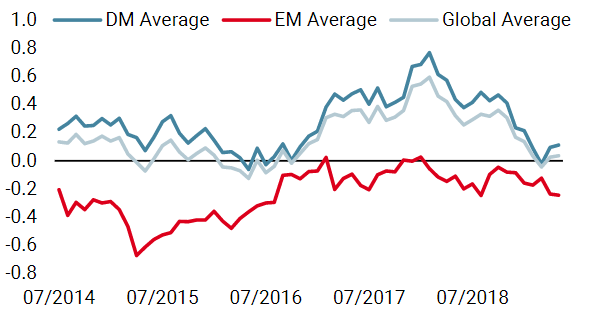

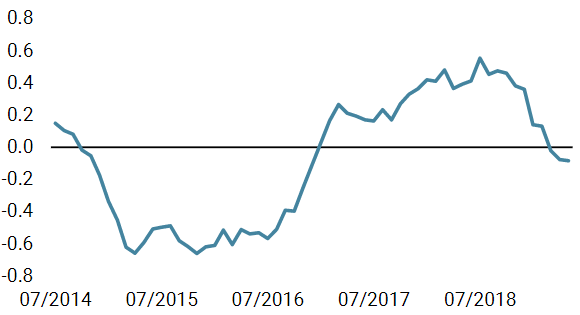

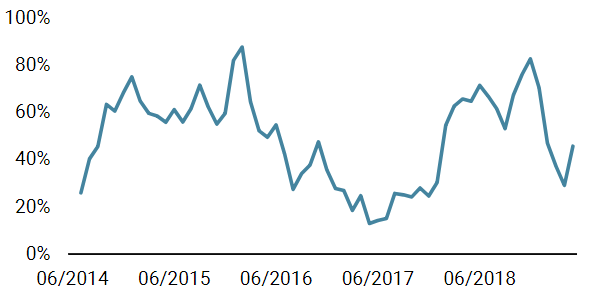

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Our world Growth Nowcaster remained unchanged last week, giving another confirmation of the pause in the slowdown.

- Similarly, our world Inflation Nowcaster remained stable at sub-zero levels, implying inflation risk is low for now.

- Market stress increased significantly over the course of the week, with volatility and spreads moving higher.

Sources: Unigestion. Bloomberg, as of 13 May 2019.

Important Information Past performance is no guide to the future, the value of investments can fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed by recipients to any other person. This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in the investment vehicles it refers to. Please contact your professional adviser/consultant before making an investment decision. Where possible we aim to disclose the material risks pertinent to this document, and as such these should be noted on the individual document pages. Please contact Unigestion for a complete list of all the applicable risks. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. As such, forward looking statements should not be relied upon for future returns. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of this information. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor. Depending on your country of residence, this document is distributed by Unigestion UK Limited, Unigestion SA, Unigestion Asset Management (France) S.A., Unigestion Asia Pte Limited or Unigestion Asset Management (Canada) Inc. Unigestion UK Limited is authorised and regulated by the UK Financial Conduct Authority (“FCA”). Unigestion UK Limited is also registered as an investment adviser with the U.S. Securities and Exchange Commission (“SEC”). Unigestion SA is authorised and regulated by the Swiss FINMA. Unigestion Asset Management (France) S.A. is authorised and regulated by the French Autorité des Marchés Financiers. Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore. Unigestion Asset Management (Canada) Inc. is authorised and regulated by the Ontario Securities Commission. Unigestion Multi Asset Risk-Targeted (USD): 31 December 2014 to 31 December 2018 1: This year is incomplete. Special Disclosure: For presentations prior to 31.03.2018 the strategy was measured against the LIBOR 3M USD + 4%. Beginning April 2018 the firm determined that the benchmark did not accurately reflect the strategy mandate and the benchmark was removed. Definition of the Firm: For the purposes of applying the GIPS Standards, the firm is defined as Unigestion. Unigestion is responsible for managing assets on the behalf of institutional investors. Unigestion invests in several strategies for institutional clients: Equities, Hedge Funds, Private Assets and the solutions designed for the clients of our Cross Asset Solution department. The GIPS firm definition excludes the Fixed Income Strategy Funds, which started in January 2001 and closed in April 2008, and the accounts managed for private clients. Unigestion defines the private clients as High Net Worth Families and Individual investors. Policies: Unigestion policies for valuing portfolios, calculating performance, and preparing compliant presentations are available upon request. Composite Description: The Multi Risk Targeted (Medium) composite was defined on 15 December 2014. It consists of accounts which aim to deliver consistent smooth returns of cash + 5% gross of fees across all market conditions over a 3-year rolling period. It seeks to achieve this by capturing the upside during bull markets while protecting capital during market downturns. Benchmark: Because the composites strategy is absolute return and investments are permitted in all asset classes, no benchmark can reflect this strategy accurately. Fees: Returns are presented gross of management fees, administrative fees but net of all trading costs and withholding taxes. The maximum management fee schedule is 1.2% per annum. Net returns are net of model fees and are derived by deducting the highest applicable fee rate in effect for the respective time period from the gross returns each month. List of Composites: A list of all composite descriptions is available upon request. Minimum Account Size: The minimum account size for this composite is 5’000’000.- USD. Valuation: Valuations are computed in US dollars (USD). Performance results are reported in US dollars (USD). Internal Dispersion & 3YR Standard Deviation: The annual composite dispersion presented is an asset-weighted standard deviation calculated for the accounts in the composite the entire year. When internal dispersion is not presented it is as a result of an insufficient number of portfolios in the composite for the entire year. When the 3 Year Standard Deviation is not presented it is as a result of an insufficient period of time. Compliance Statement Unigestion claims compliance with the Global Investment Performance Standards (GIPS®) and has prepared and presented this report in compliance with the GIPS standards. Unigestion has been independently verified for the periods 1 January 2003 to 31 December 2016. The verification report(s) is/are available upon request. Verification ssesses whether (1) the firm has complied with all the composite construction requirements of the GIPS standards on a firm-wide basis and (2) the firms policies and procedures are designed to calculate and present performance in compliance with the GIPS standards. Verification does not ensure the accuracy of any specific composite presentation.

Year

Composite

Return Gross

of FeesComposite Net Return

Benchmark Return

Number of Accounts

Internal Dispersion

Composite 3-Yr Std Dev

Benchmark 3-Yr Std Dev

Composite AUM (M)

Firm

AUM (M)

2015

-1.61%

-2.80%

–

1

–

–

–

127.24

15,550.31

2016

5.05%

3.79%

–

1

–

–

–

129.66

18,144.46

2017

11.16%

9.82%

–

1

–

–

–

169.51

22,340.80

2018

-2.91%

-4.08%

–

1

–

–

–

286.93

21,403.49

20191

5.06%

4.74%

–

1

–

–

–

278.23

23,204.71