The current financial – and soon to be economic – crisis has gone through a sequence. It started with a macro shock, leading to a financial correction, triggering a flight to liquidity and creating a significant systemic risk. Although the sequence seems similar to previous crises and to the most infamous of them all post-World War II, the GFC, we think there are key differences with 2008 that are worth considering. These differences imply a different medicine for the economy and the falling markets, even more so as the average investor is now rushing to cash. This means a liquidity crisis could follow this economic crisis, making us lean on the defensive side.

Liquidity Crunch and Recession Call for Defensiveness

Hurt, Johnny Cash, 2002

Hurt

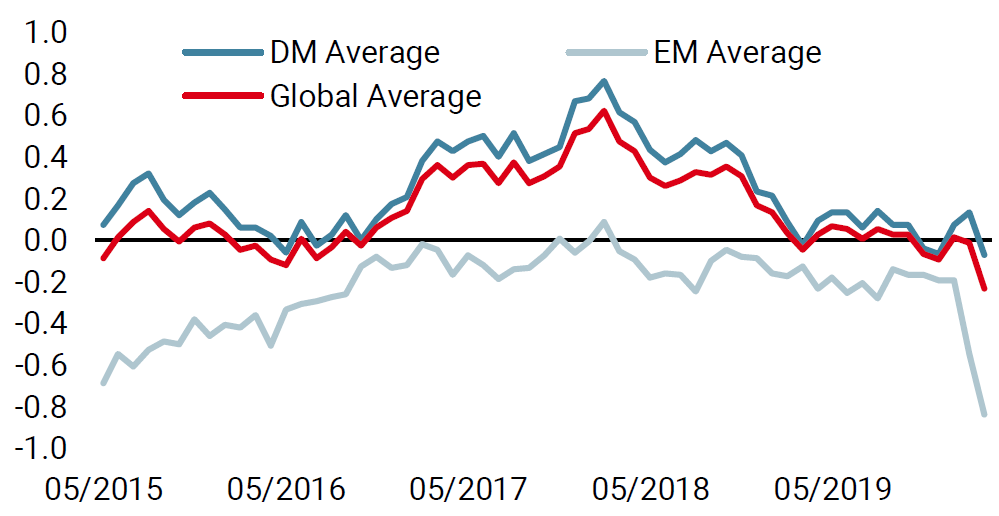

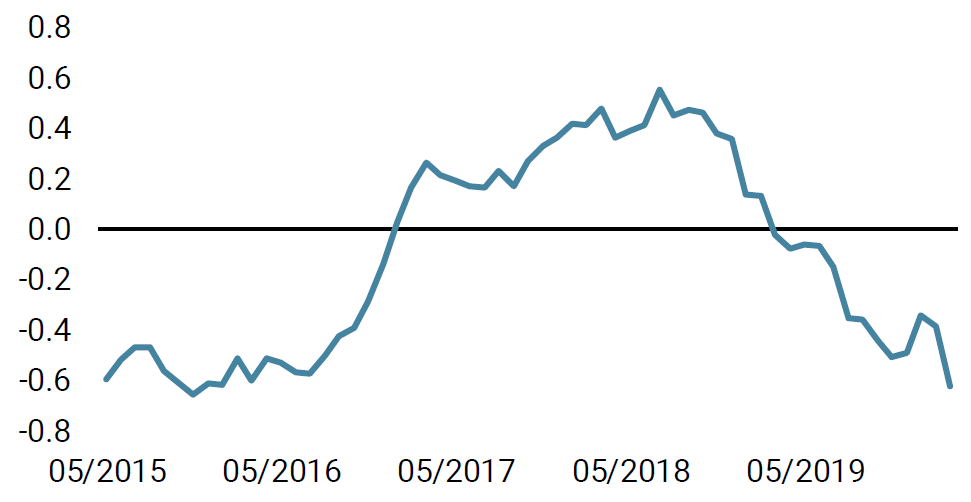

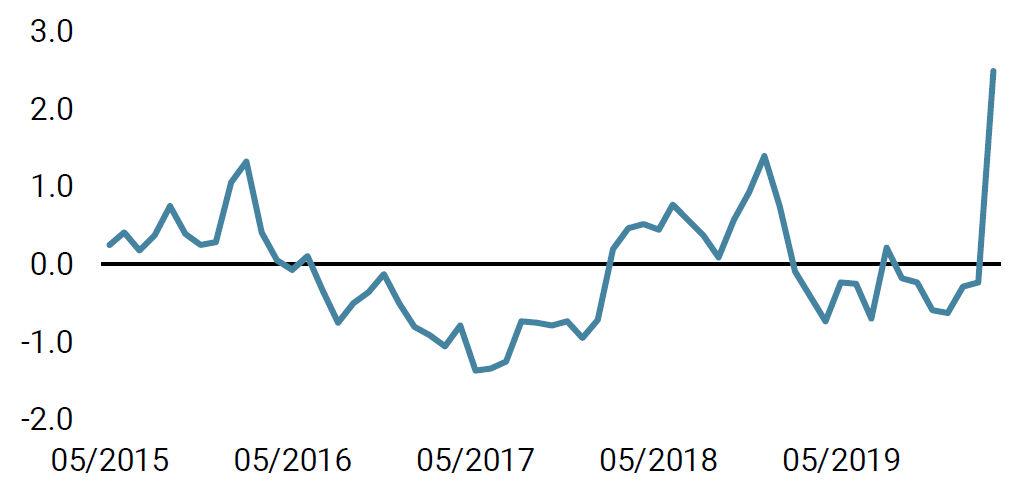

1. This shock is exogenous and comes surrounded by uncertainties. It creates a challenging situation that is far more complex than the collapse of the real estate market and/or financial markets in 2008 and 2001. Therefore, finding a solution is also much more of an uncertainty today than in previous crises. 2. Contrary to 2008, yields were low entering into the crisis. Central banks’ balance sheets are still large while sovereign debt has not had time to decrease significantly. This situation will limit the extent of fiscal stimulus for two reasons: first, debt is large enough for markets to be reluctant to take on more of it. Second, the ability of central banks to cap the evolution of yields is lower than it was in 2008: the element of surprise has passed and the medicine must be stronger than in the past to be successful. The increase in bond yields over the past two weeks is a symptom of that, creating a correlation shock as investors run to cash. 3. The current crisis is affecting every sector of the economy. With China, we first had a production shock, but with the spreading of the virus to the Eurozone and the US, this production shock is now being complemented with a demand shock. In 2008, the shock focused on the US real estate sector, spreading to the financial world. Today, the extent of the damage is broader. 4. Finally, the world is highly dependent on the level of interest rates and today there is a larger duration sensitivity than ever. Financial assets, GDP growth and social stability have largely benefited from the low bond yield environment of the past ten years. With the potential increase in sovereign debt, an increase in bond yields could be bad news for global markets, the economy and, more broadly, for households – Direct: in the US and other countries, plans to implement a direct fiscal spending programme to support growth and help SMEs survive the blow. – Loans: mainly in Europe, plans to lend money to the economy should it need it in order to limit the quantity of defaults. Government spending will need to be bigger than in 2008 in order to offset the current macro shock. Our core scenario is now a 5% contraction in global GDP over Q2 –a significant recession shock for the world economy. These contraction estimates could be increased further should the various quarantine periods be extended. From what most governments have announced so far, the numbers have not yet reached these levels except in the case of the US. The roles played by governments will be critical in determining the differences between countries. In the case of the US, a large-scale response can be expected, while for Europe it will be harder to spend significantly more. What has been announced in Europe so far is mainly a lending mechanism, not fiscal spending per se. According to our calculations, the impact should be in the range of USD 2.5 trillion of negative growth in the US and along the same lines in Europe. Currently, governments are offering about USD 2 trillion of direct measures and USD 1.8 trillion of loan-related measures. The problem is that much of the USD 2 trillion is actually coming from the US in the shape of a virus bill. We expect the bill to pass, but ex the US effort, other global governments are only expected to contribute around 10% of what is needed to offset the negative consequences of our core scenario. This, in our view, is not enough. Another key factor is that we are expecting the average investor to rush towards cash, creating an increased need for market liquidity. The Fed is currently providing this liquidity only in the US Treasuries market, leaving other markets exposed to rising liquidity risk. Investment solutions such as ETFs are likely to be hit hard, potentially creating gaps in market prices and adding to the current panic. What then could be the answer? In order to mitigate these concerns, a new type of “helicopter money” intervention would be necessary in our view: a revised version of TARP that would buy all assets including equities, ETFs and corporate high yield. The Bank of Japan has been doing something similar for a while and it should help, though no one can know if it would be enough. For now, our main fear on the economic front is for SMEs, the weakest part of economy and the one that will suffer the most from the crisis. SMEs represent a large part of employment, and thus consumption, and would only see limited benefit from monetary policy easing. The fiscal stimulus therefore needs to be large in order to make up for the limits of monetary policy. In 2008, the housing market was rates driven: today’s situation is much less sensitive to the policy tools of central banks (short and longer-term rates). 1. A significant improvement in terms of the health situation, meaning a slowdown in the growth rate of new COVID-19 cases. We are not there yet and, as we write this, it still is in the 20% range in Europe. 2. As explained earlier, a significant combination of fiscal and monetary policy stimulations, with all the challenges listed above. 3. A further drop in equities, in line with the extent of the current expected economic contraction. Historically, during recession periods, every percent of negative GDP growth implies about ten times the earnings growth contraction and a comparable change in the price of equities, as the next earnings become abnormally relevant to fixing the price of stocks. Only a sharper peak to trough negative equity performance would therefore be consistent with the 2008 sensitivities and our core macro scenario. None of these boxes are ticked for now. We could see a technical rebound, but its potential is likely to be short lived. Over the longer run, we think the combination of liquidity crunch and uncertain yet significant macro damage will weigh on most growth-related assets. We remain defensively positioned. World Growth Nowcaster World Inflation Nowcaster Market Stress Nowcaster Weekly Change Sources: Unigestion. Bloomberg, as of 23 March 2020.What’s Next?

This time it’s different

In our view, there are four key points that make this crisis different:The expected fiscal answer

This special situation calls for a special response and we now have more information regarding the different fiscal plans proposed by the countries affected. They are two kinds: direct plans and loan-based plans.A complex policy mix response

However, it will take time before this stimulus is felt in the economy. The announcement should reassure investors, but the genuine economic impact will take time to offset the loss in wealth and revenues worldwide due to the stringent social distancing measures. There is naturally a delay between the moment a financing bill is passed and the moment it goes into the pockets of households and SMEs – but this delay adds another layer of uncertainty that shrewd investors need to discount in their scenario.Three triggers to return to markets

Before returning to the markets and reducing our cash position, we would need to see three key triggers:Unigestion Nowcasting

Important Information This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person. The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor. Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore (MAS). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).