The last few weeks of trading have been driven by strong optimism regarding the strength of the economic recovery, pushing so called ‘re-opening trades’ higher while penalising asset classes and sectors most sensitive to rising inflation pressures. Rising rates have taken centre stage and questions about future central bank action are becoming increasingly urgent. How – and more importantly when – will central banks respond? Will they lag the curve? How credible is the “transient” rhetoric surrounding inflation fears?

Heavy Dream Rotation

What’s Next?

Uneven recoveries lead to different action plans

From a macroeconomic perspective, all the elements are in place for surging inflation pressures to continue for longer than central bank rhetoric would suggest, particularly the Fed’s. Given currently expected levels of growth, a traditional and historical view of the global fundamental backdrop would prompt a more hawkish tone from policymakers globally if it wasn’t for the level of uncertainty surrounding the future evolution of the pandemic. Exit strategies are unlikely to be as homogeneous as the global responses to the crisis, given the disparity in the pace and scope of the recovery across regions. Divergence in the responses of various central banks will be inevitable and with it relative value opportunities, or alpha plays, rather than beta, will open up.

US and Europe: a tale of two blocs

Due to structural differences in the way both continents execute monetary and fiscal plans, the expected pace of their economic recoveries and macro projections for the years to come are radically different. In its latest FOMC meeting, the Fed upgraded its growth forecast for 2021 from 4.2% to a stunning 6.5%, while realised inflation for the year is expected to exceed the central bank’s initial target without massively overshooting. Core PCE – the Fed’s preferred measure of inflation – is now set to 2.2% versus 1.8% at its December meeting. If this holds true and prices do not overshoot, it bodes well for the US economy overall and financial assets in particular. This would enable a smooth return to ‘normal’ monetary policies with an orderly surge in interest rates, one of the main risks in investors’ minds at the moment. However, we think that there is a risk that inflation pressures will be less transitory than expected, increasing the odds of the Fed sitting “behind the curve” and later being forced to change course more rapidly than projected. Base effects will push Q2 inflation prints to about 3%, while supply and demand imbalances could have a longer lasting impact on prices. We therefore expect tapering of asset purchases to happen more quickly than current pricing suggests, and liftoff in interest rates to take place earlier than the current projection of 2023. The trajectory of monetary policy in the US in the quarters to come can only become more hawkish and faster paced than currently projected.

Europe however is in a different situation. Inflation is expected to remain muted for a prolonged period while GDP growth and employment recover less rapidly than in the US. HICP inflation is now expected to top 1.5% by year-end before slipping slightly to above 1%, far from the ECB target of 2%. In addition, the risk posed by rising rates has a different taste in the old continent given the heterogeneity in fundamental dynamics across member countries. For this reason, the ECB has a more acute focus on rate surges. The central bank decided at its latest meeting that it would ramp up its weekly asset purchase operations under its PEPP programme to keep yields afloat and prevent an overshoot in sovereign financing conditions, which would otherwise weigh on the recovery at a very inopportune time. With lots of ammunition still available in the special pandemic programme, the aim is to increase asset purchases in the months ahead from an average of EUR 15bn a week to EUR 20bn a week: a completely different stance to its US counterpart.

These divergences have been confirmed by our proprietary Nowcasters for some time now. Growth has been running above potential in the US since September last year and in spite of a temporary slowdown in December and January. In contrast, European growth has remained at below potential levels and still struggles today, mainly due to slack in investment perspectives, consumption, and insufficient improvement in unemployment. In relative terms, the situation is expected to remain in favour of the US over the short term, especially given the recent evolution in the pandemic and the monumental disparity in the size of the fiscal stimulus between each side of the Atlantic. Indeed, total fiscal support now represents more than 12% of US GDP but ‘just’ 6% in Europe. This will have a huge relative impact over the medium term in terms of the pace of economic recovery and inflation pressures, as well as financing needs.

Where to look next: dispersion and relative value

Large rotations have already occurred in so-called ‘reopening trades’ since the beginning of the year, across and within asset classes. Pro-cyclical and certain inflation risk premia have been buoyed by better economic prospects, while duration has been hit hard by one of the fastest historical rate rises. Below the surface, small caps, Financials and Energy-related stocks outperformed while Tech suffered. The Russell 2000 index, considered one of the main proxies for improving growth prospects, has outperformed the S&P 500 by 14% as of 15 March, and by 12% in the US Financials sector. US bonds strongly underperformed their G7 peers, with 10-year yields up 80bps year-to-date versus only a 30bps rise in German Bunds, and fully in line with relative fundamental forces at play as described above. Last week saw partial unwinds in these big sectorial/relative value trades on the back of increased lockdown measures taken in response to what health officials fear to be a third wave of the pandemic. Moreover, these rotations coincided with quarterly rebalancing flows, a process that usually weighs on large outperformers and benefits laggards as asset managers return exposures to desired target levels.

In our opinion, this is only a temporary setback that opens up opportunities for the medium term. The trajectory of the pandemic remains positive: increasing demand from consumers will hit the real economy in the months ahead and growth remains solid. In the meantime, inflation remains underestimated by the investment community and central bankers. We believe that the environment is favourable for inflation-sensitive assets, such as breakevens and cyclical commodities. On the short side, we remain dynamically underweight duration, especially in US Treasuries as we believe the Fed currently sits behind the curve and could speed up its reaction faster than currently expected in response to any meaningful surges in inflation measures over the short run.

Unigestion Nowcasting

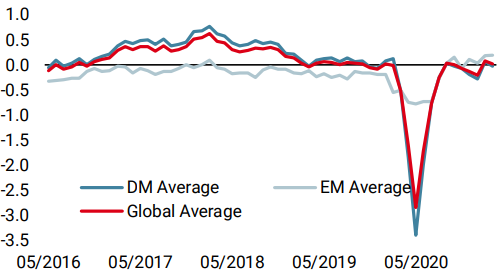

World Growth Nowcaster

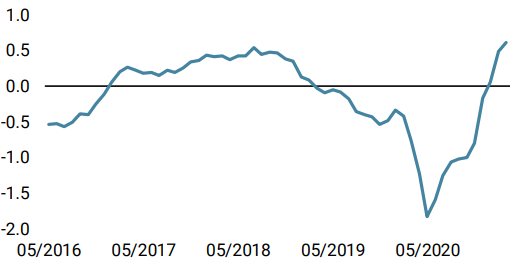

World Inflation Nowcaster

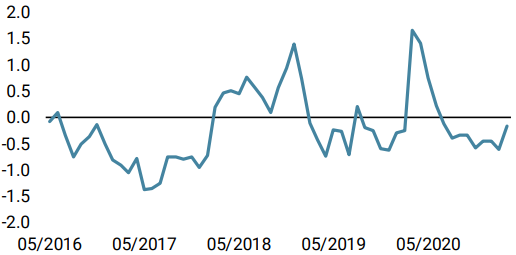

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster declined as US data showed a limited decline once again. The US Growth Nowcaster has now reached negative territory while remaining close to zero.

- Our World Inflation Nowcaster declined slightly as the majority of countries showed marginally less inflation-oriented data. Inflation risk is still very high.

- Our Market Stress Nowcaster increased across all its components last week: liquidity, spreads and more recently volatility. Market stress risk is high.

Sources: Unigestion. Bloomberg, as of 26 March 2021

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).