Macro Fundamentals Support A Risk-On Position

The new year has started with significant volatility, as central bankers make clear a shift in monetary policy that has seen long rates move sharply higher and questioned asset valuations. Assessing macro fundamentals today, we see a picture that is largely supportive, especially for growth assets: global growth has been stable at a robust level for some time, and inflation pressures are showing signs of stabilisation (if not reduction). While we expect monetary policy to normalise as policymakers contend with the inflation they were apt to dismiss just a few months ago, we do believe an easing of inflation later this year will rein in aggressive policy action. At the same time, the omicron variant looks less virulent than initially feared, and this fading risk should support our positive medium-term view.

Positivity

What’s Next?

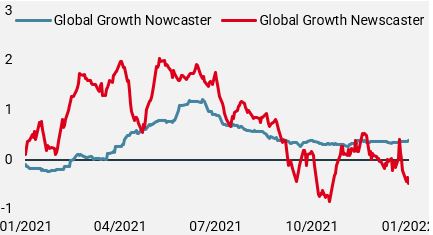

Global growth is solid and stable

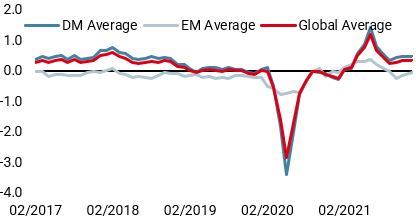

During the third quarter of last year, we saw a significant drop in economic growth as many of its supports faded without a strong consumption recovery. At the time, the deceleration was led by easing demand from the US and tighter policy slowing growth in China. However, since the fourth quarter of last year, global growth looks to have stabilised above potential, with a modestly improving picture in both US and China. Figure 1 shows the evolution of our two systematic indicators tracking global growth, the Nowcaster and Newscaster. Both of these indicators had fallen significantly from their July 2021 peaks but stabilised more recently. Importantly, the Newscaster, which is intended to be more reactive by incorporating news articles about the economy, has dipped again, following the Fed U-turn. The Nowcaster has seen most of its components decline and level off around potential, with the notable exception of Employment, which has steadily risen since October 2021.

Figure 1: Global Growth Indicators

Source: Bloomberg, Unigestion. As of the 12.01.2022

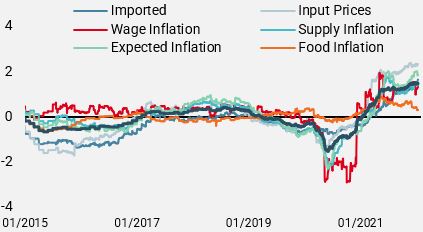

Lofty inflation pressures showing early signs of easing

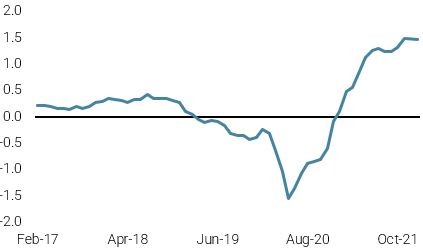

Inflation has become the key macro topic over the last few months, shifting from a “transient” phenomenon to one that central bankers now have in their cross-hairs. Wednesday’s US CPI print of 7% y/y was the highest in 40 years but matched economist estimates. Investors had apparently already priced in these inflation rates, as the market reaction was quite positive: bonds and equities both rallied, credit spreads tightened, and commodities continued moving higher. While there is no doubt that inflation pressures are still with us, we do expect them to subside over the course of this year due to easing supply bottlenecks, normalised demand, and the unlikelihood of prices surging as much as last year. Figure 2 shows our Global Inflation Nowcaster and its underlying components, most of which have stabilised at these historically high levels.

Figure 2: Global Inflation Nowcaster and Its Components

Source: Bloomberg, Unigestion. As of the 12.01.2022

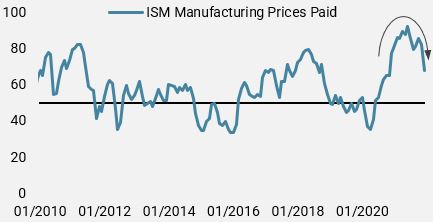

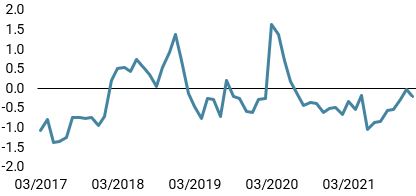

The US ISM report is a useful insight into the business climate, and over the last few months, there has been a turn in the Prices Paid survey: As Figure 3 shows, fewer firms report paying higher prices. While this does not mean prices are falling or set to fall in the near-term, it does indicate that a meaningful acceleration in inflation is unlikely, which would benefit many assets, once market participants adjust their expectations to cooling inflation.

Figure 3: ISM Manufacturing Report on Prices Paid

Source: Bloomberg, Unigestion. As of the 12.01.2022

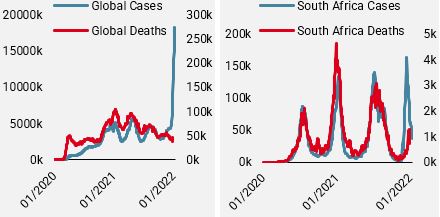

Omicron variant uncertainty fading

At the end of last year, we viewed the emergence of the omicron variant as a market stress episode rather than a genuine macro shock: there was too much uncertainty about the variant, its severity, and its resistance to the vaccines to make a clear call on its impact on the macro-economy. However, over the past few weeks, some of that uncertainty is clearing to the benefit of markets: while the variant is highly transmissible, even among vaccinated people, it looks to be much less severe than the previous variants. Figure 4 charts the week-over-week growth in confirmed Covid cases and deaths, where the deaths have been lagged by two weeks (given the typical time delay between diagnosis and death), for both the world and South Africa. As the two charts make clear, the explosion in cases has not led to an explosion in deaths (and indeed hospitalisations). While the sheer number of sick has been a drag, as many people need to stay home until they recover, it looks unlikely to have a more meaningful impact on economic growth and could even be a way for the pandemic to become an endemic. Taken within a context of healthy growth and the prospect of cooling inflation pressures, we believe the macro case for an asset allocation favouring risk, especially geared toward growth, should perform well in the current environment.

Figure 4: Covid Cases and Deaths

Source: Bloomberg, Unigestion. As of the 12.01.2022.

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster was steady as marginal improvements in US and Chinese data were offset by a slower growth impulse in the Eurozone.

- Our World Inflation Nowcaster was steady, with most countries displazing high but stable inflation pressures.

- Our Market Stress Nowcaster was slightly down over the week, as volatilities fell and spreads tightened.

Sources: Unigestion, Bloomberg, as of 13 January 2022

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).