When we look at financial market drivers, they paint a fairly positive picture for the next few months: global growth has recovered strongly as monetary policy remains accommodative in the absence of any meaningful inflation pressures. The fiscal impulse has faded but has largely been effective in supporting incomes. At the same time, positive news on a potential coronavirus vaccine points to lower uncertainty for households, businesses, and investors, which should not be underestimated. While we are concerned about declining valuations for growth-oriented assets, the rising number of coronavirus cases and ensuing restrictions is potentially a more imminent threat. In addition to monitoring health statistics, we are keeping a close eye on our Growth Newscaster, a fast-moving indicator that assesses reporting on economic growth. While there has been deterioration since the beginning of the month, it is currently confirming what our Growth Nowcaster is observing: the risk of a global recession is low, though there is dispersion across countries.

Break the News

What’s Next?

The challenges of exogenous and rapid shocks

The nature of the coronavirus crisis – an exogenous shock followed by a sharp global economic contraction and massive stimulation – has made it difficult to track with traditional macro data. Our own Growth Nowcaster, which has demonstrated its ability to give a timely read on economic growth, reveals the challenge: as the virus spread into Europe and the US in February, the macro data prints were still relatively healthy. Indeed, our Global Growth Nowcaster was essentially zero at the end of February, meaning that the global economy was growing in line with its long-term trend, as it had for most of 2019. As restrictions and lockdowns went into effect in early March, markets sold off but macro data did not reflect the extent of the contraction until the end of the month, as the data agencies compiled the necessary information. Thus our Global Growth Nowcaster took until 26 March to point to a severe risk of recession. While catching the start of a recession within a month is usually timely, the coordinated and unprecedented fiscal and monetary response announced at this time meant that the recession would likely be short-lived and marked the bottom of the market. The Growth Nowcaster continued falling from March until the end of May, and took until 18 June to see an ebbing of recession risk, as stimulation worked its way through the economy. By that point, the MSCI ACWI had already rallied 38% from its low on 23 March.

Alternative data is one way to meet these challenges

Before the pandemic, we developed new systematic indicators to track global growth and inflation using alternative data. We focused on using structured data extracted from news stories about macroeconomic conditions, hence ‘Newscasters.’ Only relevant news for a given economy’s growth or inflation dynamics are considered, and global indicators, along with respective diffusion indices, are computed in the same way that we construct our Nowcasters. However, the Newscasters exhibit important differences: they are only about 30% correlated to corresponding Nowcasters, exhibit a two to three month lead, but are also more volatile. Importantly, they caught turning points earlier than the Nowcasters.

The coronavirus crisis provided a clear out-of-sample test for these Newscasters, and they reacted well, in particular the Growth Newscaster. In mid-February the Global Growth Newscaster agreed with the Nowcaster: it was at a zero level. But by 28 February, it had deteriorated rapidly, indicating a very high level of recession risk. The indicator bottomed out on the 26 March and then started marching steadily up as the stimulus measures were announced. It is important to point out that these indicators are not built to pick up stories about the coronavirus, pandemics, or any health concerns. They focus purely on economic news. Thus, the deterioration in the indicator and its recovery was based purely on press reporting about the expected economic impacts of the coronavirus and the stimulus that followed.

What have you done for me lately?

As we have communicated recently, we believe the current context is positive for growth-oriented assets over a medium-term horizon but could be challenged in the short-term by the resurgence of coronavirus cases. European assets experienced these pains in late October as restrictions were imposed. While the latest numbers suggest a stabilisation or improvement in European countries, the US is experiencing record numbers of new cases and the death toll is reaching levels last seen during the depth of the crisis. New York City is shifting to online classes for schools and restrictions are likely to follow in other cities and states as the virus shows no signs of slowing down. 26 states have seen cases grow by more than 25% over the last week, including Texas (48%), California (54%), and Florida (40%). Together, these three states account for nearly 30% of US GDP.

It should not be surprising that our Growth Nowcaster continues to convey a positive picture: the global level is just above zero, though the US indicator has fallen into slightly negative territory recently. But given our expectations and recent experience, we are keeping a close eye on our Growth Newscaster. So far, the global level remains positive (0.2) but has deteriorated meaningfully from its recent high at the start of November (1.1). While the trend over the last few months remains positive, the short-term reversal over the last few weeks is worth digging into further.

Part of the recent deterioration is driven by Europe, where the Newscaster has fallen from 0.8 on 26 October to -1.0 today as news focused on the economic consequences of social restrictions. In the US, the indicator has fallen from a recent high of 1.3 on 5 November to 0.6 today. Importantly, news coverage is not focused solely on the surging virus but also includes likely fiscal policy of a Biden administration, Fed comments, and macro data releases. On the positive side and supporting the global indicator, economic news out of China remains strong: the indicator there has been oscillating between 1 and 2 since July and is currently at 1.7.

The Newscaster reflects our overall dynamic views: a positive trend over the medium term but short-term risks could be spoilers and lead to volatility in the days and weeks ahead. For now, we prefer to keep our medium-term views while managing the short-term risks through diversifiers and optional strategies. We will keep these hedges in place until we have clearer indications that the global economy is heading into the second leg of a double-dip recession or that a vaccine will be administered soon, allowing economies to normalise.

Unigestion Nowcasting

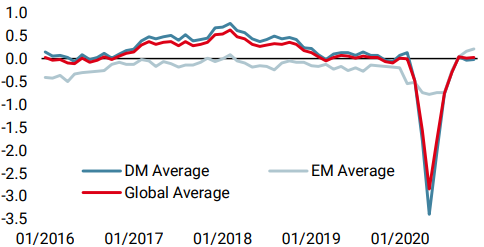

World Growth Nowcaster

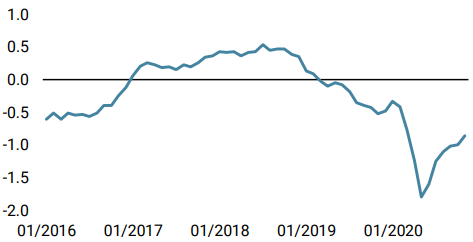

World Inflation Nowcaster

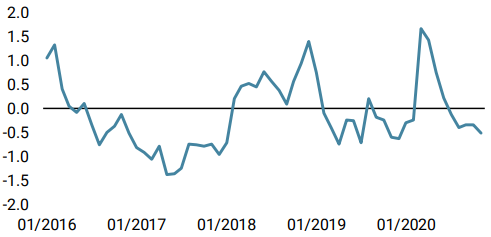

Market Stress Nowcaster

Weekly Change

- Our World Growth Nowcaster decreased last week, as US data remained positive but not as much as previously. Recession risk remains low for now.

- Our World Inflation Nowcaster increased: three out of five components in our US Inflation Nowcaster rose last week. Inflation risk remains neutral.

- Last week, our Market Stress Nowcaster remained unchanged globally as wider liquidity spreads (TED) were offset by lower implied volatilities.

Sources: Unigestion. Bloomberg, as of 20 November 2020.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore (MAS). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).