December capped off an extraordinary year for the world, with the global pandemic affecting nearly every aspect of life. In many ways, the month saw a continuation of the market trends that established themselves at the nadir of the financial crisis. Looking ahead into 2021, we see further upside for global growth as fiscal stimulus, easy monetary policy, and the vaccine rollout should support consumption and investment, which remained constrained in 2020. With this positive support for spending, we also expect bursts of inflation that will provide opportunities and risks in the year to come.

Don’t Stop ‘Til You Get Enough

What’s Next?

Markets continued their post-crisis trends in December

With vaccination programmes rolling out and a Brexit deal finalised (final approval should happen this month), December saw the environment for risky assets improve further. Equities benefited significantly, with the MSCI All Country World index (ACWI) up 4.6% on the month. US stocks continued their strong run, with the Russell 2000 rising 8.7% and besting the S&P 500’s 3.8% return. Despite some periods of strong outperformance, the value factor underperformed the market cap index, with the MSCI World Value returning 3.6% vs 4.2% for the MSCI World. Growth and Momentum continued to be the outperformers (4.9% and 4.3%, respectively), while Quality underperformed slightly (3.7%) and Min Vol lagged (2.1%). Emerging markets performed quite well with the MSCI EM index up 7.4% over the month while the JP Morgan EM Currency index rose 2.8% and the Barclays EM Hard Currency Aggregate index was up 1.5%.

High yield corporate bonds also posted strong performances, with the Barclays US Corporate High Yield index posting a 1.9% return on the month. Breakeven inflation rates rose as well, with the US 5-year breakeven inflation rate rising 27bps to 1.97%, as the price of crude rose 8% to 51.80 USD/bbl. The Bloomberg Precious Metals subindex was up 8.9%, with both gold and silver prices seeing strong gains on the month, though the Industrial Metals subindex rose only slightly at 0.3%. Despite the positive moves from both growth- and inflation-oriented assets, yields on government bonds remained steady with the Barclays Global Treasuries index posting a slightly positive return of 0.2%.

Growth may provide upside surprise in 2021…

As we head into the new year, we are starting to see an alignment of key drivers of market returns. This alignment suggests that global consumption growth in H1 2021 stands a good chance of exceeding expectations as the considerable stimulus unleashed by most governments has yet to manifest fully in the global economy. The G7 countries have injected 16% of their combined GDP according to the IMF (not including the recent US plan that amounts to 5% of the country’s GDP). There are two key observations to make here. First, the scale of the stimulation is unprecedented, approximatively 1.5 times larger than in 2008. Second, in contrast to 2008, a large group of countries responded with fiscal stimulus: the Euro area stimulation is larger while the Asian developing countries have done considerably more than what they did to address the consequences of the Great Financial Crisis. Where has the money gone? Mainly into savings, on both the consumer (US households’ disposable income has increased by 13.6%, for example) and corporate sides (across US companies, cash levels are up 2% of revenues). World consumption may be underestimated by many. Private economists expect 4.6% growth in consumption in both the US and in the Eurozone next year, which implies 2.4% and 3% in excess of their long-term trends, respectively. In our opinion, this is unlikely. Consumption is due to creep higher than those figures, especially in the US: above 5% consumption growth, either in H1 or over the year, would not surprise us.

With the further macro improvement, it is natural to ask if sentiment is already at full speed with investors expecting such a positive context. It is not, and that can be seen from multiple angles. First, in spite of the lower VIX now, the term structure of its futures remains upward sloping and the far end of the curve remains quite high by historical standards (the August 2021 futures were still about 26% at the end of December 2020). Second, the skew of the VIX curve, which indicates whether investors are insuring themselves against a drop or a rise in equity markets, remains strongly tilted towards downside protection. Finally, investor positioning on growth assets – especially among global macro hedge funds and CTAs – have a significant way to go before we can say that positioning has normalised. History teaches that this recovery could take time in spite of the violent V-shaped recovery that we witnessed last year, and the normalisation will also likely take time.

…which will naturally bring inflation pressures into focus

The most natural consequence to our higher-than-expected consumption growth ties to the evolution of inflation. Current inflation expectations for next year remain quite conservative: at the end of December, professional economists expected inflation of around 2% and 0.9% in the US and the Eurozone, respectively for 2021. The reflation of the world economy is expected to be slow and happen mainly over 2022. Official forecasts such as the Fed’s or the ECB’s are respectively 1.8% (in the case of the PCE) and 0.2% for 2021. We think that 2021 inflation could surprise for two main reasons. First, given our macro scenario, higher-than-expected consumption growth should eventually translate into higher prices. Given the historical relationship that binds both, 5% consumption growth alone could lead to around 3.5% inflation worldwide vs the 2.7% currently expected by economists. Second, the current scarcity level due to depressed production capacity (73% in the US and 76% in the Eurozone) could accelerate this process. With a rising willingness among consumers to spend money on fewer available goods and constrained service capabilities, the price-setting balance could tip in the direction of producers rather than consumers. This is a temporary and cyclical factor that will wane in the medium term but it should matter in 2021.

Overall, we have a positive view on risky assets given the continued economic recovery and expectation of further normalisation in sentiment. We also expect this positive environment to coincide with rising inflationary pressures, which may take some market participants by surprise. This is why we prefer a mix of both growth and inflation-oriented assets that should most directly benefit if our core scenario comes to pass.

Unigestion Nowcasting

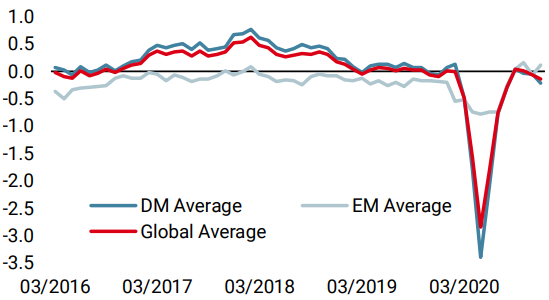

World Growth Nowcaster

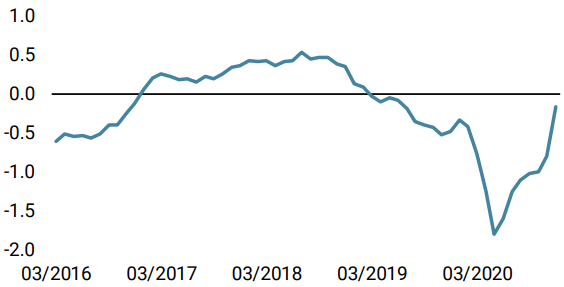

World Inflation Nowcaster

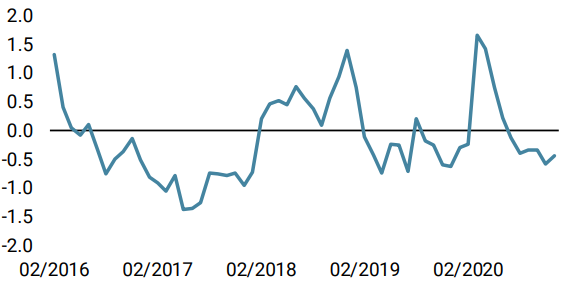

Market Stress Nowcaster

Weekly Change

- Our World Growth Nowcaster remained broadly unchanged last week. UK data posted significantly weaker signals following the Brexit deal.

- Our World Inflation Nowcaster also paused with inflation risk still being high for now.

- Our Market Stress Nowcaster declined as credit spreads reached lower territory.

Sources: Unigestion. Bloomberg, as of 04 January 2021.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore (MAS). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).