Key Points

- Both governments and consumers are increasingly committed to achieving emissions targets and changing behaviour.

- This is creating strong market tailwinds, which generate attractive investment opportunities with a measurable positive impact.

- At Unigestion, we have a proven ability in this segment of the market and are thus well placed to help investors capture these opportunities.

- The historic notion that environmental investing leads to lower financial returns is no longer true – returns and impact can go hand in hand.

Overview

The race to net zero has begun and the world as we know it has started to change. Countries, cities and companies have committed to reduce their greenhouse gas emission footprints, which shows that climate change is no longer the mere concern of environmentalists and NGOs.

From companies meeting the demands of shareholders through to consumers opting to buy organic products and switching to a more sustainable lifestyle, increased awareness of climate change has created a new market environment. The role of the financial services industry to provide capital has thus become more important than ever to drive this transition to a net zero economy and reduce pressure on natural resources. In particular, private equity will play an exceptional part in this transition, a responsibility that we welcome at Unigestion.

The Climate Tailwind

In a large-scale survey conducted by the UN Development Programme in 2021, two-thirds of the 1.2 million respondents considered climate change as an emergency and called for decision makers in the public and private sectors to step up and take action1. Thus, environmental concerns are part of the general thought process and consumer behaviour across the world is changing. People have begun to embrace sustainable living and want products and services that align with their personal values. With access to more information than ever before, consumers research the type of companies they want to support and products they want to purchase, basing shopping decisions on more than just price. It should therefore come as no surprise that the number of eco-friendly/sustainable products and services have risen significantly and that one-third of global consumers are willing to pay a premium2. This changing environment creates future challenges but also opportunities – a new kind of market tailwind.

As a longstanding private equity specialist, Unigestion has identified three significant areas which highlight the role of private equity when addressing climate change and environmental concerns in the market:

- Entrepreneurship: Structural change across industries and technological innovation in the sustainability space is driven by entrepreneurial growth typically rooted in private companies.

- Flexibility: Private companies have high control over decision processes and are more agile in implementing change. This flexibility allows them to adjust their sustainability journey and react quicker to changing consumer needs.

- Innovation: Developing solutions to replace “brown” technologies or environmentally harmful products requires innovative thinking and private companies are equipped to drive innovation in business models/services.

Climate change is about more than just switching to renewable energy as sectors from transport through to construction will provide many attractive investment opportunities.

Climate Impact: The Investment Opportunity

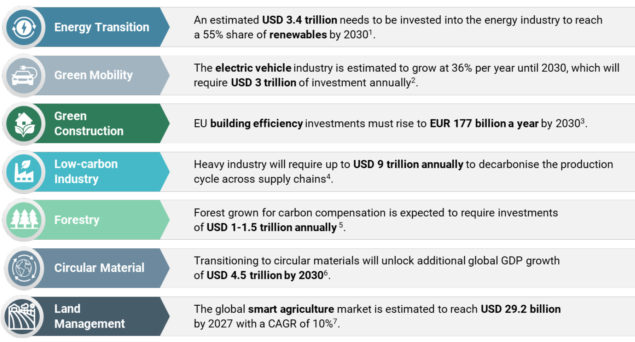

Considering the aforementioned demand, estimated investment needs in low-carbon sectors are very high. It will take more than just switching energy supply from fossil fuel to renewable sources – governments and businesses will need to change their operational model along the entire production and consumption cycle. As an example, energy efficiency retrofits of building infrastructure has the potential to save up to 80% of energy use and will require EUR 177 billion a year in the EU alone. In the transportation sector, we have entered new territory with the “Great Electrification”, which will require at least USD 3 trillion a year until 2030. Finally, transitioning to a circular economy will not only reduce pressure on natural resources but also stimulate growth and jobs.

Figure 1: Opportunities in Climate Change

Source: 1Frost & Sullivan Report Growth Opportunities from Decarbonisation in the Global Power Market; 2IEA Sustainable Development Scenario; 3EBRD Green Building Investments; 4International Energy Agency 2019; 5World Bank Report 2020 Pension Fund Investments in Forestry. 6World Business Council for Sustainable Development CEO Guide to the circular economy; 7 Valuates Report “Smart Agriculture Market by Global Opportunity Analysis and Industry Forecast, 2021–2027”.

In the following sections, we take a closer look at three sectors where private companies will play a significant role over the coming decade.

Green Mobility

In 2020, at least 53% of global petroleum consumption was used to meet 94% of energy demand in the transportation sector, including shipping, aviation, passenger vehicles, and freight. While the aviation sector remains difficult to decarbonise, road transportation has experienced significant innovation over the past decade, given its vital investment needs. Battery powered electric vehicles (EVs) emit no tailpipe emissions. Along with the constant expansion of renewable energy, EVs are therefore a sustainable alternative for the road transportation industry. Global EV sales reached 6.75 million units in 2021, 108% higher than in 2020, with 370 different electric car models available for purchase3.

Further innovation has taken place in the development of fuel cell vehicles as hydrogen-powered electric motors are already widely used in the public transport sector. North America is a fast-growing market for hydrogen with a large number of hydrogen fuel stations already fulfilling needs and the market is projected to grow at a CAGR of 62% until 2028. Other alternative fuels are also being developed as potential solutions to replace the use of petroleum, such as biofuel made of plant materials or animal waste, and its production is forecast to increase by 25% per year over the next five years.

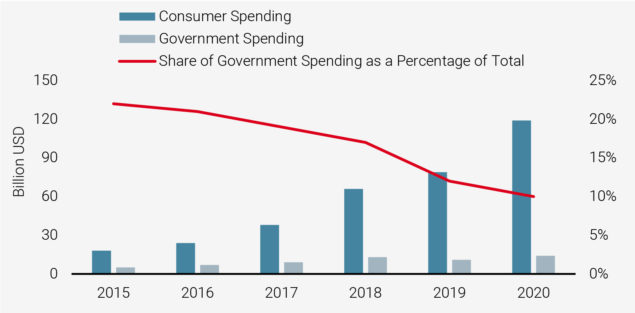

All of the above innovations have wide implications for investors and asset managers worldwide, not only because of the required capital but also due to a changing regulatory environment in favour of more sustainable standards. Vehicle emission standards and carbon tax will increase costs in the petroleum-based transport sector, while investments in green mobility allow investors to avoid transitional risk and benefit from long-term change. Figure 2 demonstrates how consumer spending increased substantially between 2015 and 2020, while government intervention steadily decreased. This situation can be compared with the early stages of the renewable energy market 15 years ago, which has now matured.

Figure 2: Consumer and Government Spending on Electric Cars 2015 to 2020

Source: International Energy Agency, “Trends and Developments in Electric Vehicle Markets”, 2021.

Regional differences mean the entire value chain needs to be considered when implementing decarbonisation measures to reduce pressure on the environment.

Agriculture

Agriculture accounts for a large proportion of global greenhouse gas emissions, varying significantly across regions. While it can make up to 40% of emissions in Sub-Saharan Africa, it “only” accounts for around 10% in North America and Europe. Thus, the entire value chain needs to be considered when implementing decarbonisation measures and reducing pressure on the environment.

Traditional farming has experienced radical transformation due to an increasing uptake of smart farming solutions. Agri-tech helps to meet growing food demand while decreasing the impact on the environment by web-enabled smart devices which can monitor soil for light, humidity, temperature, moisture, and health. Estimates suggest that the agri-tech market will grow at a CAGR of 10% until 20274.

Nevertheless, even the best technologies will be of no use if we cannot address soil fertility loss and water scarcity, since agriculture irrigation accounts for 70% of water use worldwide. Urban farming technologies enable plants to grow in hydroponics, needing no soil and saving water, as the roots of plants are submerged in liquid solutions containing all the needed macronutrients, such as nitrogen, phosphorus, and sulphur. The global hydroponics market is expected to grow at a CAGR of 20.7% between 2021 and 20285.

There are a wide range of approaches to minimise the negative environmental footprint of agriculture and to make a positive impact. Such activities include, but are not limited to, efficient use of resources such as water, replacement of chemical fertilisers, and reduction of greenhouse gases through carbon sequestration and supply chain decarbonisation.

The re- and upcycling of waste, the reuse of materials and the life extension of products will all be significant in the transition to a low carbon economy.

Circular Economy

When closing the loop in the fight against climate change, it is critical to reduce the consumption of resources. The re- and upcycling of waste, reuse of materials and life-extension of products can have a significant impact in the push toward a low carbon economy. With rising population growth and increasing consumption, landfills have quickly reached their capacity limit, and global waste is expected to grow to 3.4 billion tons annually by 20506.

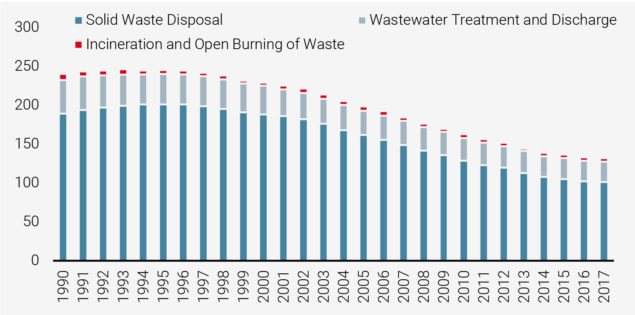

The impact of recycling is significant for the climate. Figure 3 depicts how greenhouse gas emissions from waste have fallen by 42% in the EU due to the uptake of recycling. The amount of emissions released depends on the type of waste and how it is treated. If organic material is disposed in landfills untreated, methane is released during the decomposing process, which is 25 times more potent in trapping heat in the atmosphere than carbon dioxide. Therefore, the more litter is recycled, the less of it is landfilled, resulting in less greenhouse gas emissions.

Figure 3: Greenhouse Gas Emissions of Waste Management

Source: EEA. Million tonnes of CO2 equivalent, EU-28 1990 to 2017.

Opportunities for investors are therefore growing vastly in the waste sector. Waste-to-energy technologies, in which non-recyclable waste is treated to produce electricity or heat, are proven technologies that have been implemented for decades. The rapid development of the recycling market is projected to continue in the coming years and is expected to reach a market size of USD 715 billion by 2030, witnessing a CAGR of 6.1%7.

The notion that impact investing comes with a trade-off of lower financial returns is based on misleading assumptions.

Can Returns and Impact Go Hand in Hand?

In the past, the inclusion of sustainability or impact within an investment portfolio was presumed to lower financial returns. However, this notion was based on misleading assumptions. Historically, exclusionary screening has been the oldest form of sustainable investing, dating back to the 18th century and practiced by religious groups that aligned their portfolios with their personal values. Investments in certain industries, for example ammunition, were therefore excluded and resulted in the loss of returns that derived from that particular industry.

Impact investing has grown in awareness over the last 20 years, but in the eyes of some financial market participants it still comes with a trade-off. In their view, the greater the positive social or environmental impact, the lower the financial returns as impact investors are ready to invest for below-market returns, in line with their impact objectives.

Today, meeting financial return expectations while generating positive social and environmental impact has developed into a sophisticated investment approach. With society facing extreme weather events and resource scarcity, the market demands new solutions. As already explored, these strong market tailwinds are generating attractive investment opportunities with a measurable positive impact, such as greenhouse gas reduction, biodiversity conservation, or water efficiency.

Unigestion’s private equity team has a proven track record in delivering solid returns through climate-related investing.

Unigestion’s private equity team has long recognised the importance of environmental responsibility within its investment strategy, launching its first environment-focused fund in 2010 and an ESG-focused mandate for a large client in 2014. To date, we have generated a 2.5x TVPI and 20% net IRR on realised climate impact deals8.

Going forward, we believe the following “green drivers” will lead to outperformance in climate impact investments:

- High demand for low carbon solutions: Sustainable products/services are in high demand and have been widely adopted as a substitute for incumbent products over time. The sharp increase in customer demand drives growth by increasing revenues and market expansion.

- Pricing power: “Green” products can command higher pricing power, leading to higher margins. Indeed, studies confirm that people are ready to pay more for a “green” product. The products or services can also bring material cost savings such as through energy efficiency, lower regulatory costs (e.g. lower carbon taxes), reduced risks of fines, and enhanced productivity.

- Lower financing costs: “Green financing” is available at a lower cost for companies with environmental products or services.

- Strategic premium: For all the reasons mentioned above, private companies with sustainable products or services will ultimately be in high demand by investors and/or larger companies wanting to increase exposure to climate impact strategies.

Conclusion

Unigestion’s motivation to launch a dedicated Climate Fund is driven by two equally important reasons. First, we know the market well. As explored in this paper, there is a strong shift in capital requirements to spur the transition to a low-carbon economy and satisfy consumer demand, where the private sector will play a significant role. Our team has access to those high growth and innovative companies via multiple channels and knows what it takes to create value while simultaneously achieving attractive returns and measurable impact. Second, investors are increasingly bound to include climate-positive investments in their portfolios, spurring the uptake of environmentally-friendly measures while de-risking away from the potential of stranded assets. As a result, the ‘Net Zero Investment Framework’ was defined by large-scale investors, identifying five core components of a net zero investment strategy to achieve the 1.5°C temperature goal set by the Paris Agreement.

We believe we can have a greater impact by specialising and deepening our focus on this theme, as we not only see an opportunity for generating attractive returns for investors, but also better outcomes for society and the environment. During our 10+ years of experience in climate investing, we have already been able to demonstrate the attractiveness of the sector.

1,International Public Opinion on Climate Change, January 2021

2,Global Sustainability Study 2021, Simon-Kucher & Partners

3,International Energy Agency, “Trends and Developments in Electric Vehicle Markets”, 2021

4,Valuates Report “Smart Agriculture Market by Global Opportunity Analysis and Industry Forecast, 2021–2027”

5,Market Analysis Report 2021 “Hydroponics Market Size, Share & Trends”

6,The World Bank A Global Snapshot of Solid Waste Management to 2050

7,Waste Management Market by Waste Type & Service – Global Opportunity Analysis & Industry Forecast, 2021 – 2030

8,Performance data based on five investments that were realised between September 2016 and October 2019. Past performance is no guide to the future, the value of investments can fall as well as rise, there is no guarantee that your initial investment will be returned. Performance is shown gross of fees, thereby the inclusion of fees, costs and charges will reduce the overall value of performance.

Important information

Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed by recipients to any other person. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in the investment vehicles to which it refers. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Please contact your professional adviser/consultant before making an investment decision.

Where possible we aim to disclose the material risks pertinent to this document, and as such these should be noted on the individual document pages. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Unigestion maintains the right to delete or modify information without prior notice. Unigestion has the ability in its sole discretion to change the strategies described herein.

Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors.

To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

No separate verification has been made as to the accuracy or completeness of the information herein. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of information from third party sources. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Legal Entities Disseminating This Document

UNITED KINGDOM

This material is disseminated in the United Kingdom by Unigestion (UK) Ltd., which is authorized and regulated by the Financial Conduct Authority (“FCA”). This information is intended only for professional clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients.

UNITED STATES

This material is disseminated in the United States by Unigestion (UK) Ltd., which is registered as an investment adviser with the United States Securities and Exchange Commission (“SEC”). All inquiries from investors present in the United States should be directed to clients@unigestion.com at Unigestion (UK) Ltd. This information is intended only for institutional clients and qualified purchasers as defined by the SEC and has therefore not been adapted to retail clients.

EUROPEAN UNION

This material is disseminated in the European Union by Unigestion Asset Management (France) SA which is authorized and regulated by the French “Autorité des Marchés Financiers” (“AMF”).

This information is intended only for professional clients and eligible counterparties, as defined in the MiFID directive and has therefore not been adapted to retail clients.

CANADA

This material is disseminated in Canada by Unigestion Asset Management (Canada) Inc. which is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario, Quebec and Newfoundland & Labrador. Its principal regulator is the Ontario Securities Commission (“OSC”). This material may also be distributed by Unigestion SA which has an international advisor exemption in Quebec, Saskatchewan and Ontario. Unigestion SA’s assets are situated outside of Canada and, as such, there may be difficulty enforcing legal rights against it.

SWITZERLAND

This material is disseminated in Switzerland by Unigestion SA which is authorized and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”).

Document issued March 2022.