PRIVATE EQUITY INVESTMENT INSIGHT

This case study of Euromed provides an insight into the types of private equity direct co-investments that Unigestion makes. It also shows how we create value and how we decide to exit an investment.

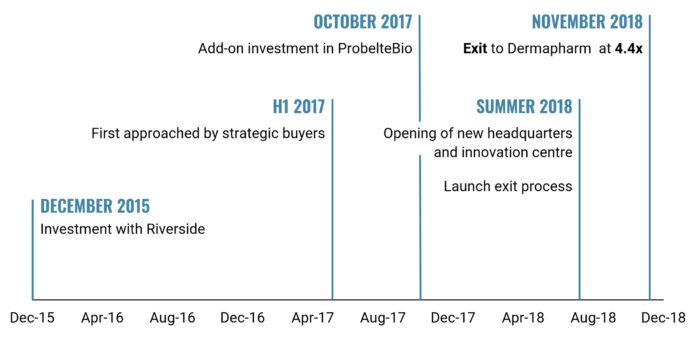

We acquired Euromed in December 2015 from Meda, a Swedish pharmaceutical company seeking to divest its non-core business, and sold it in December 2018 to the German company Dermapharm Holding SE for a multiple of 4.4x cost.

- Within our direct co-investments, we look for firms whose growth is underpinned by long-term trends

- Our aim with Euromed was to consolidate its position as a market leader by diversifying revenues across customers and geographies

- One of the key factors behind our success was our ability to take an observatory seat on the company’s board to help their growth strategy

About Euromed

Euromed was founded in 1971 and is a Spanish supplier of herbal extracts and natural active substances that are used as key ingredients in the phyto-pharmaceutical and dietary supplements industries. The company processes more than 5,000 tonnes of raw materials per annum, extracting around 600 tonnes of high-quality products at its manufacturing plants near Barcelona and Murcia, Spain. Its client base is made up of more than 300 customers in 35 countries.

- Investment Date: December 2015

- Strategy: Buy and build buyout

- Exit Date: December 2018

- Realised Multiples: 4.4x MOI (60% IRR)

Why Did Unigestion Choose to Invest in Euromed?

At Unigestion, when we make direct co-investments, we are looking for companies whose growth is underpinned by long-term trends. At the time of our acquisition, we were confident that Euromed would be well positioned to profit from the trends of healthier living and an ageing population. Furthermore, we considered the barriers to enter the company’s market to be high, because it would take a new entrant a lot of time to establish production and technical know-how, expertise in regulation and quality standards as well as customer relationships.

We are also looking for small and mid-market companies which are resilient in their own right thanks to a solid market position, management and financials. At the time of our acquisition, Euromed was a global leader in its field. It was recognised for the quality of its products. And it was appreciated by its clients for its ability to offer tailor-made as well as off-the-shelf products. While the company had enjoyed steady growth and solid profitability, our analysis highlighted multiple avenues for further growth. We were confident that, if we were able to deliver on Euromed’s potential, the company would appeal to both strategic and financial buyers.

What Avenues for Further Growth Did You Identify?

We identified several avenues of growth. One such opportunity was to increase production capabilities by introducing an additional shift and installing a further production line. In addition, an expansion into the North American and Asian markets through add-ons would allow the company to further increase its production capacity. By growing in the dietary supplement market in North America and Asia, Euromed’s customer base could be increased and more diversified. Further developing the product portfolio with olive extract and grape seed would result in the business growing at a faster pace. Finally, we also identified potential to strengthen and incentivise the management team as well as to improve the operations of the company.

Why Did You Choose Riverside as Your Investment Partner?

The Riverside Company is a global private equity firm with more than 30 years and 560 transactions to their name. They focus on taking controlling and non-controlling stakes in growing businesses valued at up to USD 400 million and have extensive experience in healthcare investments, having completed 85 deals in this space, including supplement and pharmaceutical companies. They know how to drive growth by boosting production, improving operations and continuing to invest in research and development. Given this, and the potential that we saw in Euromed, they were a natural partner for us to invest alongside.

How Did Unigestion and Riverside Create Value at Euromed?

Many ingredients are necessary to create long-term value. Euromed’s success lay primarily in its dedicated management, consisting of Xavier Roig and his team, who did a fantastic job in propelling the company to the next level. I was impressed to see how well the combination of a) strong management and board, b) clear strategy and c) strong market fundamentals enabled this deal to have such a positive outcome.

A key initiative we undertook was the building of a new research and development centre at Euromed’s headquarters in Barcelona. This was equipped with the latest laboratory equipment and allowed us to implement a structured product development process. This ensured that the sales team was able to offer customers new products and applications for the extracts that they already commercialise and to develop new ones.

Another key value driver was the purchase of Probelte Biotecnología in October 2017. Probelte’s strengths were in water-based extraction and purification processes and they complemented well Euromed’s existing strengths in solvent-based extractions. The acquisition helped expand production capacity by 30% and increased the product offering in dietary supplements and functional food ingredients. For example, some of the new product additions were a fresh pomegranate extract and an extra virgin olive extract. Overall, the purchase of Probelte created significant value, synergies and improved production capacity, and helped underpin Euromed’s growth.

In addition, we were able to implement several operational changes including improvements to the working capital.

One of the most important factors for Unigestion to be able to support Euromed’s growth strategy was the observatory seat on the company’s board. This allowed us to get close to the business, understand its needs and identify the best approaches to take to meet Euromed’s needs

How Quickly Did Your Actions Bear Fruit?

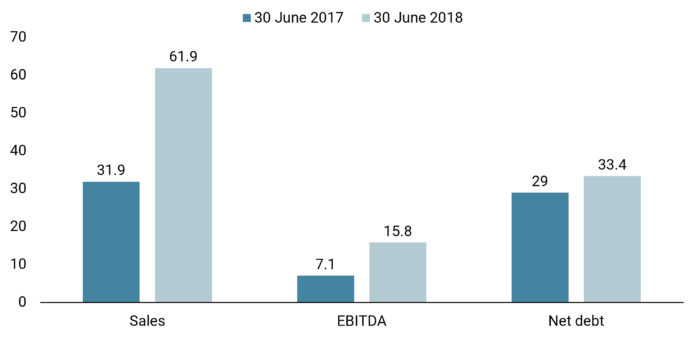

The initiatives identified and implemented, combined with the acquisition of Probelte, helped Euromed significantly improve its financial performance in 2018 compared to 2017. As a highlight, sales grew markedly, while earnings more than doubled. And all this happened with only a small increase in the company’s net debt.

Figure 1: A Strong Improvement in Financials (EUR millions)

What Was the Rationale for Exiting the Investment?

Given the success of the business and subsequent interest, we decided to sell earlier than had been originally anticipated.

When we invested in Euromed, we did so with the aim of reinforcing and consolidating its position as a market leader by diversifying revenues across customers and geographies, particularly in the US and Asia. This would help enhance the company’s strategic value to trade buyers. Given the stability of the business, its attractive financial profile and its high cash generation level, all of which were further enhanced during our investment period, Euromed also became increasingly attractive for financial investors aiming to further develop the asset.

In 2017, Unigestion and Riverside were approached by a number of potential buyers who had been impressed by Euromed’s rapid growth. Given the interest, we decided to sell earlier than had been originally anticipated and initiated our exit process in the summer of 2018. Within just six months, we closed the transaction through a sale to Dermapharm, a strategic buyer.

How Did the Investment Outcome Match Your Expectations?

Our investment in Euromed came to fruition early on, with management constantly over delivering on both targets and budgets. In addition, the company’s strong and confident partnership with its new shareholders allowed it to grow at a faster pace than had initially been anticipated.

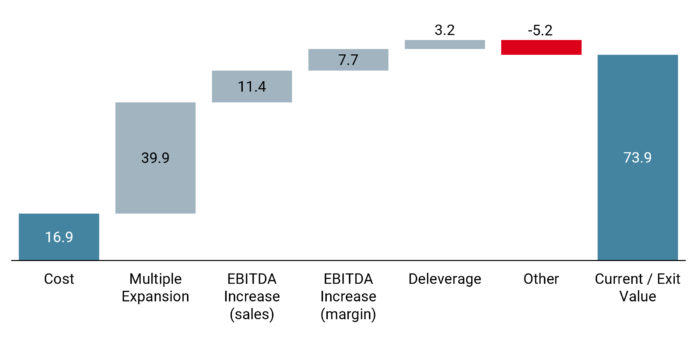

The strengthening of the team, complemented by a strong board and the initiatives launched by the shareholders, allowed the company to consistently exceed the initial strategic plan of its new investors. The materialisation of the value creation pillars, shown below, came earlier than expected and allowed management and shareholders to anticipate the timing for exit.

Figure 2: Value Contribution Bridge (EUR millions)

Timeline

Important Information

Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed by recipients to any other person. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in the investment vehicles to which it refers. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Please contact your professional adviser/consultant before making an investment decision.

Where possible we aim to disclose the material risks pertinent to this document, and as such these should be noted on the individual document pages. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors.

To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of this information. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

No prospectus has been filed with a Canadian securities regulatory authority to qualify the distribution of units of these funds and no such authority has expressed an opinion about these securities. Accordingly, their units may not be offered or distributed in Canada except to permitted clients who benefit from an exemption from the requirement to deliver a prospectus under securities legislation and where such offer or distribution would be prohibited by law. All investors must obtain and carefully read the applicable offering memorandum which contains additional information needed to evaluate the potential investment and provides important disclosures regarding risks, fees and expenses.

Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA). It is also registered with the Securities and Exchange Commission (SEC). Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion Asset Management (France) S.A. is authorised and regulated by the French Autorité des Marchés Financiers (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is regulated in Canada by the securities regulatory authorities in Ontario, Quebec, Alberta, Manitoba, Saskatchewan, Nova Scotia, New Brunswick and British Columbia. Its principal regulator is the Ontario Securities Commission. Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore.

Document issued June 2019.