Global equities declined sharply last week leading to a negative return in January (-0.45% for MSCI AC). Despite this correction, the consensus for this year remains unchanged: a rebound in the global economy, greater political stability and a policy mix that is still very accommodating are creating a very favourable environment for growth assets. While we share these views for the medium term, it remains important to assess the extent to which asset prices, formed by expectations, are moving away from fundamentals, and the extent and speed with which they are doing so. Such an analysis reveals that some markets have seen their risk reward deteriorate recently, prompting us to moderate our overweight in short-term growth assets and neutralise our bet on “reflation”.

Wicked Game

What’s Next?

On the macro front, everything looks solid…

From a macroeconomic perspective, momentum remains positive thanks to unprecedented fiscal and monetary support. The rapid arrival of several vaccines should also lend support to a strong and broad recovery in the global cycle. Thus, last week, the IMF revised their growth forecasts for the world economy upwards for 2021, forecasting growth of 5.5% after a contraction of 3.5% expected for 2020. Such a rebound should lead companies to restore their profitability and households to spend.

Q4 earnings results highlight the positive effects of this cyclical rebound. Only 30% of companies in the S&P 500 index and 10% in the Eurostoxx 600 have published their results so far but the figures show a high level of surprise for both profits and sales. On average, profits have grown by 4% on a year-on-year basis while sales show yearly growth of 1% for US companies and respectively of 9% and -4% for European companies.

The strong rebound in global trade, ongoing since June 2020, also confirms that the second containment cycles had less of a negative impact on activity because the measures were more targeted and only concerned certain economic zones. Combined with a new fiscal stimulus in the US of around 10% of GDP, all these elements should lead us to remain largely overweight growth and real assets. However, while fundamentals, whether they be macroeconomic, microeconomic, budgetary or monetary, are the main drivers of asset returns over the medium term, they are not the only factors that can affect the markets. Valuation, positioning and market sentiment are also important factors to take into account in a dynamic asset allocation.

… but beneath the surface, we see some initial signs of irrational exuberance

Analysing the performance of assets, their sectoral and geographic dispersion combined with the dynamics of positioning and valuation, is very instructive for assessing market sentiment and attendant risks, their horizons and their probability of occurrence. To be clear, we do not anticipate another recession or a wave of bankruptcies in 2021. The elements cited above are strong and sustainable enough to avoid such a scenario. In the short term, however, we see some signs of “irrational exuberance” which, if they were to persist and expand into larger market segments, could pose major positioning and valuation risks. What are these signals and which markets are affected?

- Some markets are showing extreme valuations with an unsustainable performance velocity. These include the IPOX SPAC index, the Renaissance IPO index, Cryptomoney (Bitcoin and Ethereum), certain penny stocks or securities related to the “renewable” theme (TXCT and ERIXP indices). Most of the above exhibit annualised returns of over 100% over a few weeks / months and have seen their implied volatility explode. Historically, price acceleration is a part of our bubble check list;

- The gross and net leverage of long/short equity strategies has increased significantly and remains high historically even after the de-grossing seen last week (around 62% for net leverage and in the 83rd percentile since 2010 according to Morgan Stanley);

- The ratio between calls and puts traded on US equities also remains at alarming levels with an excess of call vs put volume;

- The market reaction to “earnings beats” has been negatively asymmetric for US corporates, suggesting that expectations were too high.

One could argue that these elements are not so dramatic because they are specific to hedge funds and limited to very specific markets. Indeed, the current consensus view is that these factors are idiosyncratic risks rather than systemic. Nevertheless, other elements, more typical in their amplitude of change and related to broader markets, have also moved and raise questions about “speculative” market sentiment:

- Our Market Stress Nowcaster has gone from showing a very low risk to a high risk within just a few days;

- Credit spread levels, especially in the High Yield segment, do not reflect the scale of the increase in debt observed in 2020 and highlighted by the IMF report;

- The VIX curve remains inverted and the spread between implied volatility and realised volatility continues to widen;

- Short positions on the US dollar are at an extreme level, accentuating a risk of correlations in the event of a short-term correction in equity markets;

- Dispersion within equities has been very high as shown by the realised correlation index of securities on the S&P 500, which remains close to lows last seen in January 2018 and January 2020. Last week saw the worst relative performance by far for Crowded Longs versus Crowded Shorts since at least 2013. Moreover, our sectoral dispersion indicator that tracks the monthly performance of S&P 500 sectors points to a level of dispersion not seen since 2008.

What could be the next step?

At this stage, the bullish consensus view holds that the risk of contagion, which would imply a greater de-leveraging, will remain very limited because: 1) the exposures to risky assets of both long-term investors and systematic strategies remain moderate; 2) the P&L accumulated during the last six months should provide a cushion to avoid a negative feedback loop; and 3) implied volatility, which is still very high, should fall.

Without overestimating the short-term elements mentioned previously, we believe that the risk of broader de-grossing is greater than current pricing for two reasons. On the one hand, cross-asset exposures have changed a lot for systematic strategies: the beta to sovereign bonds, commodities and dollars has reversed significantly from “defensive” to “risky” over the last few months, implying that the de-risking / de-grossing threshold could be much closer than assumed by taking equity momentum as the only driver of risk management. Indeed, correlation effects could amplify the downside participation in an equity correction due to short positions on T-notes and the US dollar, as well as long positions on commodities.

The second reason is more structural and concerns the regime of volatility. In their famous paper on economic cycles, Stock and Watson1 link the volatility of assets to that of economic macro data, observing that the more stable and “controlled” the economic cycle, the lower the risk of economic “overshoot”. This in turn leads to a lower risk of economic shock and lower asset volatility.

The magnitude of the 2020 economic shock pushed the volatility of macro data such as industrial production, inflation, ISM or retail sales to levels not seen in previous shocks. We also saw this increase in macro volatility in our Nowcasters for the different countries we track. In addition, given the unprecedented amount of liquidity injected into the economy, reflected by the 25% increase over one year in the US money supply (M2), and which has mainly flowed into household and corporate savings, the risk of inflation remains high and higher than in recent years. Historically, inflation shocks have always been accompanied by an increase in the volatility of macroeconomic aggregates. We therefore believe there is little chance of a return to a regime of low asset volatility, such as that observed between 2010 and 2020 and before the GFC. Consequently, the increase in growth asset prices expected in 2021 will result, in our view, more from a clear cyclical improvement in corporate profitability and a resulting increase in the growth premium than a massive reduction in risk perception. This implies a gradual and moderate increase in risky asset returns rather than a sudden spike in performance, as observed recently.

Asset allocation implications

The aggregation of the different signals that we have developed to monitor the different dimensions of risk leads us to adapt our current tactical positioning in two directions. On the one hand, we have reduced the overall size and risk of our tactical bets to contain the overall risk of our portfolios and limit the impact of a correlation shock. On the other hand, we have adjusted our growth theme relative to the inflation theme. The significant increase in breakevens in the US as well as the performance of cyclical commodities in January have validated our reflation bet and led us to take our profits and neutralise this tactical bet. Conversely, we continue to believe that household consumption should surprise to the upside in the coming months and we therefore maintain our positive view on global equities despite negative short-term factors.

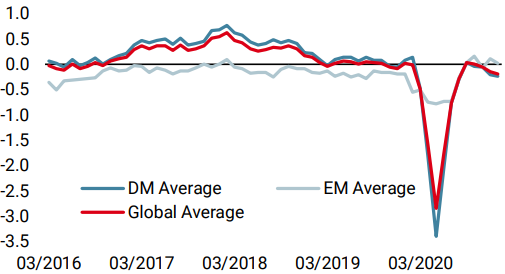

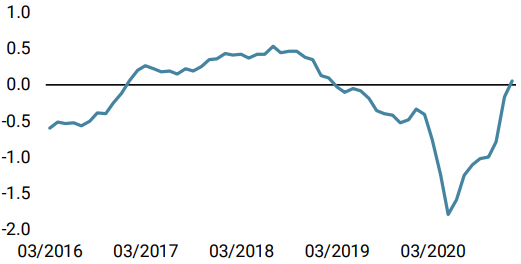

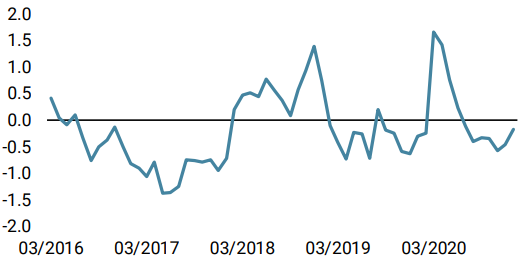

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster remained unchanged globally as weaker US data was offset elsewhere.

- Our World Inflation Nowcaster also remained unchanged, still showing a very high inflation surprise risk.

- Our Market Stress Nowcaster increased last week, mainly as implied volatility took the elevator. For now, market stress risk is high.

Sources: Unigestion. Bloomberg, as of 01 February 2021.

1https://www.nber.org/system/files/chapters/c11075/c11075.pdf

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore (MAS). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).