This week marks the beginning of the Q1 2021 earnings season when we should start to see the first indications of the success (or lack thereof) of the vaccine programmes. Disparate outcomes in vaccination efforts have naturally led to different economic impacts, and market participants have already started incorporating these divergences into expectations for corporate profitability. Indeed, pro-cyclical sectors are expected to post the strongest numbers this quarter and to start closing the gap with those sectors that weathered the coronavirus storm, namely Technology and Healthcare. Recent macro data, especially out of the US, supports the case for a robust cyclical recovery, and if this positive context translates to firms’ bottom lines, we can expect the recent trend of outperformance in cyclical assets, sectors and factors to continue.

Take Care of Business

What’s Next?

Earnings season will likely be an important short-term driver

As they have in the past, US financials will be the first to report this week, including the bulge bracket banks that often serve as a bellwether for the broader market. Next week will see earnings season kick off in Europe, and by the following week, 60% of S&P 500 firms will have reported, along with 50% of firms in the Euro Stoxx 50. With vaccine programmes exhibiting varying degrees of success globally, another jolt of fiscal stimulus in the US, and accommodative monetary policy keeping short-term rates fixed even as long-term rates rise, this earnings season is likely to be a key market driver in the weeks ahead.

Consensus estimates aligned with economic divergences

A critical economic divergence has been building between the US and other economies, especially European ones, over the last couple of months. Thanks to the successful rollout of vaccines and the additional coronavirus relief bill, the US economy is on an upward trajectory toward normalisation. This is in stark contrast to continental Europe that has seen a botched and slow vaccine rollout, and is on a clear downward trajectory toward additional restrictions and lockdowns. Consensus estimates for sales growth is in line with this divergence: while sales for firms in the S&P 500 and Russell 2000 indices are expected to grow respectively by 5% and 9% from a year ago, they are expected to contract for Euro Stoxx 50 and SMI firms (-11% and -20%, respectively). The UK has done an admirable job in turning around its health situation and vaccinating a significant number of people, but the foreign revenue exposures of FTSE 100 firms means that they are expected to see their sales contract by -21% as well.

Looking closer at S&P 500 sectors reveals the cyclical recovery that is expected: Energy, Materials, and Consumer Discretionary firms are expected to see the strongest revenue growth compared to last quarter, though Technology and Healthcare firms are still expected to see the best sales growth on a year-over-year basis. With profit margins expected to recover strongly, firms are expected to turn the top-line numbers into bottom-line growth. Cyclical sectors are again expected to perform best when compared to last quarter: Materials, Industrials, and Consumer Discretionary firms are all expected to see strong EPS growth compared to Q4 2020, from 60% for Materials up to 100% for Industrials. Energy firms are also expected to post stellar earnings growth numbers, though base effects play a significant role for this sector. Importantly, Technology and Consumer Staples are expected to post the weakest quarter-over-quarter growth numbers (29% and 7%, respectively), even if their year-over-year growth figures are expected to fare better.

Confirmed expectations would point to continuation of trends

The market action this year has been largely driven by the outperformance of cyclical/value stocks versus defensive/growth stocks. This dynamic is largely aligned with earnings expectations but there are some points to highlight. While the year-to-date return of the Russell 2000 is nearly double that of the Nasdaq 100 (15.6% vs 9.3%) and the Topix has done the same compared to the SMI (10.1% vs 6.4%), the Euro Stoxx 50 has slightly outpaced the S&P 500 (12.1% vs 12.0%). It is important to point out here the Euro Stoxx 50’s 60%/40% cyclical/defensive split versus the S&P 500’s 40%/60% split has helped the former’s performance this year. European firms’ EPS are also expected to grow slightly faster than S&P firms on a year-over-year basis (28% vs 21%), despite the disparate path in revenue growth. The underwhelming year-to-date return of the Nasdaq 100 may also seem challenged by its expected earnings growth of 35% compared to last quarter, but rising yields have been a heavy burden for the index to bear. A standard Gordon-Shapiro model would suggest that the 70bps rise in the US 10-year yield this year, combined with earnings growth of 35%, would net an expected return of about 4%, all else being equal, given the high duration of these stocks. One important supportive factor for the index is worth noting: speculative long positioning has been reduced significantly over recent weeks, removing some of the technical headwinds facing the index.

Looking ahead, we believe that recent trends should continue: economic growth should continue to improve throughout the year with a subsequent rise in inflation. This will continue to apply pressure on defensive assets, in particular sovereign bonds, while supporting those with a pro-cyclical bias. Indeed, the recent stellar ISM figures from the US suggest the cyclical recovery is accelerating, buoying our preference for equity indices like the Russell 2000 as well as cyclical commodities. The divergence discussed above also pushes us to tilt our positive inflation breakeven view towards US rates.

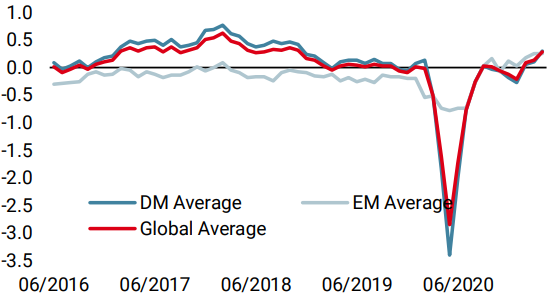

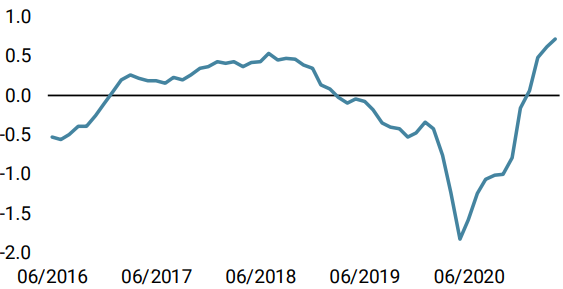

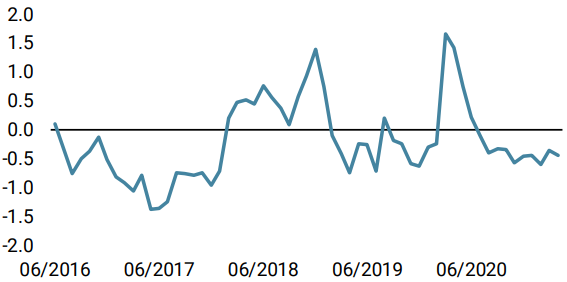

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster increased significantly, mainly on a sharp uptick in the US data. Recession risk is solidly anchored at the “very low” level.

- Our World Inflation Nowcaster increased similar to our growth indicator because of the US data. Inflation risk is very high and we should see a lot of that this quarter.

- Our Market Stress Nowcaster remained unchanged this week. With low spreads and volatility levels, our indicator points to a low market stress risk.

Sources: Unigestion. Bloomberg, as of 9 April 2021

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).