Q3 Earnings Provide Cause for Optimism Despite Failing to Impress Investors

The Q3 earnings season is coming to a close and has thus far proceeded in much the same way as recent quarters: muted expectations from analysts have been surpassed by firms’ results. While equity markets continued to move higher, the performance gap between firms beating versus missing their estimates suggests investors were less impressed by the results. Looking ahead, supply chain challenges and labour shortages are likely to persist for some time, but with firms putting capital to use, primarily via share repurchases, the context for equity markets remains positive in our view.

That Don’t Impress Me Much

What Happened?

Firms continue to post strong results…

The bulk of firms in the US and Europe have now reported their results for Q3, and they have been fairly strong: based on the 73% of firms in the S&P 500 that have reported so far, 83% are beating their Q3 earnings estimates and 67% are beating their sales estimates. For the 62% of Stoxx 600 firms reporting, 59% are beating their earnings consensus estimates and 63% are beating on sales. In year-over-year terms, sales are up 18.5% and earnings 39.4% for reporting firms in the S&P 500, while Stoxx 600 firms are seeing 14.3% sales growth and 44.3% earnings growth.

Figure 1: Percentage of Firms Beating Estimates

Source: Bloomberg, JPM, Unigestion, as of 3 November 2021.

The strong results are also broad-based, at least in the US: the Utilities sector in the S&P 500 has been the laggard in surprises thus far, and 60% of these firms are still beating their earnings estimates. At the other end, over 90% of Technology firms have beat on earnings. In Europe, there is greater variation across sectors, with just 38% of Consumer Discretionary firms beating their earnings estimates while 81% of Financials are beating theirs.

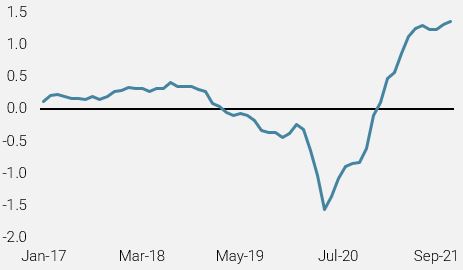

…yet investors are not impressed

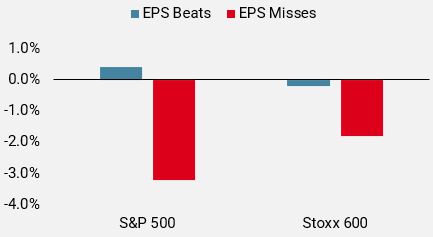

Overall, equity markets have rallied further this earnings season, with the S&P 500 up 6% and the Stoxx 600 up 4% since the first day of reporting to ahead of the Fed meeting and press conference last Wednesday. However, market action suggests investors have not been so impressed by the results and other drivers are pushing equity markets higher. Figure 2 compares the median 1-day price return (relative to the market) of firms that beat their EPS estimates versus those that missed for the S&P 500 and Stoxx 600. As the chart shows, firms who beat estimates were not rewarded nearly to the same degree that firms missing were punished. This asymmetry suggests that investors were likely more optimistic than analysts.

Figure 2: Median 1-day Performance versus MarketX:

Source: JPM, Unigestion, as of 3 November 2021.

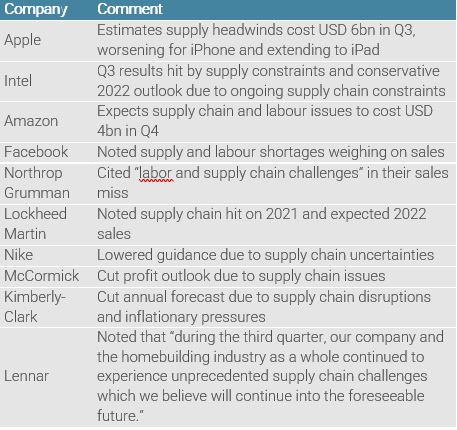

Bottlenecks very much the focus of company commentary

One of the key topics this earnings season was the impact of supply chain disruptions and labour shortages. Few firms escaped these headwinds, and indeed many expect them to continue into the next quarter and, in some cases, next year. Figure 3 highlights a few notable comments from firms during this earnings season.

Figure 3: Company Comments on Labour/Supply

Source: JPM, Unigestion, as of 3 November 2021.

While there are a few different paths through which these bottlenecks may be resolved (declining demand, additional capacity being brought online, delivery delays), they will likely persist into the rest of this year and part of next year as well.

Firms are starting to put capital to work

After becoming flush with cash in the immediate aftermath of the coronavirus crisis, firms have started to put that capital to use. Indeed, among non-financial firms in the S&P 500 that have reported thus far, their cash balances have remained stable quarter-over-quarter and are down -3% year-over-year. One important use of cash has been capital expenditures, which are now in aggregate growing for the S&P 500 and Stoxx 600 and improving for the Energy/Oil & Gas sectors, which have seen some of the largest cuts in capex over the last few years (see Figure 4). A continuation of this trend would provide a key support to growth.

Figure 4: Year-over-year Capex Growth

Source: Bloomberg, Unigestion, as of 3 November 2021.

However, capex is not the only use of cash that is seeing significant growth. Buybacks for S&P 500 firms reporting thus far are up 13% quarter-over-quarter and 68% year-over-year (vs 7% and 20%, respectively, for capex). More than 80% of the share repurchases have been funded with cash, and over USD 730bn worth of buybacks have been announced this year, eclipsing the 2019 level of USD 702bn and approaching the massive USD 939bn seen in 2018.

A positive context for equity risk

Earnings season has largely confirmed our expectations: firm revenue and profitability remain very strong, and though supply/labour bottlenecks are likely to continue to be a drag for the foreseeable future, healthy demand provides sufficient support to equity markets. The Fed meeting last Wednesday also confirmed that the world’s key central bank will remain patient and continue to provide ample liquidity to markets until the middle of next year. Interest rate lift-off is still some time away with “still ground to cover to reach maximum employment.” Thus we believe the context for equity risk going into the rest of the year has improved significantly following this earnings season and a supportive Fed meeting.

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster was steady as better data from China was offset by a deterioration in Australia.

- Our World Inflation Nowcaster moved slightly higher driven largely by higher readings out of Europe and China.

- Our Market Stress Nowcaster moved modestly higher as liquidity indicators became less supportive.

Sources: Unigestion, Bloomberg, as of 5 November 2021.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).