The first half of the year was characterised by record-breaking price action in many asset classes. Many stock indices reached new highs, credit spreads new lows, commodity prices posted their best returns in years and economic momentum gained tremendous traction. Fears of asset bubbles have been mounting, flagged by central bankers as something to watch, but investor appetite for risk has been voracious so far. The exuberance – a state of overexcitement and enthusiasm – in financial markets is real but is it legitimate or is it irrational?

Complacent

What’s Next?

From a macro standpoint, it is rational

There is no question about the current state of the recovery: the world economy is growing well above potential and all, from central bankers to economists and investors, agree. Looking forward, different opinions arise as to whether the peak in activity has been reached or not and if so, whether growth will plateau at elevated levels or start grinding down to long-term potential – or even lower.

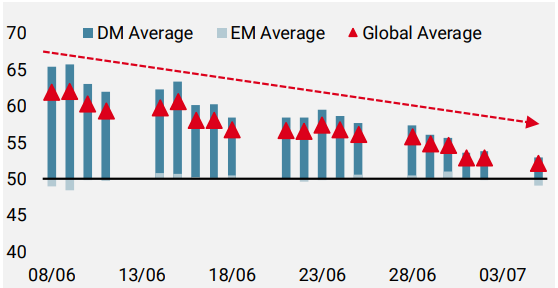

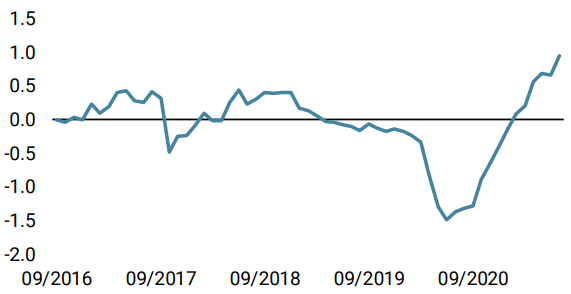

Our Growth Nowcasters have stabilised over the last few weeks, and their diffusion indices (measuring in percentage terms the quantity of improving versus deteriorating macro data) have recently been trending down to 50%, from 60%+ not long ago. This was to be expected as there is a hard limit as to how long data can improve before it starts mean reverting. However, stabilising does not necessarily mean decreasing, and our central scenario is that economic growth will remain above potential for at least 12 to 18 months.

Figure 1: Growth Nowcaster – Diffusion Index over the Last Month

Source: Unigestion, Bloomberg, as of 5 July 2021

There are obvious conditions, risks and dependencies as in any scenario but we remain confident that consumption, investment and employment, the three major GDP components that have failed to rise meaningfully in the recovery so far, will compensate for fading expectations and housing.

Sentiment: frantic but not irrational

Such a supportive macro environment inevitably lifted sentiment and risk appetite. The question is always to assess if asset prices are in line with the current context and account for certain risks, or if there is a disconnect between the two: the roots of complacency and “irrational” exuberance.

Our view is that sentiment has peaked with macro expectations, but is showing signs of complacency toward the risks lying ahead. Looking at equities, the joint forces of strong earnings and ample central bank liquidity legitimates current record levels, where valuations remain relatively contained by very low interest rates. Earnings expectations for 2022 onward have cooled and now align with the expected slowdown in GDP growth. Similarly, credit spreads are now trading close to historical lows, acknowledging the future benign environment for corporate defaults. Inflation-related risk premia such as breakevens and cyclical commodities are another example of rational optimism, which are also in the process of stabilising. However, sovereign yields remain one of the rare market segments that are completely disconnected from macro fundamentals, driven by other forces such as central banks’ asset purchases and relative attractiveness compared to other fixed income assets, as discussed in a previous edition.

Therefore, we can depict the current state of financial markets as being rational but somewhat complacent, given that they are priced for perfection and do not account for the risks ahead.

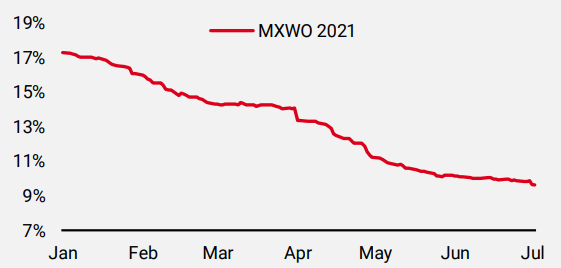

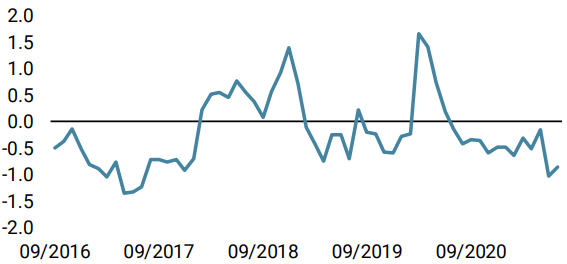

Figure 2: MSCI World Index: Earnings Revision for 2022

Source: Unigestion, Bloomberg, as of 2 July 2021.

Risks are low, but real

Of the multiple events that could derail a superb H1, there are two holding our attention, one “upside risk” and one “downside risk”.

The first regards inflation and central bank actions. There has been a shift recently in the perception of the transitory nature of inflation pressures, acknowledge by a chorus of policy makers, not only in the US but in other countries too. In line with our “stronger for longer” scenario on growth, inflation could surprise for longer and imply a faster-than-expected reduction in accommodation (tapering) and an earlier lift-off in rates. OIS curves currently imply a 50% chance of a rate hike in the US as early as mid-2022, and any further positive developments on the employment front will certainly push this probability higher. For now, investors remain highly sedated by liquidity injections, choosing to ignore that stimulus must end soon, which could end in a rude awakening from a long dream.

The second risk is a repricing of growth expectations that could come on the back of pre-emptive measures taken by governments to anticipate a fourth wave in the pandemic, postponing again the complete reopening of the world economy and choking investor optimism with uncertainty. We remain of the view that this risk remains contained and that rising infection rates will not translate into hospitalisation and deaths at a similar rate to previous waves due to vaccine efficacy and a much higher proportion of vaccinated people.

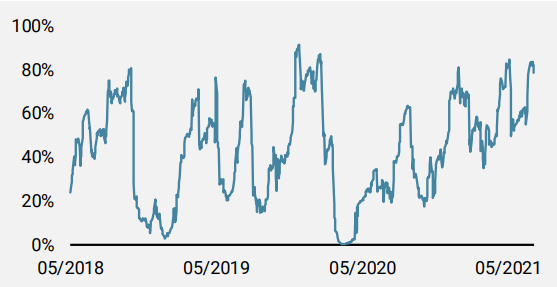

These risks are real, although we allocate a greater probability to the upside risk than to the one of marked macro deceleration. In any case, investor complacency towards these potential sentiment disruptors has reached levels unseen since early May, when markets dropped 5% in a few days, a healthy correction back then.

Figure 3: “Complacency” Indicator: Surged to Last Quintile’s Reversal Zone

Source: Unigestion, Bloomberg, as of 8 July 2021.

We therefore remain overweight to growth and inflation-related assets to reflect our core scenario. Alongside this, we have started adding short-term hedges through long exposure to the US dollar and equity downside protection to cushion against potential bursts of market stress and temporary sentiment reversals.

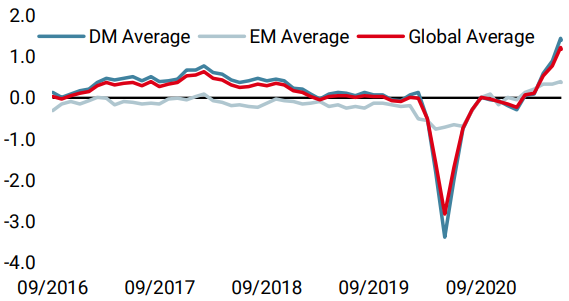

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster retraced, largely due to lower momentum from the US, but remains elevated.

- Our World Inflation Nowcaster also fell modestly due to less inflationary pressures out of the US.

- Our Market Stress Nowcaster moved up further last week due to a continued pick-up in volatility.

Sources: Unigestion. Bloomberg, as of 9 July 2021

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).