This week, for the first time since December 1995, the Federal Reserve will almost certainly ease its monetary policy despite the US economy being far from recession. Consequently, financial markets are divided on the extent and the duration of the upcoming Fed easing. In this weekly note, we analyse previous Fed easing cycles in order to assess the likely impact for financial assets and the global economy. We believe that central banks are ready to do “whatever it takes” to reduce the risk of recession, firstly by lowering short-term rates and secondly, if needed, by restarting quantitative easing. So, sit back and relax, central banks will save markets once again. In 1987, speaking to a Senate Committee, the then Fed president, Alan Greenspan, spoke the famous sentence: “If I seem unduly clear to you, you must have misunderstood what I said”. More than three decades later, the situation has dramatically changed. Central banks around the world have increased their efforts to be transparent by enhancing communication about policy decisions and their assumptions about the economy. Now, with clear forward-looking guidance on policy, dot projections and regular reviews of monetary policy strategy, tools and communication, the stance of central banks is well known and understood by financial markets.“Relax” – Frankie Goes to Hollywood, 1984

What’s Next?

Transparency vs history

Based on recent Fed speeches, it appears almost certain that they will cut rates in 2019. Over the last six months, this transparency on the monetary policy outlook has helped markets to stabilise after the turmoil of last year. As a result, uncertainty is very low ahead of this week’s meeting. We expect a 25 bps cut this week and then a second, similar cut before the end of the year. Currently, the market is forecasting an easing of 100 bps over the next twelve months.

Compared to what has happened in the past, this pricing is either too large if the US economy continues to grow at or slightly below potential, or too small if recession risks increase markedly in the coming months.

In 2000, markets priced in only 50 bps of cuts against actual cuts of 250 bps within six months. Finally, in 2007, as in 2000, Fed easing was large and quick with 225 bps of easing within six months versus the 75 bps expected. Conclusion: financial markets seem blind when they have to evaluate the depth of the economic slowdown and the speed of the downward dynamic. Therefore, they tend to underestimate the size of central bank action.

At this stage of the US cycle, our proprietary US GDP Nowcaster, which tracks the US economy in real time, does not point to any risk of recession in the coming months. However, we are convinced that the Fed has all the tools to act if necessary and will not need to wait for symptoms of recession to activate significant levels of easing. In fact, the Fed has room to lower rates and then to steepen the curve because they are the only central bank to have normalised its monetary policy over the last four years. With its current balance sheet at 2013 levels, the Fed also has room to expand its balance sheet. But why would the Fed ease more than market expectations if recession risk remains low? We believe that the Fed is more concerned about the current inflation dynamic rather than the economic outlook. In their latest monetary policy report submitted to Congress, the Fed highlighted five monetary policy rules (https://www.federalreserve.gov/monetarypolicy/2019-07-mpr-part2.htm). Four of the five rules concern the difference between the sustainable long-term rate of unemployment and the current unemployment rate, and the difference between recent inflation and the FOMC’s longer-run objective. The fifth one, the price-level rule, takes into consideration the deviation of inflation from the long-run objective in earlier periods as well as the current period. The other rules do not consider the past misses of the inflation objective. This price-level targeting rule was favoured by former Fed chairman Ben Bernanke to face effective lower bound (ELB) challenges in 2017. In the latest report, this rule is the only one below the current Fed Fund rate. Moreover, the recommended rates of the price level rule are closer to 0 than to 225 bps below current rates, roughly the size of the six month easing cycle in 2000 and 2007. Anticipating large moves from central banks means forecasting a high risk of recession. Historically, such a context has not been favourable for growth-oriented assets and they have underperformed government bonds. Since 1989, in the six months following the first Fed cut, US equities have delivered an average return of 5%. However, the dispersion has been large, with a 28% return in 1998 and a 13% loss in 2007.Risk scenario is “Dovishness” not “Hawkishness”

“Bad is good” or “bad becomes bad”

Relax

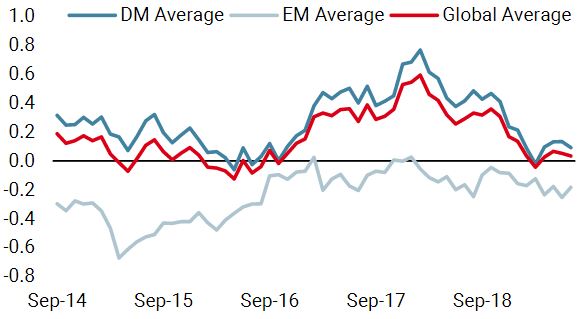

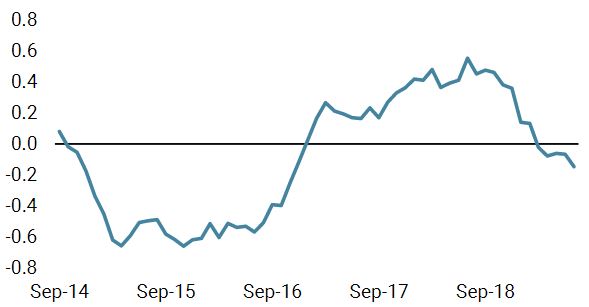

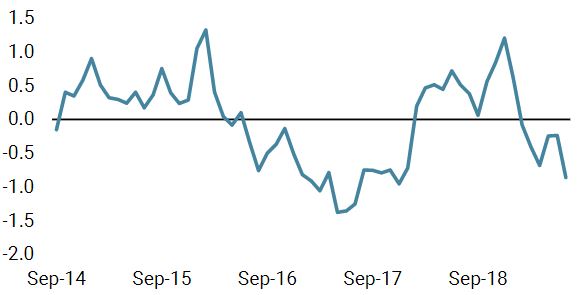

Our medium-term views remain cautious, and we prefer to get exposure to growth via high yield corporate credit. We are also complementing our equity exposure with options to protect the portfolio in the case of equity drawdowns. Over the month of July thus far, the Uni-Global – Cross Asset Navigator fund is up 1.30% versus 1.55% for the MSCI AC World Index and 0.53% for the Barclays Global Aggregate (USD hedged). Year-to-date, the Uni-Global – Cross Asset Navigator has returned 8.52% versus 18.03% for the MSCI AC World index, while the Barclays Global Aggregate (USD hedged) index is up 6.57%. World Growth Nowcaster World Inflation NowcasterStrategy Behaviour

Performance Review

Unigestion Nowcasting

Market Stress Nowcaster

Weekly Change

- Our world Growth Nowcaster remained unchanged this week, as the slight improvement in the US situation was offset by European and Japanese data.

- Our world Inflation Nowcaster decreased further this week, mainly driven by continued disinflationary prospects in the US.

- Market stress decreased this week, as credit spreads contracted.

Sources: Unigestion. Bloomberg, as of 29 July 2019.

Past performance is no guide to the future, the value of investments can fall as well as rise, there is no guarantee that your initial investment will be returned. Important Information Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed by recipients to any other person. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in the investment vehicles to which it refers. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Please contact your professional adviser/consultant before making an investment decision. Where possible we aim to disclose the material risks pertinent to this document, and as such these should be noted on the individual document pages. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of this information. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor. Uni-Global – Cross Asset Navigator is a compartment of the Luxembourg Uni-Global SICAV Part I, UCITS IV compliant. This compartment is currently authorised for distribution in Austria, Belgium, Denmark, Finland, France, Germany, Ireland, Italy, Luxembourg, Netherlands, Norway, Spain, UK, Sweden, and Switzerland. In Italy, this compartment can be offered only to qualified investors within the meaning of art.100 D. Leg. 58/1998. Its shares may not be offered or distributed in any country where such offer or distribution would be prohibited by law. No prospectus has been filed with a Canadian securities regulatory authority to qualify the distribution of units of these funds and no such authority has expressed an opinion about these securities. Accordingly, their units may not be offered or distributed in Canada except to permitted clients who benefit from an exemption from the requirement to deliver a prospectus under securities legislation and where such offer or distribution would be prohibited by law. All investors must obtain and carefully read the applicable offering memorandum which contains additional information needed to evaluate the potential investment and provides important disclosures regarding risks, fees and expenses. All investors must obtain and carefully read the prospectus which contains additional information needed to evaluate the potential investment and provides important disclosures regarding risks, fees and expenses. Unless otherwise stated performance is shown net of fees in USD and does not include the commission and fees charged at the time of subscribing for or redeeming shares. Unigestion UK, which is authorised and regulated by the UK Financial Conduct Authority, has issued this document. Unigestion SA authorised and regulated by the Swiss FINMA. Unigestion Asset Management (France) S.A. authorised and regulated by the French Autorité des Marchés Financiers. Unigestion Asia Pte Limited authorised and regulated by the Monetary Authority of Singapore. Performance source: Unigestion, Bloomberg, Morningstar. Performance is shown on an annualised basis unless otherwise stated and is based on Uni Global – Cross Asset Navigator RA-USD net of fees with data from 15 December 2014 to 10 June 2019.Navigator Fund Performance

Performance, net of fees

2018

2017

2016

2015

Navigator (inception 15 December 2014)

-3.6%

10.6%

4.4%

-2.2%