The knock-on effects of the rise in bonds yields pose significant risks and opportunities to investors. Importantly, they provide further support for the rotation in equity markets that came to the fore as vaccination programmes commenced. The prospect of economic normalisation bodes well for the bottom lines of firms that have struggled over the last year. Beyond this macro support, the cheaper valuations and least-favoured status of these equities provide fertile soil for a strong comeback. In this context, swiftly rising bond yields could transform an orderly rotation, where equity markets continue to rise while a rotation occurs under the surface, into a disorderly one, where the rotation rises to a tumult and the broader market is challenged.

Circles

What’s Next?

Investors continue adjusting their expectations

Financial markets have largely continued their recent trends this month, with bond yields continuing their climb and equity markets broadly flat but with high dispersion across geographies, sectors, and factors. Inflation expectations have moved up further, though at a slower pace than at the end of February. With President Biden approving the US 1.9tn stimulus last Thursday, fiscal impulse from the US will remain positive for some time. While the bill does not include a minimum wage increase, which would have had a more persistent impact on US inflation, it does include USD 1,400 cheques for low- and middle-income Americans, providing another short-term boost. Real rates in the US have remained stable since their surge in February, but remain negative along with those in Germany and the UK. While the latter economies have struggled over the last few years to lift economic growth, prolonged periods of negative real rates in the US are rare. Absent inflation expectations skyrocketing, real rates should continue their upward trajectory with stimulus-supported economic growth.

Opportunities in equity markets

As we have communicated in recent weeks, we believe alpha is critical in the current context since beta will be challenged by rising yields and correlation shifts. One area where we believe there are good opportunities to express our core view – a strong cyclical recovery producing upward inflation pressures – is select equity indices. A few observations to note:

- Unsurprisingly, investors flocked to secular growth stocks after the COVID shock, as these firms offered a combination of resilient earnings, strong balance sheets, and cash flows that benefited significantly from lower rates.

- For country indices, this post-COVID rotation favoured those with large exposures to defensive sectors, such as Consumer Staples, Communication Services, Health Care, and IT, at the expense of those with a cyclical bias, i.e., large tilts to sectors such Industrials, Financials, Energy, and Materials.

- This exacerbated longer-term trends that favoured growth over value, with the MSCI World Value index’s underperformance vs the MSCI World Growth index surpassing the lows of the Tech Bubble by the end of 2020.

Planting the seeds of the reversal

As often happens, the reasoning that led investors to back the winners of 2020 laid the foundations for an eventual reversal. As vaccination programmes have rolled out (with varying degrees of success), the prospect of economies reopening safely has become a headwind for past winners that benefited from the work-from-home economy. At the same time, these stocks are more interest rate-sensitive, as their far-dated cash flows are hit especially hard by higher discount rates.

On the other hand, the losers of 2020 now stand to benefit from the broader context: energy firms from higher oil and gas prices, financial companies from steepening yield curves, and industrials from a recovery in household and corporate demand. They are under-owned, relatively cheap, and many have only recently recovered their COVID losses. A handful of country indices stand out: the Russell 2000, Toronto Stock Exchange (TSX) Composite, Euro Stoxx 50, FTSE 100, Topix, and the ASX 200 each have 60-75% exposure to cyclical sectors.

Examining the historical performance of these indices during periods of rising growth premia (i.e., real rates) is helpful in today’s context. From 2000 until the end of 2020, a basket of these “cyclical/value” indices have outperformed a basket of “secular/growth” indices (S&P 500, Nasdaq, SMI, and MSCI EM) by 5.4% during periods of rising US real rates on average. During two of these periods (March-October 2008 and July-December 2016), the cyclical basket outperformed the secular one by more than 8%. Moreover, while the cyclical basket has outperformed the secular basket by 4% year-to-date, it has still underperformed by 10% since the beginning of the COVID shock.

Valuations also provide positive factors for the cyclical indices. While equities are expensive across the board on an historical basis, the valuations of cyclical indices are not quite so extreme as the secular indices. For example, using a cross-sectional average of value measures, including enterprise value and price ratios, we find that the valuations of the TSX Composite and FTSE 100 are “only” around their 65th percentile, while Topix is at its 68th percentile. Contrast this with SMI, which has the most attractive valuation among the secular/growth indices, at its 73rd percentile.

We continue to believe that rising yields are a key determinant of a sustainable rotation across assets, factors and sectors, and that faster rises will lead to a more disorderly rotation with bouts of market stress. Our investment framework points us toward cyclical exposures, whether in energy commodities, in currencies where we favour the Norwegian krone and Canadian dollar, or in equity indices with our preference for cyclical indices over secular ones.

Unigestion Nowcasting

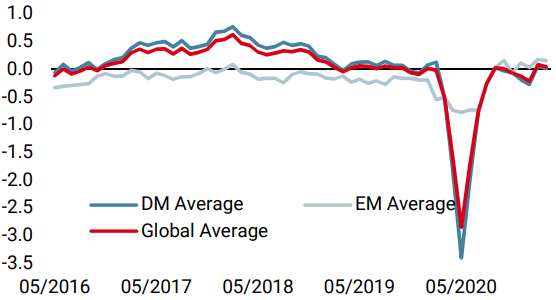

World Growth Nowcaster

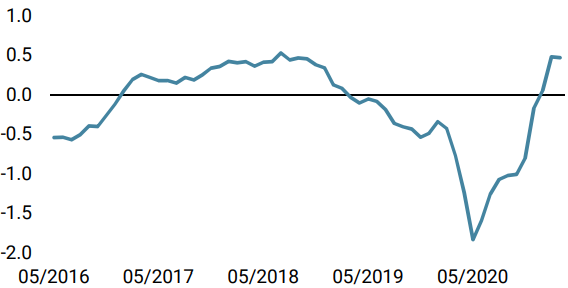

World Inflation Nowcaster

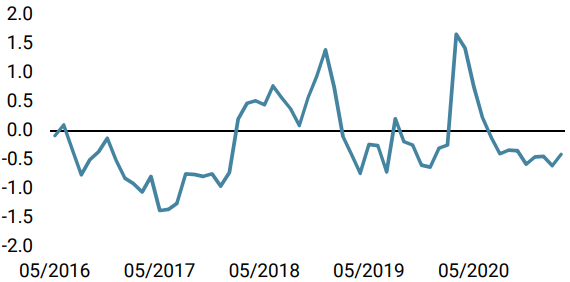

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster declined slightly as US data showed a limited decline. Recession risk remains low with 53% of data improving across our indicators.

- Our World Inflation Nowcaster was steady last week, the first time in a while. Inflation risk remains yet very high.

- Our Market Stress Nowcaster decreased as volatilities declined and spreads contracted. Market stress risk is neutral for now.

Sources: Unigestion. Bloomberg, as of 12 March 2021

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).