After a very strong start to the year for risk-taking broadly, with most assets posting very solid returns, it seems like sentiment is becoming more fragile. A lot of positive information on both macro and microeconomic fronts has already been discounted in asset prices and investors are now waiting for the piece of news that could lift expectations even higher, or conversely call for more cautiousness. As the famous trading expression says, “Sell in May and go away”. Will this apply in 2021?

Bumpy Road Ahead

What’s Next?

Improving growth but watch out for inflation

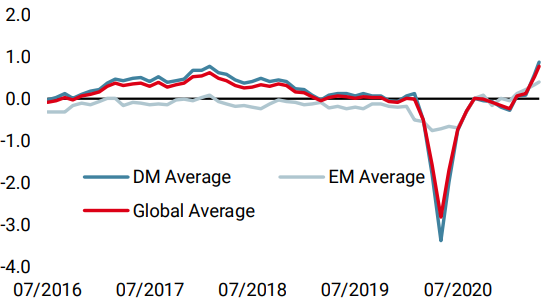

From a macro standpoint, there is at this point nothing to worry about. Growth projections for 2021 have recently been revised higher in most major economies, buoyed by the acceleration in the vaccination campaigns and the resulting higher demand expectations for the second part of the year. In the US and Europe, policymakers are confident that economic activity will rise above their most recent GDP expectations for the year – respectively, 6.5% and 4% – while they expect inflation to remain under control in spite of what they call a “temporary” overshoot above target levels. In terms of actual data measured by our proprietary Nowcaster indicators, we continue to observe an acceleration in growth momentum. Global economic activity levels are way above potential and are now back to their late 2017/early 2018 peak, while diffusion indices (the percentage of improving macro data) have been solidly anchored above 60% for three months in a row. Interestingly, this acceleration is now a common factor amongst all the developed and emerging countries that we monitor, with the anecdotal exceptions of Thailand and Indonesia.

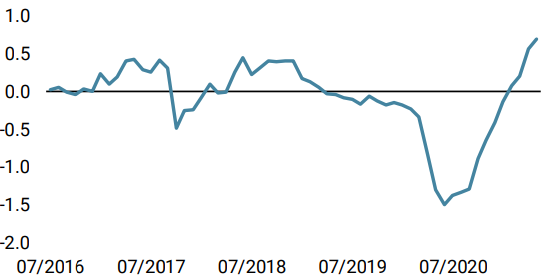

Inflation remains the main risk, in our view. Indeed, both our Inflation Nowcaster and Newscaster have reached multi-year highs but inflation has not yet taken a toll on investor sentiment for risky assets. This has much to do with central bankers’ rhetoric about the temporary – or “transient” – nature of current price pressures, but we believe that once realised inflation accelerates toward and above their 2% target, it could create volatility and stress in financial markets. Complacency towards inflation is a dangerous game. The last time it happened was in early 2018 when it triggered a short-lived yet violent correlation shock in February and March of that year. There are similarities between the situation now and then that should not be overlooked, and inflation could well be the spark in the powder keg.

Sentiment needs to cool off

This very strong macro backdrop has increased investor risk appetite, pushing growth-related assets close to or above historical highs. Although it makes sense to see sentiment surging on the back of clearing macro skies and the rapidly improving health situation, the question now is: to what extent has this positive newsflow already been factored into asset prices and is this optimism becoming excessive. By combining different market metrics into a sentiment indicator, we can see that the answer from an historical perspective is definitely a ‘yes’. By the end of the first week of May, upside velocity, realised, implied and intraday volatility levels, the number and scale of negative versus positive trading days, and the length of the rally with no major negative daily returns were all in the top quintile or decile over the last three years. Such a combination of market technicals is usually followed by a sub-trend or by negative returns. The average 30-day drawdown following such strong risk appetite readings is -5%. This is another metric comparable to the market context observed in early 2018. It is also comparable to Q3 2018 (just before the major Q4 selloff), late 2019 (before the Covid-19 crisis) and, more recently, late 2020 (which yielded volatility without return).

Central banks are at a turning point, the tide in monetary support is turning

Monetary and fiscal support have helped economies to weather the unprecedented macro shock induced by the Covid-19 pandemic, no doubt about it. Central banks’ actions also helped stabilise financial markets through massive liquidity injections, which are set to end in the next 18 months. However, now that most of the job is done in terms of growth, and unemployment and inflation are both on positive trajectories, the tide of economic support will inevitably turn. Tapering is coming, and earlier than expected. The BoE recently announced a decrease in its monthly asset purchases and the ECB will probably follow suit in the second half of the year, reducing the pace of its special PEPP umbrella. The BoJ has increased the threshold to buy equity ETFs and the Norges bank might be the first developed central bank to hike rates, before year-end. Even if the rate of the tapering is not set in stone and will be dependent on the future course of economic activity, itself dependent on the pandemic evolution, the direction is clear, there will be less support going forward, for good reasons.

That being said, tapering does not mean tightening, and we are very far from a global liftoff in rates, so monetary conditions will remain accommodative for the foreseeable future. In the US, the Fed seems committed to remaining behind the curve, adopting a reactive rather than proactive stance. Fed rhetoric around inflation has been a blessing in preventing sovereign yields from rising further and reassuring investors than the lessons from the taper tantrum have been learnt. However, it could turn into a curse if the Fed’s credibility is challenged by the data, forcing them to act quicker than initially planned. One asset class is defying the view from the Fed: inflation breakevens. At the beginning of the year, both the short end (2-year) and the longer end (10-year) of the inflation breakeven curve traded around 2%, pricing in expectations that the US inflation gauge would stabilise around the Fed target. Since then, the 2-year has jumped to 2.8% and the 10-year has soared to 2.55%. This means either that market expectations are excessively high, or that higher prices are here to stay for some time. In our opinion, short-term expectations are fairly priced and inflation will surprise to the upside, while longer anticipations are too high and will converge over time toward the Fed’s 2% average target.

Therefore, we believe that there is a need to distinguish between short-term and the medium-term market environments. Over the short run, overoptimistic sentiment and high valuations in growth and inflation-related assets could increase the odds of market stress events, with inflation surprises acting as a potential catalyst during a period of historically unfavourable seasonality. Over the medium term however, we expect to see continued improvement in macro conditions as the world reopens and economic activity resumes. Pent up demand from consumers and the implementation of fiscal plans are yet to hit the real economy and will provide a durable extra boost to corporate profits. The road may get bumpier ahead but the trajectory remains upward.

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

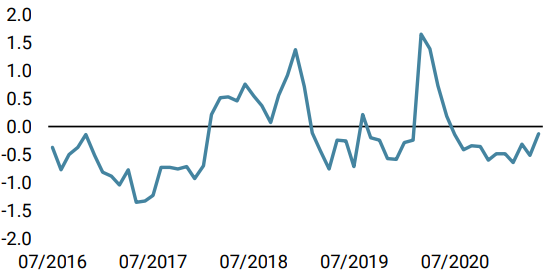

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster increased further with a broad improvement across countries, with India notably showing the most improvement.

- Our World Inflation Nowcaster ticked up slightly, due in large part to higher wage data from Switzerland and expected inflation in the US.

- Our Market Stress Nowcaster increased thanks to high volatility in markets.

Sources: Unigestion. Bloomberg, as of 17 May 2021

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).