The last few weeks have seen a significant shift in the pace of growth across many of the world’s economies. While this slowdown is taking place from extremely high levels, it is nevertheless concerning due to its breadth and underlying drivers. The Delta variant is clearly having an impact on demand and delaying economic reopening even if it does not necessarily lead to lockdowns like we saw last year. Early signs that the variant may be peaking, with the number of new cases and hospitalisations turning over, is encouraging but it will need confirmation. In the meantime, we have shifted to a more selective exposure, favouring those assets and markets that we expect to perform well during a period of more moderate economic expansion.

Slow Burn

What’s Next?

The slowdown can be seen across economies and drivers

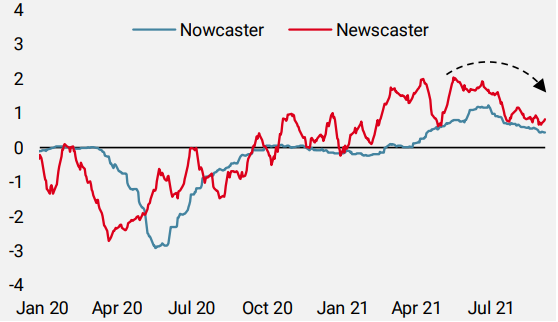

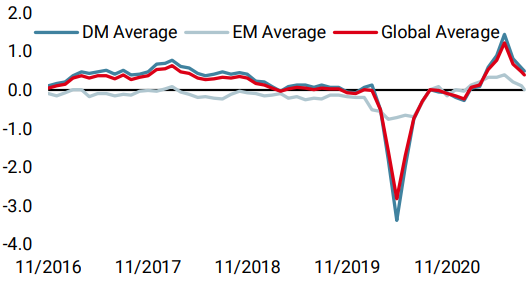

Since the end of June, our proprietary indicators tracking global growth have been declining steadily. Both our Global Growth Nowcaster – which aggregates and analyses traditional macro fundamental data – and our Global Growth Newscaster – which aggregates and analyses news sentiment data – suggest that the growth impulse has peaked, even if growth remains above its potential level. Figure 1 shows the evolution of these indicators since the beginning of last year, both of which have declined after seeing their respective diffusion indices (which indicate the percentage of improving versus deteriorating data) fall below 50%.

Figure 1: Global Growth Indicators

Source: Bloomberg, RavenPack, Unigestion, as of 08.09.2021

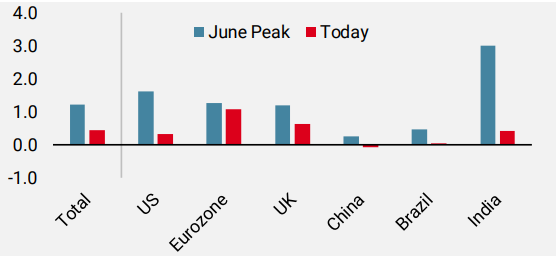

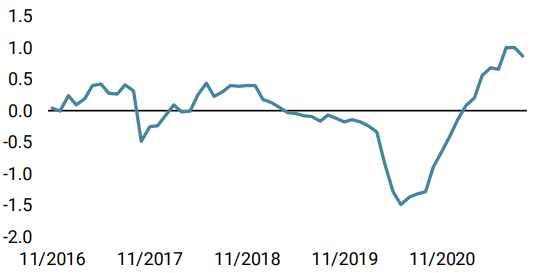

This phenomenon of economic expansion at a slower pace can be seen at the individual country level. As Figure 2 demonstrates, it is fairly broad-based with nearly all countries down significantly from their early summer levels. The Eurozone is the exception, where growth remains at a similar elevated level as it was at the end of June. However, the Eurozone diffusion index has fallen from 67% of data improving at the end of June to just 40% of data today, suggesting that growth here is also slowing.

Figure 2: Growth Nowcaster by Region

Source: Bloomberg, Unigestion, as of 08.09.2021

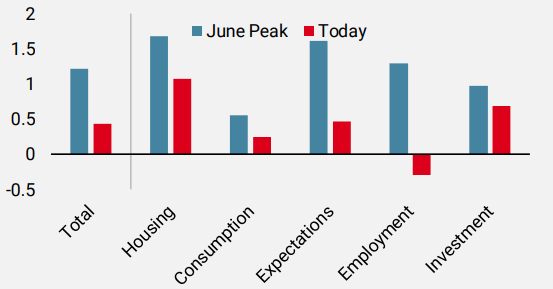

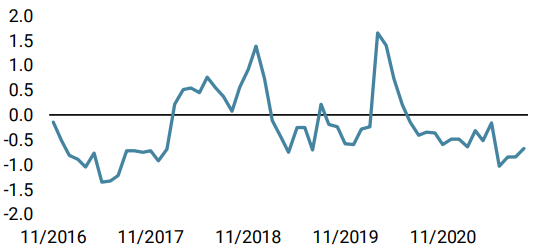

Looking at the components of our Global Growth Nowcaster, much of the slowdown is due to Employment, with job growth at a standstill, and Production Expectations highlighting that businesses are seeing deteriorating demand (see Figure 3). Importantly, Consumption never reached the highs of some of the other components and is now close to its long-term level, whereas we had expected it to catch up and put the recovery on a more sustainable footing.

Figure 3: Global Growth Nowcaster by Component

Bloomberg, Unigestion, as of 08.09.2021

The Delta variant has dragged but vaccines remain effective

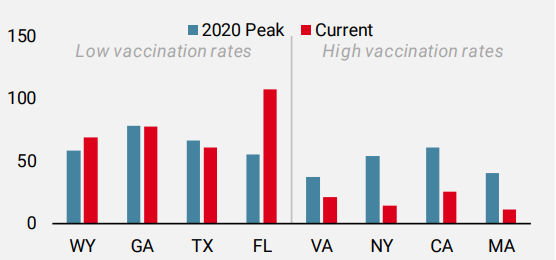

Surging coronavirus cases due to the Delta variant have significantly hampered the economic recovery, either directly by reinstituting restrictions in some cases like New Zealand, or indirectly by denting household and corporate sentiment in the face of added uncertainty. While the most recent data is subject to revisions, the US does seem to be turning a corner with the number of new daily cases (smoothed over a seven-day window) falling over the last couple of days. Most European countries (outside of Germany and the UK) have also seen the rate of new cases decline over the last couple of weeks, as have Japan and China. New hospital admissions – which are the trigger for restrictions – seem to have stabilised or fallen in many countries, including the US. While there has been a focus on the degrading efficacy of the vaccines against infection by the Delta variant, their efficacy against severe cases requiring hospitalisation appears to be stable even months after inoculation. The US, with its disparate state responses to Covid, provides a useful case study. As Figure 4 demonstrates, states with low vaccination rates have seen their hospitalisations rise back to the peaks they saw in 2020, while those with high vaccination rates are seeing much lower rates of hospitalisations. Florida is a notable case in point, where a ban on mask mandates and a large at-risk population have likely fuelled the surge in hospitalisations.

Figure 4: New Hospital Admissions by US State (7d MA, per 100k)

Source: CDC, Mayo Clinic, Unigestion, as of 31.08.2021

Shifting from pro-cyclical to more secular growth exposures

The change in economic conditions has led our exposures to follow suit, moving us away from the strong pro-cyclical bias we had earlier to a more cautious stance that is selective in its growth exposure. Importantly, we do remain positive on the macro context as we expect monetary policy to remain supportive in the face of the growth slowdown. Thus, our underweight in government bonds has been significantly reduced, and we are pairing an overweight in developed equities with underweights in corporate credit spreads. We are also maintaining a long US dollar bias, mainly against developed world currencies, to hedge our two main risks of an upside inflation shock or a significant further decline in growth.

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster declined slightly due to a broad loss in momentum across most economies.

- Our World Inflation Nowcaster declined slightly but remained at elevated levels with most countries seeing stable inflation pressures.

- Our Market Stress Nowcaster increased modestly because of higher market volatilities.

Sources: Unigestion, Bloomberg, as of 10 September 2021.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).