Small and Mid-market Private Equity: The Calm During the Storm

-

COVID-19 is set to send the global economy into a recession deeper than that seen during the GFC.

-

During a crisis or recession, small and mid-market companies have historically been more resilient than their larger counterparts.

-

History shows that it is at the small end of the market, rather than among the biggest companies, that private equity deals with the highest return potential are to be found and we expect this to continue to be the case.

Overview

The COVID-19 pandemic will likely cause one of the largest economic crises of the past 100 years. Although its full impact is uncertain and will not be quantifiable for some time, it has already been a massive and rude awakening for investors lulled to sleep by accommodative central banks over the last decade. However, one thing we can say for certain is that the global economy is heading for a recession, with many individual economies expected to experience contractions of a magnitude never seen before.

The last global recession was triggered by the Global Financial Crisis (GFC) of 2007/08. In this paper, we assess if there are any similarities between the GFC and the current crisis and what the impact will be on private equity backed small and mid-market companies. Furthermore, we consider what the investment opportunities will be coming out of this crisis.

Are there any parallels to be drawn between the GFC and the current crisis?

The catalyst for the GFC was a negative shock in the US housing market that rapidly spread to the rest of the world through linkages in the global financial system. While the triggers are very different this time around, the strong global economic growth, robust financial markets and over-inflated valuations heading into this crisis represented very similar conditions to those prior to the GFC. Therefore, with certain caveats, observations from the last crisis can still be relevant when adjusted to the new environment.

How did small and mid-market companies fare in the last crisis?

During the GFC, there were certain small and mid-market companies that did not perform particularly well, especially those operating in cyclical sectors such as oil & gas, travel / leisure, automotive and consumer discretionary – all areas one would expect to struggle during recessions.

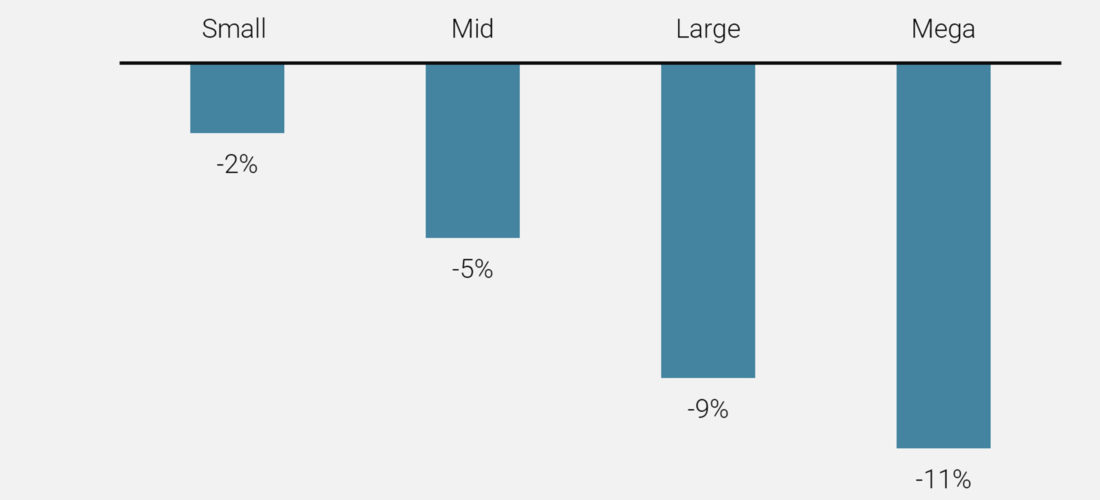

Nevertheless, most portfolio companies of small and mid-market private equity funds showed better resilience than those of large and mega-cap funds, as shown in Figure 1. Indeed, such companies tend to have lower leverage and often operate in niche sectors or in those that are less sensitive to economic ups and downs. Furthermore, they are usually more nimble. In times of trouble it is easier for them to react quickly – for example to immediately cut costs or reduce capex. Given their lower leverage and generally stronger balance sheets, it is also easier for them to absorb a temporary reduction in EBITDA and an increase in debtors and/or inventory.

Small and mid-market companies that prevailed operated in niche sectors, had strong management teams and low leverage

Figure 1: Returns of buyout funds in recession regimes

Can you give some examples of such companies that were in the portfolio during the last crisis?

One name that many readers will recognise is Jimmy Choo, the luxury accessories brand centred around ladies’ designer shoes. We invested in the company in 2007, on the eve of the GFC, and ultimately delivered a 2.7x return on our investment. The company had an exceptional management team, high EBITDA margins, a loyal customer base and huge scope for expansion in affluent emerging markets, such as Dubai, Hong Kong and Macau. Being nimble was also critical: when the GFC hit, the company immediately slowed down its store roll-out programme in order to strengthen its cashflow and became more selective on new store openings – targeting only those with very high ROIs.

Even when things are not going well, small and mid-market companies can be repositioned, with Premo being one such example. We invested in Premo, a Spanish supplier of innovative magnetics and RFID solutions to the automotive industry, in 2007. The company suffered considerably from the demand shock of the GFC and breached its debt covenants. However, we quickly intervened and helped the management team to restructure the company’s balance sheet and refocus its strategy on the most promising and profitable products – RFID solutions for keyless entry and magnetics for hybrid and electric cars. Ultimately, we were able to recoup 1.3x our original investment.

How will it be different for small and mid-market companies in the current crisis?

Early indications are that the COVID-19 crisis will cause a much deeper global recession than in 2007-09. Already, the unemployment numbers are worse than they have been in generations. In order to help businesses navigate this crisis, governments are intervening with stimulus packages on a scale never seen before. In light of this unprecedented combination of factors, it is uncertain which form the eventual recovery will take – V-shaped, W-shaped or even L-shaped.

A unique aspect of the current crisis is that many businesses will have zero revenues for several months while still maintaining a significant cost base

A unique aspect of the current crisis is that, with around four billion of the global population in some degree of lockdown, many businesses will have zero revenues for several months while still maintaining a significant cost base. Therefore, some sectors (such as leisure or restaurants) are under severe pressure. Other sectors (such as video conferencing or e-commerce) are actually benefiting from the lockdowns. Finally, certain sectors (such as energy or transportation) will likely benefit from government support. This shows that, for investors, being diversified and investing in themes that are driven by megatrends is critical.

It is also worth noting that today there is much more dispersed and unregulated private debt in the system than there was during the GFC. While banks are, on average, substantially better capitalised and thus more able to assist troubled companies, it is still too early to tell what their medium to long term reactions (and those of debt funds) will be.

Nevertheless, while it is too soon to make predictions on which companies will survive, we believe that the resilience and agility of small and mid-market companies will remain an important differentiator as we navigate the current crisis.

How should we expect small and mid-market funds that will invest in the years following the crisis to perform?

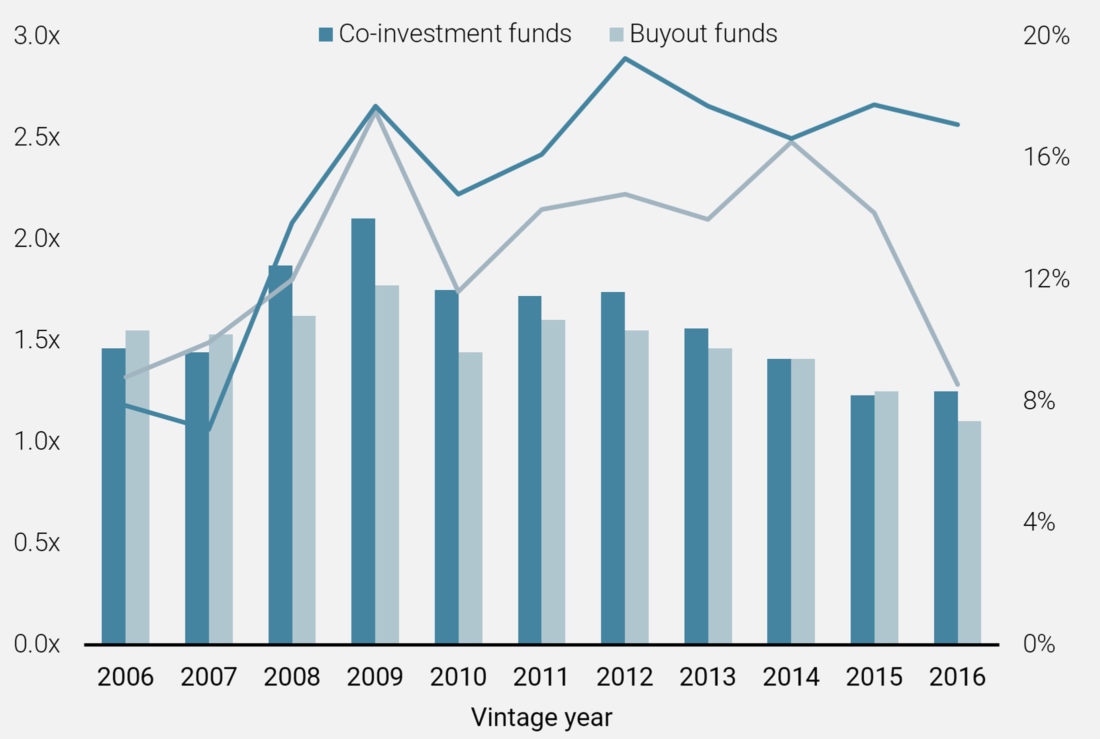

Figure 2 highlights that the best vintages for small and mid-market funds over the last 15 years were 2008 and 2009, just as we were in the midst of the last crisis. Thanks to lower fees and carried interest, co-investment funds did even better than buyout funds.

The best vintages over the last 15 years were from 2008/09, just as we were coming out of the GFC

This strong performance was driven by a number of reasons. Firstly, private equity investors were able to benefit from lower entry valuations in the years immediately following the GFC. Secondly, the small and mid-market companies in which private equity firms invested were those which had already survived the GFC, clearly demonstrating the resilience of their business models. Finally, the eventual economic recovery from 2009 onwards provided a useful tailwind to all companies.

We believe that the next one to two years will provide similar conditions for investors in small and mid-market companies.

Figure 2: Performance of co-investment vs. buyout funds below USD 1.5bn

Which sectors or investment themes do you expect to be of most interest in the coming months?

For some time, we have been pursuing a number of investment themes as part of our direct investment strategy. Our investment themes are driven by overarching megatrends such as evolving demographics and technological progress, and thus are long term and robust in their nature. The COVID-19 crisis and its implications have brought several of these themes into sharper focus in recent weeks. Lockdown, quarantine, self-isolation and working or studying from home have become the new norm for billions of people around the globe. A number of our investment themes, such as “Future of Work”, “Healthcare System Reengineered” and “Localisation of Supply”, are being positively impacted by this current situation.

The COVID-19 crisis has brought several of our longer term investment themes in to sharp focus in recent weeks

Future of Work: It has taken surprisingly little time for the majority of people to adapt to working from home and for schools, colleges and universities to offer various forms of e-learning and virtual teaching. With the rapid success of these new ways of working and learning, we can expect this trend to continue even after the current crisis is over. Consequently, technology, education and media companies which operate in these areas will benefit from this tailwind. For example, at the beginning of April, we invested in a US education company delivering culinary arts courses by e-learning.

Healthcare System Reengineered: COVID-19 has uncovered important gaps in our current health care systems when it comes to protecting the population from viral and bacterial diseases. As a result, both private and public spending within this area will only increase in a post-COVID-19 world. Areas of health care that should benefit include diagnostics, vaccines, medical equipment, home-based medical devices and online consultations. For example, we are invested in an Italian diagnostics business that has launched promising COVID-19 testing equipment.

Localisation of Supply: Supply interruption and concerns about supply quality is nothing new and it was in evidence during the GFC. But during the current crisis and global shutdown of economies and borders, it has now reached a whole new level, affecting the supply of vital ingredients such as APIs for drugs and food, and strategic components for many industries such as telecom, automotive and textiles. As we return to some sense of normality in the months ahead, we are likely to see several responses to limit such problems from occurring again. This will lead to the gradual reorganisation of global supply chains, the need for flexible business models and an increase in demand for local products. For example, in January this year, we closed an investment in a Northern European vitamin producer that supplies the rapidly growing vitamin K2 market in Europe.

Where do you expect to source investment opportunities in the short term?

We expect to see a number of opportunities emerge among small and mid-market companies in the months ahead

As a result of the COVID-19 crisis, we expect to see the following opportunities in the small and mid-market:

- Companies with immediate cash needs (e.g. recapitalisation where debt is not available)

- Spinouts from distressed conglomerates

- Growth companies requiring cash to benefit from transformational growth opportunities. As an example, we are currently considering an investment in a fast growing, US-headquartered billing software company that needs liquidity to continue to fund its growth but which the GP cannot provide

- Companies that are consolidating fragmented markets and need financing to acquire distressed players (since banks will be less willing to lend for expansion purposes)

- Portfolio companies of GPs who need to generate liquidity for their LPs.

- Companies sourced by GPs who have no capacity for further deals in their current fund and are unable to fundraise for their new fund

What sort of characteristics will you be looking for in companies?

We follow investment themes driven by long-term trends and invest in resilient small and mid-market companies, allowing us to build robust portfolios, which can largely withstand economic shocks

Irrespective of the current crisis, we are not rewriting our investment rule book when it comes to small and mid-market companies. We still seek to invest in companies that operate in sectors driven by investment themes. At the same time, we continue to seek companies that possess the following characteristics:

- Strong management teams

- Leading positions in (niche) markets

- Highly visible / recurring revenue streams (e.g. subscription based business models, provision of critical products or services)

- Diversified client base, preferably in resilient end markets

- Cash generative with low capex

- Multiple opportunities to generate value

- Low leverage

- Desired asset by multiple buyer groups

What was the last direct investment you made?

In February 2020, we invested in HealthTech BioActives (HTBA), a carve-out from a large pharmaceutical group. HTBA is a Spanish manufacturer of raw materials for the pharmaceutical, cosmetics, food & beverages and animal feed industries. Its products are mainly flavonoids derived from citrus fruits and other plants, as well as B12 vitamin derivatives and other substances.

Even after the current crisis, small and mid-market companies will continue to be a hothouse for tomorrow’s leaders

This investment plays to our theme of “Healthcare System Re-engineered” which is being driven by an ageing population and rising health awareness. In addition, HTBA has a world class management team, a broad base of loyal international customers and patented products and processes. As a testament to the resilience of this company, revenues in Q1 2020 are well ahead of plan, with demand for the company’s products actually increasing as a result of the crisis.

Small and mid-market companies have always represented a key part of the overall economy and, even after the current crisis, they will continue to be a hothouse for tomorrow’s leaders. History shows that such companies, particularly when in private equity hands, demonstrate superior resilience compared to larger companies during a crisis. Indeed, the current crisis is highlighting how important it is for investors to follow enduring investment themes and target robust companies.

It is at the small end of the market, rather than among the largest companies, that private equity deals with the highest return potential can be found. Consequently, we believe that some of the most exciting investment opportunities in the aftermath of this crisis will come from the small and mid-market.

Important Information

Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed (in whole or in part) by recipients to any other person without the prior written consent of Unigestion. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in either the investment vehicles to which it refers or to any securities or financial instruments described herein. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Such documentation contains additional information material to any decision to invest. Please contact your professional adviser/consultant before making an investment decision.

Where possible we aim to disclose the material risks pertinent to this document. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Unigestion maintains the right to delete or modify information without prior notice.

Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies or financial instruments described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors. Unigestion has the ability in its sole discretion to change the strategies described herein.

To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

No separate verification has been made as to the accuracy or completeness of the information herein. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of information from third party sources. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Additional Information for US Investors

The performance figures are based on estimated fees and expenses as well as on the underlying strategy’s estimated performances given by fund managers, administrators, custodians and third party sources at a given date. Where performance is reflected gross of fees, potential investors should be aware that the inclusion of fees, costs and charges will reduce the overall value of performance. Unless otherwise stated, the performance data source are Unigestion, Bloomberg and Compustat.

This information is provided to you solely to give you background information relating to Unigestion, certain strategies it implements and currently offers. Before making an investment decision with respect to the strategy discussed herein, potential investors are advised to consult with their tax, legal, ERISA and financial advisors. Note that not all strategies may be available or suitable for investment by U.S. investors.

This document may contain forward-looking statements, including observations about markets and industry and regulatory trends as of the original date of this document. Forward-looking statements may be identified by, among other things, the use of words such as “expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar expressions. Forward-looking statements reflect Unigestion’s views as of such date with respect to possible future events. Actual results could differ materially from those in the forward-looking statements as a result of factors beyond a strategy’s or Unigestion’s control. Readers are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward-looking statements in this document

Return targets or objectives, if any, are used for measurement or comparison purposes and only as a guideline for prospective investors to evaluate a particular investment program’s investment strategies and accompanying information. Performance may fluctuate, especially over short periods. Targeted returns should be evaluated over the time period indicated and not over shorter periods.

The past performance of Unigestion, its principals, shareholders, or employees is not indicative of future returns.

Except where otherwise specifically noted, the information contained herein, including performance data and assets under management, relates to the entire affiliated group of Unigestion entities over time including that of Unigestion UK. Such information is intended to provide the reader with background regarding the services, investment strategies and personnel of the Unigestion entities. No guarantee is made that all or any of the individuals involved in generating the performance on behalf the other Unigestion entities will be involved in managing any client account on behalf of Unigestion U.K. More specific information regarding Unigestion UK is set forth herein where indicated and is available on request.

There is no guarantee that Unigestion will be successful in achieving any investment objectives. An investment strategy contains risks, including the risk of complete loss.

The risk management practices and methods described herein are for illustrative purposes only and are subject to modification.

Legal Entities Disseminating This Document

UNITED KINGDOM

This material is disseminated in the United Kingdom by Unigestion (UK) Ltd., which is authorized and regulated by the Financial Conduct Authority (“FCA”).

This information is intended only for professional clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients.

US

This material is disseminated in the U.S. by Unigestion (UK) Ltd., which is registered as an investment adviser with the U.S. Securities and Exchange Commission (“SEC”). This information is intended only for institutional clients and qualified purchasers as defined by the SEC and has therefore not been adapted to retail clients.

EU

This material is disseminated in the European Union by Unigestion Asset Management (France) SA which is authorized and regulated by the French “Autorité des Marchés Financiers” (“AMF”).

This information is intended only for professional clients and eligible counterparties, as defined in the MiFID directive and has therefore not been adapted to retail clients.

CANADA

This material is disseminated in Canada by Unigestion Asset Management (Canada) Inc. which is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (“OSC”).

This material may also be distributed by Unigestion SA which has an international advisor exemption in Quebec, Saskatchewan and Ontario. Unigestion SA’s assets are situated outside of Canada and, as such, there may be difficulty enforcing legal rights against it.

SWITZERLAND

This material is disseminated in Switzerland by Unigestion SA which is authorized and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”).

SINGAPORE

This material is disseminated in Singapore by Unigestion Asia Pte Ltd. which is regulated by the Monetary Authority of Singapore (“MAS”).

Document issued April 2020.