It has been an extraordinary year in many ways. While the medium-term situation still seems favourable to us, we are preparing for the end of the year by reducing part of our positive bias to growth assets. A few elements on the macro side are deteriorating marginally, recent market enthusiasm seems exaggerated to us and valuations may be a short-term obstacle as we wait for the recovery in earnings to continue. For these three reasons, while remaining positive in our positioning, we believe the time has come to take some of the recently accumulated profits. Now is the time for festivities, not reckless risk-taking.

It’s Beginning to Look a Lot like Christmas

What’s Next?

Short-term factors call for a more prudent stance

Among the macro, sentiment and valuation signals that we analyse daily, a number of them are beginning to point to signs of weakness. These weaknesses are only short-term elements to us, but they nonetheless deserve our attention.

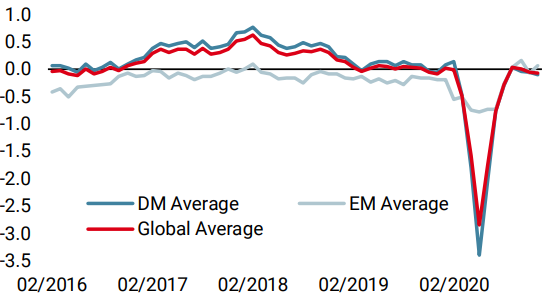

In terms of the macroeconomic situation, our indicators continue to show a risk of recession that ranges from low to neutral, depending on whether we look at the data (Nowcaster) or the media (Newscaster). While this outlook remains positive, we have recently seen our European signals losing altitude and our Chinese Growth Nowcaster registering a rapid decline.

Our Growth Nowcaster for the Eurozone has started to follow the lead of its Newscaster counterpart: it has dropped from a value of 0.08 at the end of October to -0.30 at the time of writing, which is very close to the threshold that we use to differentiate between recession and growth. The decline in the indicator is mainly explained by a drop in data relating to the consumption of durable goods and the expectations of purchasing managers. However, while the symptoms are close to those of March 2020, the amplitude of the declines are lower. Regarding China, a decline in a spectrum of data relating to consumption also explains the recent evolution of the indicator.

On the North American side, there is no visible sign of deceleration for the moment but the number of Covid-19 cases continues to rise, suggesting that the US economy could temporarily slow down in the coming weeks. According to the latest figures, the US has more than 40 new cases per day per 100,000 inhabitants, a trend and level already observed in Europe at the end of October. These three recent developments – Eurozone, China and the US – are not alarming in terms of economic impact, but call for greater caution at the very least.

In terms of the market situation, here again a number of statistics, although not catastrophic, call for a moderation of our very positive bias on risky assets. Regarding sentiment first, investor optimism is evident everywhere and has reached levels that can be regarded as exaggerated over the short term. 88% of shares on the New York Stock Exchange currently trade above their 200-day moving average (compared to 50% a month and a half ago). The AAII survey in the US, which measures the enthusiasm of retail investors, has returned to levels comparable to December 2009 or December 2017. Finally, an analysis of the velocity of recent market movements points to a level of enthusiasm that is too extreme to be sustainable in the coming weeks. Because of this enthusiasm, valuations have risen without any improvement in earnings. Multiples have therefore increased and must be supported by strong company results over the next few quarters otherwise the recovery risks “running out of legs”.

We are less worried about the medium term

We anticipate a continuation of this period of strong economic expansion for three reasons. Firstly, the trend we are observing in our economic indicators remains firm: more than 50% of the growth data we collect is improving while our indicators themselves are around their long-term level. Second, the prospect of vaccine distribution over the first quarter of 2021 suggests that a full reopening of the global economy is fast approaching: again, the future looks more positive than the near past. Finally, the economic situation has not yet fully normalised: savings rates are still high (14% of disposable income in the US, 25% in Europe), while productive capacity utilisation rates remain low (72.8% in the US, 76.3% in Europe). These two factors should normalise in the coming year, further accelerating growth. Further stimulus in the US would only add to the positivity of this medium-term economic situation.

Medium-term expectations remain pessimistic

If the economic situation has scope for improvement, the same applies to expectations as well as valuations.

On the expectations front, economists and analysts are remarkably aligned. Economists anticipate real growth in the economy of 5.2% in 2021: only 1.5% more than the historical average of the past few years. Analysts expect sales growth for S&P 500 companies to be 7.1% (vs 9.7% in 2017) and 6.1% for the DAX (vs 3.1% in 2017), strong growth that remain comparable to 2017 – a good year from an economic point of view, but without a stimulus on the scale observed today.

We expect nominal growth next year to be around 6% in the US and 5% in Europe. However, neither economists nor analysts seem well prepared for the scale of this recovery and an analysis of hedge fund positioning reveals a similar outlook: their beta to global equities has regained some colour without exceeding their long-term average. The term structure of the VIX remains in excess of its long-term average for all maturities.

To formulate the same idea differently, if our scenario is a strong continuation of the recovery already observed, the risk accompanying this scenario is not a return to recession. The risk is that the scale of the recovery could lead to unexpected inflation. We are not there yet, but our inflation indicators are showing signs of renewed vigour, and we need to remain defensive on fixed income assets such as bonds.

Finally, the scale of this recovery should improve the situation in terms of valuation. A spectrum of measures – both backward-looking and forward-looking – now show extreme valuations within global equities (on average between their historical 85th and 95th percentiles) but stronger-than-expected growth in corporate earnings should allow them to return to less discouraging levels: earnings growth should justify the expansion of multiples. Beyond equities, there are also market segments that still do not reflect the recovery we are currently experiencing. This is notably the case for emerging currencies and the energy complex. There are therefore still pockets of expected performance to tap.

If the recovery is in line with our expectations, these short-term risk factors that we see will eventually give way to the medium-term factors listed above. We have eased our positioning in terms of growth assets, as inflation risk increases and investor optimism is tempered by the extraordinary returns observed at the end of the year. We therefore maintain a positive bias, but have reduced it for short-term reasons. January should lead us to regain greater exposure to the growth theme.

Unigestion Nowcasting

World Growth Nowcaster

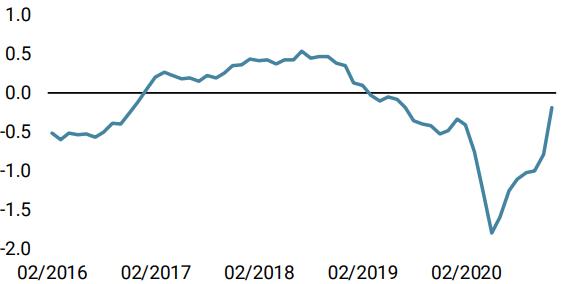

World Inflation Nowcaster

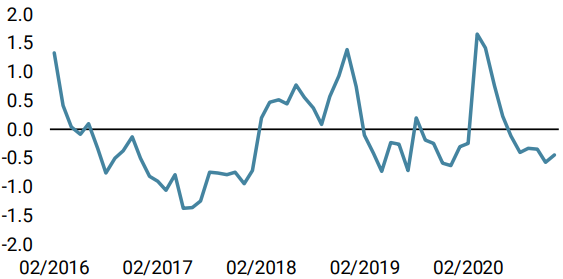

Market Stress Nowcaster

Weekly Change

- Our World Growth Nowcaster decreased last week, as DM economies showed marginally weaker data series.

- Our World Inflation Nowcaster is on the rise: inflation risk is high now.

- Last week, our Market Stress Nowcaster remained unchanged as most of its components were stable.

Sources: Unigestion. Bloomberg, as of 14 December 2020.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore (MAS). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).