As the new decade approaches in the coming weeks, which are the key elements that are likely to persist from those that we have seen in the years that have followed the Great Financial Crisis? In our view, from an economic perspective, there are two important (and connected) facts that best characterise this period. Firstly, it is the first recession-free decade in US economic history. Secondly, never in the modern era have central banks owned as many financial assets as they do today. Will this situation last over the years to come, and what will it mean for asset allocation? From the 1970s through to 2008, the US economy has faced seven recessions, as measured by the National Bureau of Economic Research. That amounts to at least one every decade. These periods were characterised by specific contexts. We had the “great inflation” from the mid-1970s to the mid-1980s, the “great deregulation” during the 1990s, and the “great moderation” between 2003 and 2007, as defined by Stock and Watson, who made reference to the low volatility of macroeconomic data observed after the tech bubble and before the Great Financial Crisis (GFC). Over these four decades, the business cycle mattered for the US economy, with phases of expansion, overheating, slowdown and then recession. We also observed a large variation in inflation, labour costs and energy prices. Although we had a European recession in 2012 and saw a slowdown in emerging markets, the current decade will be the first without a US recession. More importantly, the volatility of key US macro data, such as GDP, consumption, investment and consumer prices, has never been as low as during this decade. It is even lower than that seen during the “great moderation”. Since 2010, realised volatility for US GDP growth has been 0.7%, compared to 2.2% in the 1970s and 1.4% between 2000 and 2010. One can observe a similar pattern for inflation: 1.4% this decade versus 2.3% in the previous one. With variations in economic activity becoming smaller and smaller, does this point to an end of the business cycle? There are usually three key dimensions which best characterise an economic context: monetary policy, fiscal policy and global trade. Over the last ten years, each of these have evolved markedly. Central banks across the world have strongly supported activity with accommodative monetary policy through “traditional” rate cuts initially and then quantitative easing. That support pushed things into uncharted territory for three reasons: 1) the move has been synchronised across the world; 2) the size of liquidity injections has been large; 3) the length of the support has never been seen before. Fiscal policy has been either supportive, like in the US and China, or neutral, as in Europe or Japan. Finally, the growth in global trade has been negative over the last ten years for the first time since 1960. Data from the World Bank showed that merchandise trade increased from 16% (of global GDP) in 1960 to 47% in 2010, increasing by around 10% of global GDP per decade despite recessions during this period. Currently, it represents 46%, a lower number than ten years ago and sharply lower than the peak of 52% observed in 2008 before the GFC. This is largely due to a deleveraging of the global economy and illustrates how the drivers of the global economy have changed. In our view, the lower variation in GDP stems mainly from a higher weight of services in the US and the global economies. Consumption of services currently represents 18% of US GDP vs 11% in 1970. Data from the IMF also highlights that trade in services has continued to grow over the decade, rising from 10% to 13% of global GDP over the period, while trade in goods has declined, as mentioned previously. Services are less cyclical than manufacturing activities. Consequently, their rising weight in the global economy and in employment creates lower changes in inventories, which feeds into more stable supply chains and thus a more stable economy.“Ten Years Gone” – Led Zeppelin, 1975

What’s Next?

The End of the Business Cycle?

The Situation Reflects a Changing US and Global Economy

These changes in the structure of the global economy have increased polarisation across sectors, countries and political systems. The impact of these factors has increased over the last few years. Polarisation has concerned “Disruptors” versus “Disrupted”, “Services” versus “Manufacturing”, “Rates sensitive” versus “Rates non-sensitive” and “Exposed to globalisation” versus “Non-exposed”. Consequently, the winners of the decade, mainly big tech companies, are not the same as in previous ones: essentially cyclical companies benefiting from globalisation (such as in the materials sector).

The dispersion of returns within asset classes has also increased. As an illustration, the gap between value stocks and growth stocks is at a record high. Since 2009, the MSCI World IT index has delivered 15.4% a year on average versus only 2% and 5.8% respectively for the MSCI World Energy and the MSCI World Bank indices. Over the same period, the MSCI World index has outperformed the MSCI World equal weighted index by 29%. The main consequence of this trend is a rise in inequality because new winners benefit from the “first takes all” theory that tend to create oligopolies.

While inequalities in developed and emerging countries have expanded due to lower GDP growth, it is clear that governments and financial institutions will do “whatever it takes” in the future to prevent any economic shock in order to maintain social stability. As a result, a supportive policy mix would last, and potentially be amplified, in the case of an economic slowdown. We believe that this will maintain the volatility of macroeconomic variables at a low level, reduce the risk of large shocks and reduce the probability of sustained financial turmoil. Consequently, we expect a reduction in the risk premium of most liquid risky assets. Does this mean that equities will become the new bonds, delivering income with a low risk of drawdown? Based on returns delivered during the current decade, we would argue yes. Over the last nine years, US equities have returned the best excess return on average since 1986 (13% per year), higher than those seen in the 1980s (9%), 1990s (12%) and those delivered between 2000 and 2009 (-1%). The Sharpe ratio has also improved, while realised volatility has been consistently lower on an historical basis since 2010. We observe a similar pattern for US high yield. This result is even more exceptional because it has been realised in a context of low growth and low inflation. We are all aware of the magic driver: low interest rates. Will they stay low in the coming years?Lower Macro Volatility Implies a Weaker Financial Shock

Of course, it is always difficult to make forecasts for asset returns for the next decade. Who would have forecast in 2009 that negative bond yields would represent more than 30% of the Barclays Global Aggregate market capitalisation? Ten years ago, everybody thought that accommodative monetary policy would be inflationary. Who would have guessed that despite the biggest monetary experiment of all time, that there would be no inflationary pressures.

Our conviction is that the world has changed and that, for different reasons, central banks will remain active and supportive. Rather than debate the legitimacy of this stance, we prefer incorporating this element into our asset allocation as fact and anticipating what kind of consequences this will have on investors and the global economy. Our view is simple: bond yields will remain at low levels, and that the probability of us singing David Bowie’s “Golden Years” in 2029 is not negligible.

Ten Years Gone

Our medium-term view is currently constructive: we are still overweight growth assets and underweight precious metals. Given the current cost of hedging, we are using forex based strategies exposures to hedge ourselves against adverse market conditions. Over the month of November to date, the Uni-Global – Cross Asset Navigator fund is up 1.0% versus a 1.7% return for the MSCI AC World Index and a -0.9% return for the Barclays Global Aggregate (USD hedged). Year-to-date, the Uni-Global – Cross Asset Navigator has returned 11.0% versus 21.4% for the MSCI AC World index, while the Barclays Global Aggregate (USD hedged) index is up 7.6%.Strategy Behaviour

Performance Review

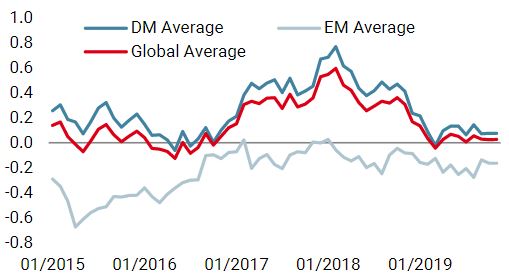

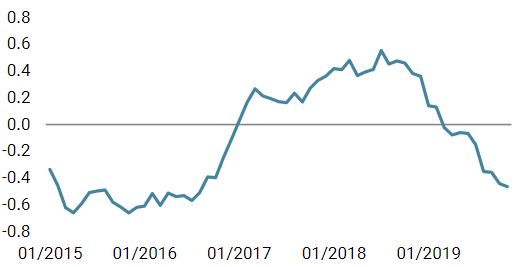

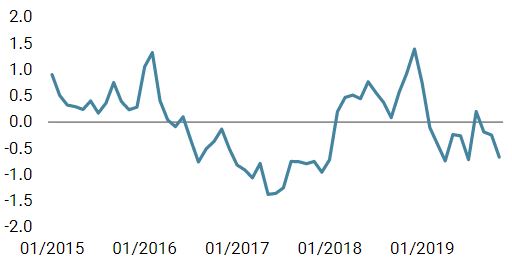

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Our world Growth Nowcaster remained unchanged this week, as both emerging and developed economies showed further signs of stabilisation.

- Our world Inflation Nowcaster went through a slight decrease last week but its diffusion index continues to indicating a stabilisation period.

- Market stress decreased, driven by all its components.

Sources: Unigestion. Bloomberg, as of 11 November 2019.

Navigator Fund Performance

| Performance, net of fees | 2018 | 2017 | 2016 | 2015 |

| Navigator (inception 15 December 2014) | -3.6% | 10.6% | 4.4% | -2.2% |

Past performance is no guide to the future, the value of investments can fall as well as rise, there is no guarantee that your initial investment will be returned. Returns may increase or decrease as a result of currency fluctuations.

Important Information

Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed by recipients to any other person. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in the investment vehicles to which it refers. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Please contact your professional adviser/consultant before making an investment decision.

Where possible we aim to disclose the material risks pertinent to this document, and as such these should be noted on the individual document pages. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors.

To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of this information. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Uni-Global – Cross Asset Navigator is a compartment of the Luxembourg Uni-Global SICAV Part I, UCITS IV compliant. This compartment is currently authorised for distribution in Austria, Belgium, Denmark, Finland, France, Germany, Ireland, Italy, Luxembourg, Netherlands, Norway, Spain, UK, Sweden, and Switzerland. In Italy, this compartment can be offered only to qualified investors within the meaning of art.100 D. Leg. 58/1998. Its shares may not be offered or distributed in any country where such offer or distribution would be prohibited by law.

No prospectus has been filed with a Canadian securities regulatory authority to qualify the distribution of units of these funds and no such authority has expressed an opinion about these securities. Accordingly, their units may not be offered or distributed in Canada except to permitted clients who benefit from an exemption from the requirement to deliver a prospectus under securities legislation and where such offer or distribution would be prohibited by law. All investors must obtain and carefully read the applicable offering memorandum which contains additional information needed to evaluate the potential investment and provides important disclosures regarding risks, fees and expenses.

All investors must obtain and carefully read the prospectus which contains additional information needed to evaluate the potential investment and provides important disclosures regarding risks, fees and expenses. Unless otherwise stated performance is shown net of fees in USD and does not include the commission and fees charged at the time of subscribing for or redeeming shares.

Unigestion UK, which is authorised and regulated by the UK Financial Conduct Authority, has issued this document. Unigestion SA authorised and regulated by the Swiss FINMA. Unigestion Asset Management (France) S.A. authorised and regulated by the French Autorité des Marchés Financiers. Unigestion Asia Pte Limited authorised and regulated by the Monetary Authority of Singapore. Performance source: Unigestion, Bloomberg, Morningstar. Performance is shown on an annualised basis unless otherwise stated and is based on Uni Global – Cross Asset Navigator RA-USD net of fees with data from 15 December 2014 to 11 November 2019.