Aided by the very sharp improvement in both macro conditions and market sentiment, financial markets have resurged in Q2, recouping a good part (if not all) of the losses incurred during the Covid-19 shock. The repricing in growth related risk premia has been broad-based, but their path and scale have varied significantly within and across asset classes, and with it the need to adjust portfolio exposures accordingly. Central banks’ intervention, political risks and uncertainties on sanitary matters have had a strong impact on risk taking. In previous publications, we emphasised cross-asset relationships within the current macro and micro environments. This time, the focus will be on corporate credit, as the message it conveys is somewhat different from what the stock markets are saying. In our opinion, the balance of risks for credit has deteriorated, and the time has come to temporarily reduce the exposure to this asset class.The Balance of Risks has Shifted in Credit

Trim up the Tree

An unprecedented recovery has risen from the ashes of an extraordinary macro shock. Looking at a broad set of economic data from our proprietary growth Nowcaster, there is reason to believe that the resurgence in economic activity is strong, V-shaped, and all the more spectacular in terms of velocity: after contracting into deep recessionary levels in May, unseen since the GFC, our indicator now shows a 75% recovery from the trough. It only took two months to achieve such a U –or rather, V- turn, compared to the 6 to 8 months needed in 2009 to produce the same result. This time, the swift response from both central banks (in terms of monetary policy) and governments (in terms of fiscal support) helped alleviate the burden of a major demand shock on Main Street. Amongst the numerous policies implemented, a key element has been the measures to prevent the credit markets from freezing, allowing companies to access the capital markets to fund their growing cash needs. To do so, the Fed and the ECB materially ramped up the scale and scope of their special credit facilities programmes (PMCCF and SMCCF in the US and PEPP in Europe), enacting massive purchases in investment grade and high yield debt (Fed only), either directly or through Exchange Traded Funds. From lenders of last resort to buyers of first necessity, central bankers created a self-fulfilling prophecy, as investors front-ran their various programmes in a rarely seen buying frenzy. Liquidity conditions were successfully restored in credit markets. Market participants seized the opportunity to chase monetary action and deployed walls of cash into investment grade and high yield instruments; inflows in Q2 outpaced Q1 outflows by a multiple between 3x and 5x, except in the Euro speculative grade segment, which was left out of the ECB’s scope. Hence, the combined effects of monetary measures and economic revival created a virtuous circle, which helped normalize liquidity conditions and greatly benefitted credit investors. From peak to trough, the CDS North America high yield spread contracted by 420bps and the Itraxx Xover by 350bps. In investment grade, the CDX NA IG and Itraxx EUR IG CDS indices tightened by 80bps and 65bps respectively. The message conveyed by the current “post recovery” spreads level is clear: economic activity has already come back strongly but the need to discount sanitary and geopolitical risks remain, as potential headwinds may prevent a complete recovery in the short run. This aligns with what sovereign yields are pricing. Despite a surge in inflation break-evens, nominal rates remain historically low while real rates have dipped into deeply negative territory, another hint that fixed income investors have not yet factored the V-shape into the growth premium. The only asset class currently embedding more favourable expectations are equities, mainly through PE expansion, with valuations anticipating a full blown earnings recovery from -25% in 2020 to +30% in 2021 for the MSCI World. We still think that the aforementioned tailwinds will remain over the long term, but in the short run, the balance of risks seems to have titled in a less favourable direction: Market technicals and fundamentals have deteriorated, while valuations have richened on the back of reduced expected returns. On the demand side of the equation, the second derivative of the significant inflows observed in Q2 is poised to abate. High demand, triggered by policy makers facing record amounts of issuance (the supply side of the equation), a blessing at first, could become a curse if refinancing needs remain elevated while demand fades. In the synthetic space (Credit Default Swaps as compared to cash instruments), the same phenomenon holds true: positioning in most CDS indices have already climbed back to pre-crisis levels. Because of these supply and demand imbalances, spreads could come under upward pressure at a very inopportune time, when downgrades and defaults have yet not seen their respective peaks. Research shows that actual defaults doubled year-on-year at the end of June in the high yield space –the one most at risk under current circumstances – from 3.3% a year ago to 7.3%. Expected default rates are likely to surge until the first half of 2021, to reach an estimated 10% to 13% in the US, and 6% to 8% in Europe. Recovery rates should also be lower than usual as debt is currently being used to compensate the lack of cash flow, rather than for capex purposes. Another drag preventing spreads to tighten further in the short run can be found in the lower end of the risk spectrum. When breaking the market down into rating buckets, the CCC segment lagged its higher rated speculative peers on a risk-adjusted basis. The recovery in spreads trailed higher quality names, as a sizeable number of issuers in this segment are facing secular headwinds, especially in the energy and consumer related industries still feeling the pain of the prolonged demand shock. The obstacles posed by a sustained sanitary status quo will continue to constrain risk appetite as long as the cyclical issues in sectors most affected by this crisis are not addressed for good. Finally, the recent compression in spreads and their associated capital gains have weighed on expected returns (the valuation side). Current spread levels in investment grade (sub 70bps in both US and Europe CDS Indices) and high yield (450bps in the US and 340bps in Europe) have historically returned 0.2% and 0.7% in the three months that followed. This measure rises to 0.4% and 3% over a 12-month horizon. In comparison, expected returns at the end of March neared 10% in high yield and 2% in investment grade. As much as carry became attractive during the crisis, we believe that the current valuation of these risk premias is insufficient to cover the associated risks posed by today’s macroeconomic context. In light of the above-mentioned deterioration in sentiment and valuation for this asset class, we have decided to trim our credit exposures for the weeks to come, back from an overweight to a more neutral stance, especially ahead of August and its seasonal liquidity droughts. We prefer a moderate overweight in equities, where we believe that multiples have greater room to expand as opposed to credit spreads’ potential to tighten.What’s Next?

The macro framework remains favourable…

…but headwinds remain

Adjusting dynamically to this shift in the balance of risk

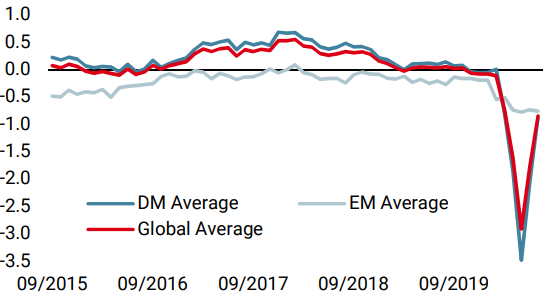

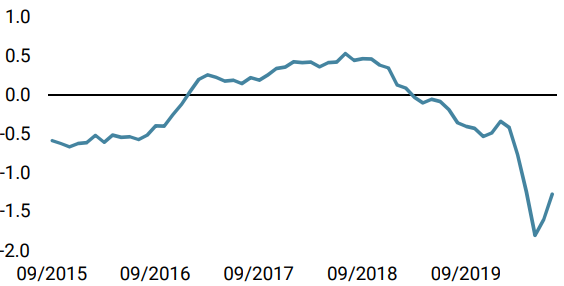

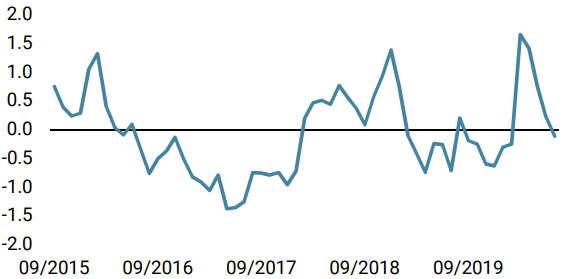

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Our world Growth Nowcaster increased across most countries.

- Our world Inflation Nowcaster barely changed last week, as most countries remained unchanged.

- Our Market Stress Nowcaster was largely unchanged last week, with its three components showing little movement.

Sources: Unigestion. Bloomberg, as of 27 July 2020.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore (MAS). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).