June capped off a remarkable first half of the year for financial markets as investors continued deploying capital following the post-coronavirus economic recovery. The rally in cyclical assets during Q1 expanded to the broader market as vaccine rollouts and supportive monetary policy provided the seeds for a “Goldilocks” environment. Looking ahead, the key question now is what supports, if any, are left for markets. In our view, there remain significant tailwinds for risky assets although we readily acknowledge the spectre of inflation, which could provide a wakeup call for investors in the months ahead.

I Want to Take You Higher

What’s Next?

A strong, cyclical-led market rally

Heading into 2021, our core view for the year was a “Goldilocks” environment: growth would recover strongly but slack in the economy would limit inflationary pressures, allowing central banks to remain accommodative in the fight against unemployment. The crowded trades from last year (Tech, Pharma, Momentum) would be unwound in favour of the laggards (Energy, Financials, Value). The resumption of global trade would support cyclical commodities, while volatility would continue to decline.

While not all of our calls have panned out, H1 has largely transpired as we expected. The Energy and Financial sectors (33% and 21%) have both outperformed Tech (13%) over the period, while Value (15%) has outpaced Momentum (7%). Cyclical commodities, and Energy especially (45%), have been the highest performing assets, while precious metals (-8%) like gold (-9%) are down on the year. While we expected monetary policy to remain supportive, we must admit that the fall in bond yields over Q2 has been surprising, even if they are up on a year-to-date basis. Global equities have benefited from this supportive context, with the MSCI All Country World finishing June up 12% year-to-date.

With the strong returns seen across nearly all markets and many of our end-of-year calls already met, it is critical to assess what supports remain for our core view. As we look across the different dimensions we monitor, we still see some significant tailwinds that lead us to continue holding our core view for the year.

We see three key supports for our positive view on markets

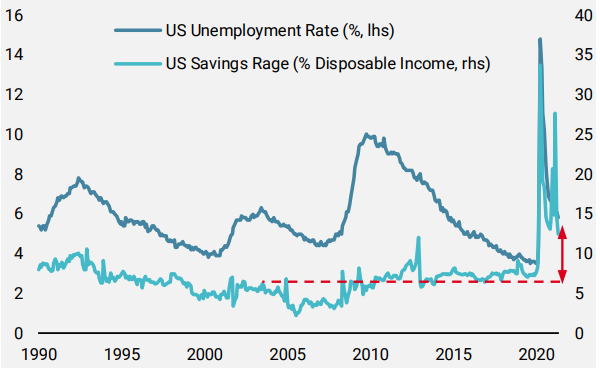

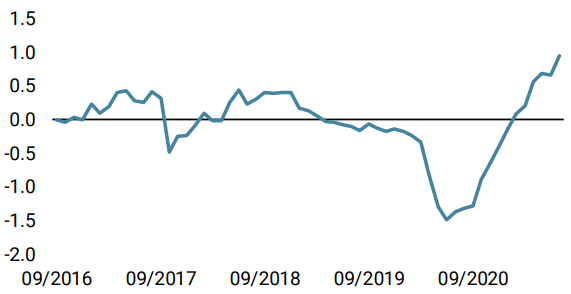

As we have communicated recently, our Global Growth Nowcaster has hit historical highs but there are underlying drivers that remain subdued. In particular, the consumption and investment sub-components are lagging the broader recovery and have only recently improved significantly. If they continue their trend, as we expect them to thanks to economic reopening, they will provide another sustainable leg of support to the macro recovery. As Figure 1 shows, with unemployment elevated, households are holding onto their savings in the meantime and are cash-rich in aggregate, providing a potent source of future demand when their spending normalises.

Figure 1: Unemployment and Savings Rates

Source: Unigestion, Bloomberg, as of 1 July 2021.

Moreover, as we discussed last week, central bank policy is far from tightening, despite the recent FOMC meeting. While some central banks (Bank of Canada, Norges Bank, as well as some in the emerging world) have shifted to a hawkish tone, the Fed remains patient. Indeed, it has been the most dovish members that have anchored the Fed Funds Target rate, and their projections call for no hikes over the next two years. Total asset purchases across the world’s central banks also continue to grow, albeit at a slower pace than at the end of last year.

Finally, market aversion toward risk-taking remains. While the VIX has grinded downwards over H1, longer-dated futures contracts remain elevated, leading to a steep VIX curve. At the same time, some systematic strategies like trend following continue to have a smaller capital allocation to risky assets such as credit spreads and equities than they did at the end of 2019. As volatility continues to decline, these strategies are likely to increase their exposures and provide further support to these markets.

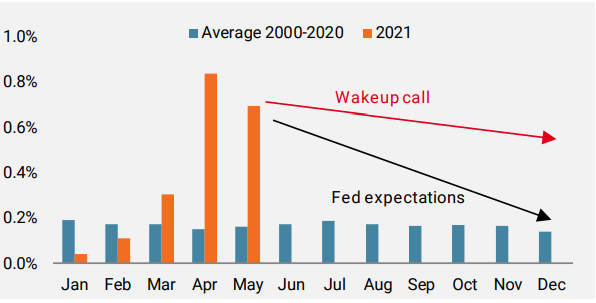

The spectre of inflation looms large as the spoiler to our view

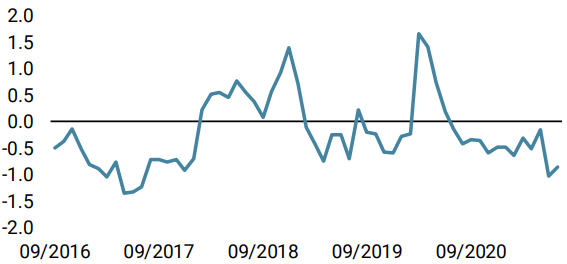

In addition to our core “Goldilocks” view, we had called out a genuine inflation overshoot as our most probable risk scenario at the start of the year. And over the last few months, macro conditions have shifted more and more in this direction, with investors following suit. Nonetheless, the consensus seems to agree with the Fed that the current surge in inflation is temporary. As Figure 2 highlights, the recent levels of inflation are quite stark, and if a demand surge meets still-constrained supply chains, the transitory inflation expected by the Fed and others could become more persistent.

Figure 2: Monthly Change in US CPI ex Energy

Source: Unigestion, Bloomberg, as of 1 July 2021.

Such a wakeup call could trigger a sudden shift in market expectations, with bond yields shifting meaningfully and quickly higher, thereby threatening the valuations of many assets that have benefited from the low level of yields. For example, in our own historical valuation metric, an increase in global bond yields of 50bps would shift developed market equities from fair-valued to expensive, all else being equal.

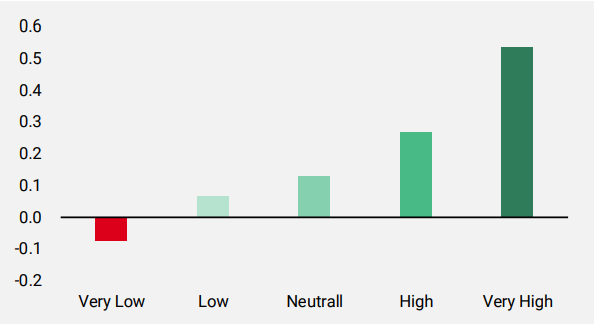

A sharp upward move in bond yields would likely trigger a period of market stress, as investors realign their expectations and reassess the value of their investments. One of our preferred exposures to hedge this risk is a broad long US dollar against other currencies. As Figure 3 shows, the greenback performs very strongly in periods of high market stress, as investors reduce their exposure and shift to holding safe assets denominated in US dollars. Furthermore, many investors, such as macro hedge funds and CTAs now appear to be short the dollar, creating room for a short squeeze in such a scenario.

Figure 3: Excess Sharpe Ratio of Fed Trade-weighted Dollar Index by Market Stress Regime

Source: Unigestion, Bloomberg, as of 1 July 2021.

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster remained steady as a modest slowing in China was offset by an improving picture in Europe.

- Our World Inflation Nowcaster moved higher again on the back of stronger inflationary pressures in the Eurozone.

- Our Market Stress Nowcaster moved up slightly due to a pick up in volatility last week.

Sources: Unigestion. Bloomberg, as of 1 July 2021

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).