The USD has been on quite an impressive journey over the last couple of years, with clear but different market drivers characterising its moves. Since last summer however, the path has been relentlessly higher, finally breaching the Covid highs in recent weeks. To this day and despite the challenges, the USD has successfully kept its dominance as the world’s reserve currency, thanks to its liquidity, lack of meaningful contenders, and its central bank’s credibility. Following an impressive +7% rise year-to-date, we will analyse if this momentum can continue or whether the USD faces the threat of a meaningful reversal. As with most asset classes, dispersions have been large amongst currencies and as monetary normalisation continues to unfold, this scenario is likely to persist.

The Million Dollar Song

Star Alignment

Safe haven

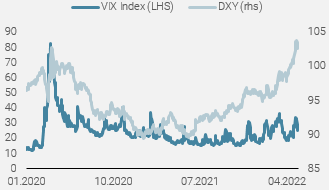

Thanks to its world reserve currency status and high liquidity, the USD is the investor’s undisputed safe haven currency of choice. Its safe haven status has been demonstrated many times in the past during various economic crises, the latest being Covid 19, where the US Dollar index jumped +8% in just over a week. Following the unprecedented monetary and fiscal stimulus that ensued, the USD retraced, as growth-oriented assets recovered significantly, reducing the greenback’s appeal and the need for hedges. The appearance of the delta variant in late 2020 also coincides with the lows made in the US Dollar index; as uncertainty increased again, so did the demand for US dollars. As fears shifted away from the delta variant and towards the central banks, market stress remained high and sentiment weakened, further supporting the dollar and marking the beginning of the bull market we are experiencing to this day.

Figure 1: The US dollar reacts well to market stress episodes

Source: Bloomberg, Unigestion as of 05.05.2022

With the high uncertainty persisting from both central bank normalisation and the ongoing Ukrainian conflict, USD demand will likely remain firm for now.

Central banks

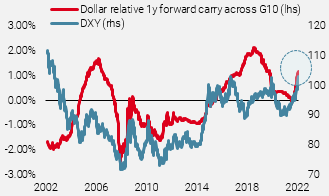

Central banks are indeed a very important component in driving FX price action and particularly the US Federal Reserve (Fed) for obvious reasons, given the influence it has on the world’s reserve currency. As the Fed turned increasingly hawkish to tackle inflation head on, the interest rate differential unsurprisingly became a natural tail wind for the USD.

Figure 2: Positive carry is an important tailwind for the USD

Source: Bloomberg, Unigestion as of 05.05.2022

Although the Fed was among the early major G10 central banks to turn hawkish, there was always the risk that the others would converge towards that hawkish stance, potentially becoming a headwind for the long USD trade. In other words, peak Fed hawkishness had been reached and priced in, whereas other central banks were still catching up, leaving room for their currencies to appreciate. However, this argument suffered a major setback when the war in Ukraine started. Indeed, Europe, which makes up the bulk of G10 currencies, is much more at risk from the conflict from a macro perspective than the US, given its openness and dependence on energy imports from Russia and the resulting price shock. This means that the US effectively has more room to tighten monetary policy compared to Europe, keeping the interest differential wider and thus favouring the US dollar.

Interestingly, looking at Europe and the ECB, whose primary mandate is to achieve price stability through low inflation (+2% over the medium term), the overall message continues to be dovish, especially when compared to its neighbours. Although some members are now acknowledging that the ECB is falling behind the curve on inflation, a majority seem to favour a gradual approach, given the uncertainty on growth caused by the ongoing Ukrainian invasion. Although the ECB will start to scale back its bond purchases, in addition to some rate hikes now priced in by the market for this year, is should normalise at a slower pace than other western central banks. The Fed on the other hand, which has a “dual” mandate of achieving stable prices and maximum sustainable employment, is currently obsessed with tackling inflation. The message from this week’s FOMC meeting was clear: nothing will derail “fighting inflation” as a top priority for the Fed. This hawkish bias implies tighter financial conditions, which will prove a challenge for most assets classes and should keep USD demand firm, both from a safe haven and an interest rate differential perspective.

Macro

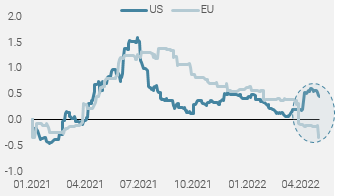

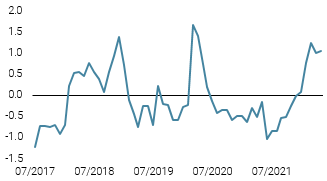

An important driver behind any foreign exchange move is the underlying macroeconomic environment. A simplified notion is that a strong economy will see capital inflows, which then naturally strengthens the underlying currency. There was a strong case early 2022 that the EUR would benefit from capital flowing from US to European indices, which have a “Value” tilt and tend to perform well in a rising rates environment. However, the Ukrainian conflict has lifted the odds of a European recession while US macro momentum remains firm for now. From a macro perspective, the case of a stronger USD therefore holds, as can be seen from the recent divergence between our EU and US Growth Nowcasters.

Inflation remains a concern for most major economies today and here again the notion of foreign exchange is pertinent, as a weaker currency is inflationary in itself (imports become more expensive). This has been a concern, notably for Poland, which was quick to raise rates in an attempt to limit the fall in its currency following the Russian invasion of Ukraine. ECB board member Villeroy also said last week: “a too weak EUR would go against the ECB inflation target”.

Central banks are in a complex situation, having to balance the threat of very high inflation without killing growth, which they tried to stimulate for years. This normalisation process brings large divergences that will continue to widen and undoubtedly affect currencies. Some countries will also be keen to use FX as a policy tool, given its macro implications.

Figure 3: Divergence between the US and EU Growth Nowcaster

Source: Bloomberg, Unigestion as of 05.05.2022

Emerging markets started an aggressive rate hike cycle in early 2021. For example, Brazil hiked its Selic rate by 10.75% from record low levels in late 2020 / early 2021. This explains why some EM Currencies such as the BRL have outperformed the USD significantly year-to-date. Here again, dispersions are large and a majority of FX pairs are down against the US Dollar on a year-to-date basis.

Conclusion

The current market environment remains challenging as uncertainty continues to dominate. Central banks are focused on tackling inflation, which has undermined asset valuations and negatively affected sentiment. Tighter financial conditions mean most assets are likely to continue falling, or at least until short-term and long-term inflation expectations converge towards central bank targets. However, dispersions remain and generally speaking, the current environment should continue to favour the USD. It is worth noting that positioning is increasingly tilting towards the long USD trade and that, after making fresh year-to-date highs not seen since 1990 and March 2020, the US Dollar Index’s momentum is bound to slow.

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster fell further, largely due to worsening European and Chinese data.

- Our World Inflation Nowcaster ticked lower with easing inflationary pressures in the US and China.

- Our Market Stress Nowcaster moved slightly higher as liquidity conditions deteriorated further.

Sources: Unigestion, Bloomberg, as of 09 May 2022

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).