-

Private equity market statistics do not yet show the full impact of the COVID-19 crisis, but we expect that investment and exit activity will fall significantly in 2020.

-

We expect a number of investment opportunities to emerge from the current crisis, particularly among small and mid-market companies and secondaries.

-

In Q1 2020, Unigestion contributed EUR 248 million to investments and received distributions on investments of EUR 152 million and completed a large secondary sale.

Overview

The first quarter of 2020 will forever be defined by the emergence of the COVID-19 pandemic. However, since the various lockdowns across the globe were not put in place until mid-March, private equity market statistics do not yet show the full impact of the crisis. Global investment activity showed a modest decline compared to the first quarter of 2019. Nevertheless, the APAC region, where the impact of the virus was felt much earlier in the quarter, posted a significant 40% decline in deal activity. Meanwhile, the decline in exit activity was more pronounced, continuing a downward trajectory from 2019.

Mega Buyouts Prop Up the Market

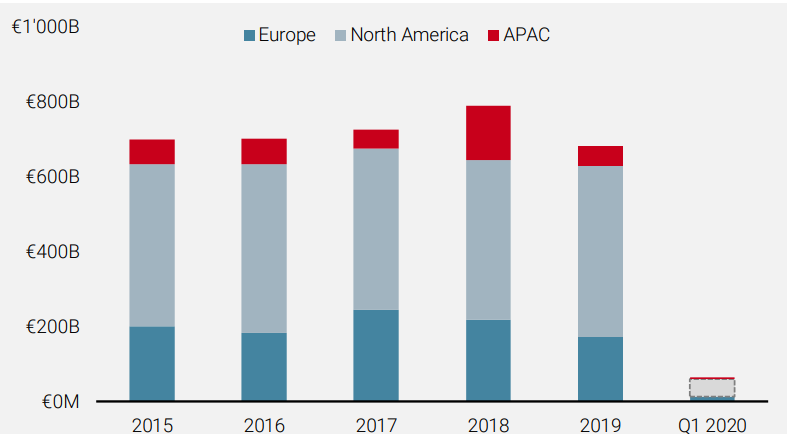

The global aggregate value of private equity deals closed during Q1 2020 was EUR 141bn, 6% down on the same quarter last year1. This decline was driven by a slump in deal activity in APAC, while activity was flat in Europe and actually rose by 3% in North America.

However, when one dips below the surface, the story becomes more nuanced. Due to a small number of mega buyouts, the volume of deals greater than EUR 2.5bn increased by 200% in Q1 versus the same quarter last year. The largest deal closed was the acquisition of German-based Thyssenkrupp Elevator AG, a manufacturer of lifts and escalators, by Advent International, Cinven and the RAG Foundation for EUR 17.2bn. In the US, Searchlight and ForgeLight acquired a majority stake in Univision Communications, the leading Hispanic media company in the US, in a deal that values it at USD 9.7bn.

Meanwhile, the fall in global exit activity was more acute (see Figure 1). The global aggregate value of exits in Q1 2020 was EUR 51bn, more than 50% down on the same quarter last year. No region was immune from this with North America (-58%), Europe (-44%) and APAC (-62%) all showing significant declines.

Despite the extreme volatility in the stock markets, private equity fundraising continued to show resilience. In total, USD 133bn was raised in Q1 20202. This was a 13% increase versus the same quarter last year despite the number of funds closed being almost 30% down. This suggests that, yet again, the large end of the market has been propping up volumes.

We expect that certain strategies, such as secondaries and small and mid-market investments, will benefit from attractive opportunities

It seems clear that, in the coming months, the private equity market will be significantly impacted by the COVID-19 crisis. Firstly, private equity companies operating in certain sectors, such as non-food retail, transportation, leisure and hospitality, will see material valuation write-downs. Secondly, we expect investment, and especially exit activity, to temporarily collapse. Finally, while many investors will view this as a good time to commit to private equity funds, fundraising in general will soften this year as certain investors grapple with liquidity constraints.

Nevertheless, once the dust has settled, we expect that certain strategies, such as secondaries and small and mid-market investments, will benefit from attractive opportunities driven by lower valuations, limited debt availability and an increase in motivated sellers.

Figure 1: Exit activity (EUR bn)

Resilience in a Crisis

In early April, we reported to clients our first assessment of the likely impact of the COVID-19 crisis on our funds and mandates by assessing the situation of the portfolio companies representing 80% of the NAV of each programme. For each company, we considered both the impact on value and the financial headroom. On one hand, we found that most companies will likely see, to a varying degree, a negative effect on valuation. On the other hand, most companies so far have sufficient financial liquidity to survive even a prolonged crisis. The full presentation of this assessment is available on our investor portal.

There are companies in our portfolios that are actually seeing a positive effect from the current crisis

There are also companies in our portfolios that are actually seeing a positive effect from the current crisis. Agro Merchants is a cold storage operator serving the food industry, with 66 facilities in 12 countries. As the market leader in providing cold-chain solutions for food commodities (e.g., beef, chicken, pork, seafood, fruit and vegetables), Agro has state-of-the-art automated handling and processing capabilities. With increased demand from the end consumer and pressure from food companies to provide continuous supply in an uncertain global environment, all of Agro’s facilities are currently operating at full capacity. Furthermore, the company will be able to continue its buy-and-build strategy in a market where valuations are expected to fall, as smaller family-owned businesses may run into liquidity issues.

Companies which benefit from clear consumer trends and have the right distribution channels are well positioned in the current situation. Voff is Europe’s leading provider of natural premium pet food. It develops and sells fresh pet products with high quality, natural ingredients and minimal processing. Pets are seen today as part of the family and therefore the demand for premium pet food products is constantly increasing. In addition, Voff has developed a sophisticated e-commerce platform which now accounts for roughly two-thirds of sales. As a result, the company has been successfully growing its share of the pet food market across the Nordic and the German-speaking regions.

This crisis is not only testing the resilience of companies, it is also uncovering the true ESG leaders. Kindred, a leading chain of nurseries in the UK, takes seriously the relationship with its employees, customers and communities. As a result of the COVID-19 crisis, nurseries were ordered to close. Following this, Kindred decided to waive fees to parents, even though the company was not contractually obliged to do so. In addition, it has launched an “Inspiration Corner” on its website that provides parents with tips and videos with potential activities for young children. This effort to continue to engage with children and parents who are now at home has been very well received. Finally, while the staff is unable to work, the company has furloughed them which allows them to continue to receive 80% of their salary (paid for by the government). Given that the company has no debt, it should be able to withstand over ten months of zero revenue.

High ESG standards are critical for small- and mid-market companies whose success depends on trust and loyalty from its employees and customers

We believe that these examples highlight the attraction of small- and mid-market companies. Such companies are resilient in their own right thanks to strong market positions, management and financials, and are able to implement their growth plans irrespective of market conditions. In addition, high ESG standards are critical for small- and mid-market companies whose success depends on trust and loyalty from its employees and customers.

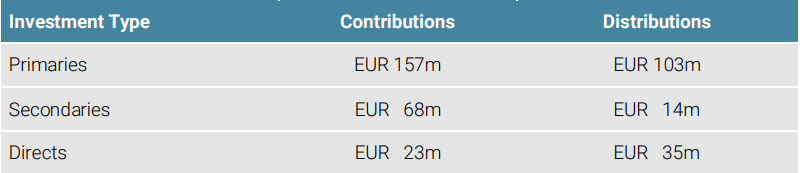

Unigestion Private Equity Investment Activity

In the first quarter of 2020, Unigestion contributed EUR 248 million to investments. We closed commitments to two new primary funds, two new secondary transactions and two new direct deals. In the same period, Unigestion received distributions on investments of EUR 152 million and completed a large secondary sale.

Figure 2: Investment Activity in Q1 2020

In January, we completed the sale of 28 funds on behalf of four different investment programmes to two different buyers in a process that began earlier in 2019. The funds concerned were of older vintages and had limited upside left. Given the size of the transaction and the quality of the underlying portfolios, we were able to generate significant interest from multiple secondary buyers. Ultimately, we achieved an attractive price of 97.4% of net asset value.

In the same month, we committed to Avallon III, managed by one of Poland’s pioneers in management buy-outs. Avallon has participated in over 100 such transactions since 2001. The fund manager seeks to invest in niche leaders across Poland’s most exciting industries, including consumer goods, business-to-business services, e-commerce and manufacturing.

We also finalised the exit of our investment in WCG, the world’s leading provider of solutions that measurably improve the quality and efficiency of clinical research. In August 2016, we participated in a recapitalisation of WCG which valued the company at USD 970m. During our investment, the company grew both organically and through multiple acquisitions, increasing revenues by over 150%. An investor group led by Leonard Green & Partners acquired the company for USD 3.2bn, delivering a 3.5x multiple on our original investment.

In February, we completed the first investment in our new direct programme. HealthTech BioActives (HTBA), is a Spanish manufacturer of flavourings, sweeteners and active pharmaceutical ingredients such as flavonoids derived from citrus fruits and other plants, as well as B12 vitamin derivatives and other substances. HTBA is well known for the quality of its products and is a well-established innovation leader with patented products and processes. In addition, HTBA’s technological know-how acts as a barrier to entry, protecting it against competition. The aim is to further grow the company through an expansion of the product portfolio and customer base, as well as through enhancements to production processes. The ultimate demand for HTBA’s products is being driven by an ageing population and rising health awareness, which allows the company to grow even in the current environment.

1Pitchbook, April 2020.

2Preqin, April 2020.

Important Information

Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed (in whole or in part) by recipients to any other person without the prior written consent of Unigestion. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in either the investment vehicles to which it refers or to any securities or financial instruments described herein. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Such documentation contains additional information material to any decision to invest. Please contact your professional adviser/consultant before making an investment decision.

Where possible we aim to disclose the material risks pertinent to this document. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Unigestion maintains the right to delete or modify information without prior notice.

Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies or financial instruments described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors. Unigestion has the ability in its sole discretion to change the strategies described herein.

To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

No separate verification has been made as to the accuracy or completeness of the information herein. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of information from third party sources. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Additional Information for US Investors

The performance figures are based on estimated fees and expenses as well as on the underlying strategy’s estimated performances given by fund managers, administrators, custodians and third party sources at a given date. Where performance is reflected gross of fees, potential investors should be aware that the inclusion of fees, costs and charges will reduce the overall value of performance. Unless otherwise stated, the performance data source are Unigestion, Bloomberg and Compustat.

This information is provided to you solely to give you background information relating to Unigestion, certain strategies it implements and currently offers. Before making an investment decision with respect to the strategy discussed herein, potential investors are advised to consult with their tax, legal, ERISA and financial advisors. Note that not all strategies may be available or suitable for investment by U.S. investors.

This document may contain forward-looking statements, including observations about markets and industry and regulatory trends as of the original date of this document. Forward-looking statements may be identified by, among other things, the use of words such as “expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar expressions. Forward-looking statements reflect Unigestion’s views as of such date with respect to possible future events. Actual results could differ materially from those in the forward-looking statements as a result of factors beyond a strategy’s or Unigestion’s control. Readers are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward-looking statements in this document

Return targets or objectives, if any, are used for measurement or comparison purposes and only as a guideline for prospective investors to evaluate a particular investment program’s investment strategies and accompanying information. Performance may fluctuate, especially over short periods. Targeted returns should be evaluated over the time period indicated and not over shorter periods.

The past performance of Unigestion, its principals, shareholders, or employees is not indicative of future returns.

Except where otherwise specifically noted, the information contained herein, including performance data and assets under management, relates to the entire affiliated group of Unigestion entities over time including that of Unigestion UK. Such information is intended to provide the reader with background regarding the services, investment strategies and personnel of the Unigestion entities. No guarantee is made that all or any of the individuals involved in generating the performance on behalf the other Unigestion entities will be involved in managing any client account on behalf of Unigestion U.K. More specific information regarding Unigestion UK is set forth herein where indicated and is available on request.

There is no guarantee that Unigestion will be successful in achieving any investment objectives. An investment strategy contains risks, including the risk of complete loss.

The risk management practices and methods described herein are for illustrative purposes only and are subject to modification.

Legal Entities Disseminating This Document

UNITED KINGDOM

This material is disseminated in the United Kingdom by Unigestion (UK) Ltd., which is authorized and regulated by the Financial Conduct Authority (“FCA”).

This information is intended only for professional clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients.

US

This material is disseminated in the U.S. by Unigestion (UK) Ltd., which is registered as an investment adviser with the U.S. Securities and Exchange Commission (“SEC”). This information is intended only for institutional clients and qualified purchasers as defined by the SEC and has therefore not been adapted to retail clients.

EU

This material is disseminated in the European Union by Unigestion Asset Management (France) SA which is authorized and regulated by the French “Autorité des Marchés Financiers” (“AMF”).

This information is intended only for professional clients and eligible counterparties, as defined in the MiFID directive and has therefore not been adapted to retail clients.

CANADA

This material is disseminated in Canada by Unigestion Asset Management (Canada) Inc. which is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (“OSC”).

This material may also be distributed by Unigestion SA which has an international advisor exemption in Quebec, Saskatchewan and Ontario. Unigestion SA’s assets are situated outside of Canada and, as such, there may be difficulty enforcing legal rights against it.

SWITZERLAND

This material is disseminated in Switzerland by Unigestion SA which is authorized and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”).

SINGAPORE

This material is disseminated in Singapore by Unigestion Asia Pte Ltd. which is regulated by the Monetary Authority of Singapore (“MAS”).

Document issued May 2020.