The Equity Bear Market Does Not Look To Be Over

With global equities now in a bear market1, many investors are wondering whether it is a good time to buy stocks. One’s investment horizon is critical in answering this question – equities will recover their losses eventually – but the current environment poses more downside risks than upside supports. Placing the current market in the context of previous bear markets, assessing equity valuations, and looking ahead to the likely path of the economy and monetary policy all suggest that equity markets are far from out of the woods.

(Let Me Be Your) Teddy Bear

What’s Next

Equities have not hit the depths of prior bear markets

The double-whammy of an inflation-induced monetary policy tightening followed by fears of a near-term recession have pushed most equity markets into bear market territory. Significant dispersion underneath the surface reflects this dynamic, with long duration/high growth stocks taking the brunt of the blows, while cyclicals have recently underperformed defensives. The key question many investors are contending with is how much further could markets fall, or, put another way, is it a good time to buy?

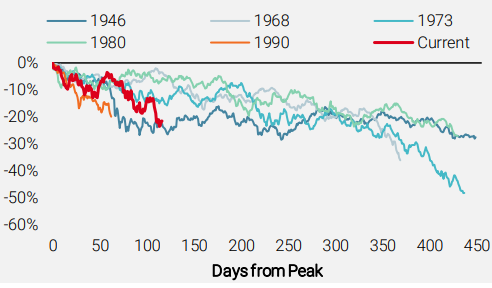

Not all bear markets are created equal, and there have been varying depths of drawdowns. The S&P 500 provides the most complete data on bear markets and their economic context, which helps to understand their drivers. Looking at S&P 500 bear markets back to 1835, we see that they have declined on average by -37% from their peaks, the shallowest being -20% (July-October 1990) and the deepest falling by -85% (September 1929-June 1932). Not surprisingly, bear markets accompanied by massive structural imbalances that were resolved by major recessions were the most acute (e.g., the Great Depression, the GFC). With financial balances healthy for both households and businesses, the good news is that a deep recession does not seem to be the likeliest scenario. The bad news is that even for other bear markets that are more akin to today’s context – monetary policy tightening triggering an economic slowdown and market sell-off – the market continued to move lower. Figure 1 charts the performance of the S&P 500 from the start of those bear markets that are relevant today as well as the current market action, revealing the severity of these “milder” bear markets. On average across these cases, the S&P 500 experienced a drawdown of -35% from its peak, leaving the current market still far off from the historical average.

Figure 1: Select S&P 500 Bear Markets

Source: Bloomberg, Unigestion, as of 23 June 2022

Beware of valuation traps when macro regimes shift

Naturally, equity valuations have dropped along with the market sell-off. The S&P 500 has seen its 12-month forward P/E ratio fall from 21.5 at the start of the year to 15.7. However, only part of this fall is due to prices, as 12-month forward earnings-per-share estimates have risen 7% over the same period. Thus far, analysts have yet to incorporate a significant slowdown – let alone a recession – into their estimates for the year ahead, and when they do, the current level of valuations will no longer look so attractive.

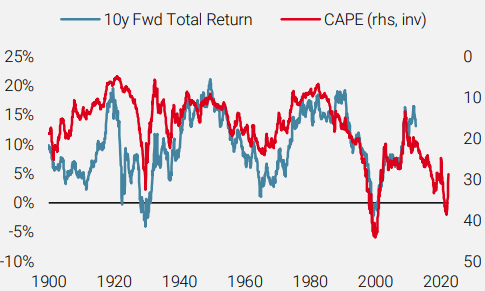

Another useful perspective to keep in mind is Robert Shiller’s cyclically-adjusted P/E ratio (CAPE), which covers the last ten years of earnings to remove cyclicality and provide a longer-term view on the expensiveness of equities. As Figure 2 shows, it has proven to be a fairly good guide to future equity returns through many different environments. At today’s levels, and despite the market correction, equity market total returns would still be expected to be in the low single digits over the next ten years.

Figure 2: Shiller’s P/E Ratio vs 10y S&P 500 Forward Returns

Source: Robert Shiller, Unigestion, as of 22 June 2022

Peak hawkishness has yet to materialise

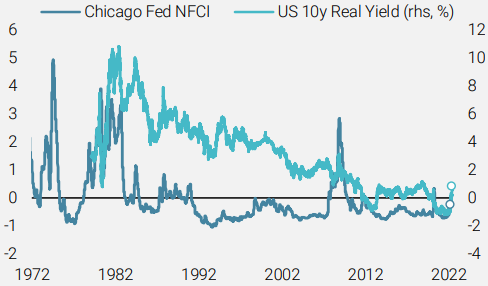

In our view, equity markets will not be out of the woods until central banks shift their rhetoric to a less hawkish stance. Unfortunately for many investors, such a pivot will likely not happen until after the economy has slowed down sufficiently to bring inflation on a sustainably downward path. In the US, despite higher short-term interest rates, the highest mortgage rates since the housing crisis, and a major correction in both bonds and equities, financial conditions have not dramatically tightened. As shown in Figure 3, the Chicago National Financial Conditions Index (NFCI) remains negative, pointing to still easy conditions. At the same time, the 10-year real yield has only moved slightly into positive territory. Despite the long-term negative trend in real yields, reflecting secular forces and lower US growth potential, the current level of real yields seems too low to achieve the slowdown the Fed is looking to engineer to fight inflation. For instance, the 10-year real yield remains below the 1.1% level seen in Q4 2018, when inflation was no concern at all for the Fed’s tightening plans.

Figure 3: US Financial Conditions

Source: Bloomberg, Unigestion, as of 22 June 2022. Real yield computed as spread between 10-year nominal yield and inflation expectations (10-year breakeven inflation from August 1998 to today and extended back to March 1979 based on University of Michigan 5-10 Year inflation expectations survey).

As financial conditions continue to tighten and flow through the economy, they will dent estimates for corporate earnings growth, adding further downward pressure on stock prices. If central banks, in particular the Fed, remain knee-deep in their fight against inflation, the environment will become toxic for equities. This does not preclude relief rallies, but with few supports outside of hedge funds’ positioning, the risk/reward for equities remains to the downside in our view.

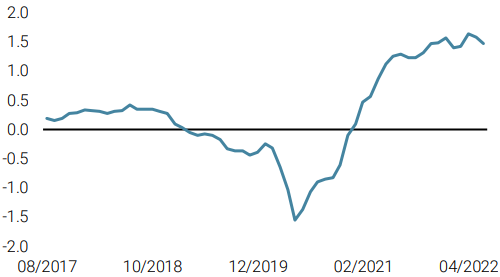

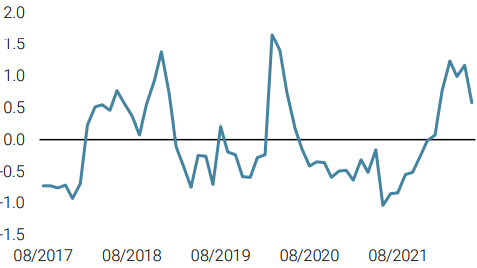

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster was steady and remains below potential. Changes were minor and offsetting across economies.

- Our World Inflation Nowcaster moved down slightly with further easing in inflationary pressures in China as well as the UK.

- Our Market Stress Nowcaster moved modestly lower last week, as volatilities retraced and spreads narrowed.

Sources: Unigestion, Bloomberg, as of 27 June 2022.

1A bear market is generally defined as a drop of at least 20% from the previous all-time high

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).