Markets interpreted the latest FOMC meeting as hawkish because 1) the dots rose significantly, with 13 out of 18 board members expecting a hike by 2023 and seven participants now expecting a hike by the end of next year; 2) this significant upward shift in rate projections was accompanied by an upward shift in inflation projections for this year, and 3) the dot dispersion across members widened sharply for 2023. In our view, despite these adjustments, monetary policy remains accommodative. Moreover, we expect the Fed to remain patient despite the upside surprises in GDP and inflation that we forecast for H2 2021.

Let The Music Play

What’s Next?

Market reaction driven by technicals, not fundamentals

Following the meeting, the market repriced the probability of an inflation overshoot in the coming years. The TIPS yield curve shifted higher and flattened, US front-end rates sold-off, growth-oriented assets declined and the USD strengthened. Interestingly, the flattening of the US curve boosted long duration growth stocks and Value underperformed, indicating a “reverse rotation”.

In our view, three key technical factors played a role in the market reaction to the Fed’s message:

- Unwinding: Most investors decided to reduce their risk following the rise in the dots for 2023, as illustrated by the increase in short interest in most equity and credit ETFs. This derisking triggered a large unwinding of winning positions such as the ‘US steepener’, ‘long value / short tech’ and ‘overweight equities / short bonds’ trades, supporting the reverse rotation within and across assets.

- Gamma positioning: Market makers were long gamma ahead of the meeting as a result of systematic overwriters selling expensive implied volatility relative to realised volatility over the preceding month. This position kept the S&P 500 index in a tight range and limited the adjustment in US equities.

- Deleveraging: CTA strategies were extremely short USD versus DM and EM currencies, and short duration. The need to partially cover these shorts following the adjustment of the Fed amplified the market reaction to the greenback and US Treasuries. As an illustration of this, the SG Trend index fell -4.2% in June.

Consequently, we see these reverse rotation movements as temporary, driven more by technical elements than fundamental ones. We therefore continue to expect significant outperformance of growth and real assets at the expense of defensive ones in H2. This bullish view is based on two key elements: 1) despite upward adjustment in the dot projections, the Fed remains dovish, and 2) the fiscal stance, which has rarely been as supportive as it is today in US and Europe, is much more important than liquidity injections for upside surprise in both activity and inflation, and for supporting growth and real assets.

The Fed remains dovish

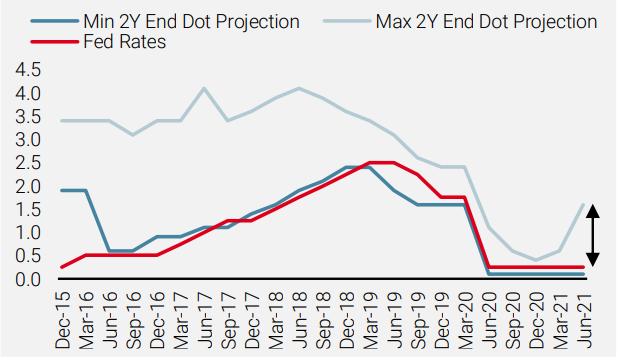

Despite the change in dot projections in the June meeting, the Fed’s stance remains largely dovish. Two elements confirm this bias. Firstly, our analysis of dot projections shows that for Fed rates to rise or taper, the board needs dovish members to converge toward hawkish ones on macroeconomic forecasts. Figure 1 compares minimum, maximum and median two-year forward dot projections with Fed rates. It shows that in the previous tightening cycle, between 2015 and 2018, the minimum rate projection, reflecting expectations from dovish members, had moved much more than the maximum, reflecting the hawkish members.

Figure 1: Historical Dot Projections of Next Two-year-end Rates vs Fed Rates

Source: Unigestion, Fed, as of 25 June 2021

This finding highlights the role and importance of dovish members for reaching a consensus to adjust monetary policy. As a reflection of this, since the implementation of dot projections and guidance, Fed rates have closely followed minimum dot projections, highlighting just how accommodative the Fed’s stance has been over the period.

The second element relates to the Fed’s clear overweight to unemployment rates at the expense of inflation in their communication. This stems partly from the Fed’s average inflation targeting policy but also from a biased risk reward analysis driven by dovish members who think that it is less costly to cap inflation pressures if they occur than to adopt a highly detrimental proactive strategy that carries the risk of a new recession by tightening too early or too strongly. As a result, in the coming months, the data to watch will not be inflation-related, such as production prices, wages or rent, but data reflecting the health and fluidity of the labour market. In terms of guidance, the hawkish signal would come from a clear downward shift in unemployment rate projections, not from a higher inflation forecast.

‘End of easy money’ is different from ‘End of easing’

Another factor that seems important to incorporate in order to categorise the monetary policy mode is the difference between the “end of easy money” that defines the start of a tightening cycle with the “end of easing” that marks the end of a rate cut cycle. In the first regime, the cost of borrowing increases and should rise in the future. In the second, this cost stops falling but should remain at a low level for some time. Historically, the “end of easy money” has led to a repricing of both inflation and growth premia that negatively affects most assets and can trigger a correlation shock if the shift was not well publicised, as in 2013 or even at the beginning of 2018. Conversely, the “end of easing” means that financial conditions remain favourable. We believe that the Fed communication reflects an “end of easing” mode, rather than a clear shift into an “end of easy money” regime.

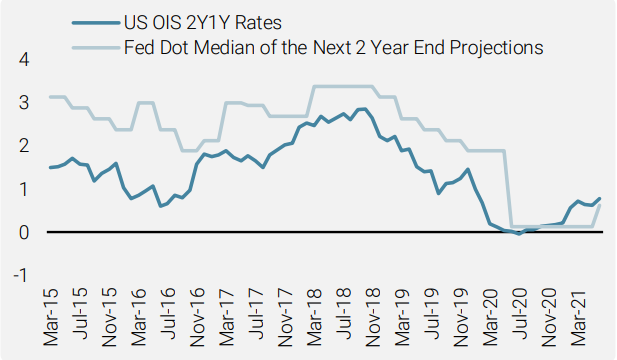

Figure 2: Market Pricing vs Fed Dot Projections

Source: Unigestion, Fed, Bloomberg, as of 25 June 2021

This is highlighted by the comparison between Fed dot projections for the end of the next two years and the rate projections implied in market pricing represented by the forward OIS USD 1Y rate in 2023, illustrated in Figure 2. As shown in the chart and despite adjustments done for 2023 dots, the short-term interest rates forecasted by Fed members remain lower than the one reflecting market views.

The ‘reflectivity game’

Last week’s FOMC meeting can be seen as a hawkish surprise, but it does not change our market outlook. Our proprietary Nowcasters for Growth and Inflation remain at high levels supported by the Expectations and Housing components for global growth and by Input Prices and Supply Side for inflation pressures. In our view, the easing of fiscal rules in the US and Europe, which will lead to a massive investment in sustainable public and private projects and infrastructure, is the pivot of our “macro regime shift” scenario. Consequently, GDP and inflation are likely to continue to exceed both Fed and market expectations, driving bond yields higher, supporting commodities and real assets, and justifying high expectations for future earnings growth. In this positive environment, the timing of the Fed’s adjustment is crucial.

Not unlike George Soros’s famous concept of “Reflexivity”, this Fed-induced “reflectivity game” could be summarised as follows: the later the rate normalisation, the higher the risk of inflation overshoot and the greater the tightening. Conversely, the sooner, the lower and the smaller the need for normalisation. In this framework where any phase in the sequence is conditional on the previous one, any step in any direction by the Fed will require risk premia adjustments and vice versa: any overshoot in market forecast and corporate/household behaviour could trigger an unexpected shift from the Fed. We expect a first rate hike in 2022 and continue to expect the tapering process to start next year. However, we don’t think this will detract from our bullish view on growth and real assets because of the strength of the global economy and the gradual and well publicised shift in financial conditions.

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster was steady at elevated levels.

- Our World Inflation Nowcaster moved up slightly on the back of stronger inflationary pressures in the US.

- Our Market Stress Nowcaster remained steady at low levels.

Sources: Unigestion, Bloomberg, as of 25 June 2021

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).