The Narrow Path To A Soft Landing

Fed governors have made clear that reining in inflation is their primary goal for monetary policy today. As they have no tools to address the supply side of prices, they can only act on the demand side by raising the cost of money to discourage spending. Their challenge will be to do so while avoiding a hard landing: can they reduce demand sufficiently to alter inflation’s course without triggering a recession? Wage inflation plays a critical role in their calculus, as its current rate of 5.5% and upward trajectory make a return to the 2% inflation target over the next couple of years difficult to achieve. Estimating the rate of economic growth needed to ease wage inflation sufficiently and assessing this estimate against current macro conditions suggests that the Fed may have a path to make the soft landing. However, it is an extremely narrow path fraught with uncertainty, and the risk of a recession remains paramount in our minds.

Paper Planes

What’s Next

Nominal wages gain steam while real wages lag

As we have previously discussed, the forward path for inflation will likely be determined by the reaction of wages to mounting prices in the broader economy. A price/wage spiral is a death knell for an economy, and the Fed’s aggressive pivot precisely aims to avoid that situation. The consolidation and modest retracement seen in US inflation breakeven rates is a positive sign for their credibility. However, nominal wages continue to rise strongly, up 5.5% y/y in April, putting further upward pressure on inflation. As Figure 1 shows, despite the strongest nominal wage growth in over a decade, realised inflation is outstripping wages and real wages continue to contract.

Figure 1: US Year-Over-Year Wage Growth (%)

Source: Bloomberg, Unigestion, as of 18 May 2022

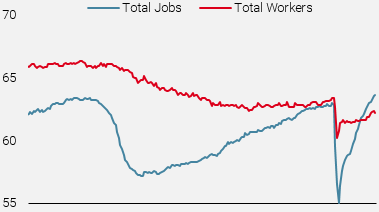

The unemployment rate is a useful barometer of the tightness in labour markets, and its current reading of 3.6% is back to pre-pandemic levels and among the lowest post-World War II. Another useful perspective to assess labour markets is comparing total jobs (employed persons plus job openings) to total workers (labour force participation), shown in Figure 2.

Figure 2: US Jobs and Workers (% of working age population)

Source: Bloomberg, Unigestion, as of 18 May 2022

This perspective clearly reveals why labour continues to have strong pricing power: whereas the total number of jobs is back to pre-pandemic levels, the total number of workers remains depressed. As long as this imbalance continues, wage growth, at least in nominal terms, will remain strong. Labour supply could certainly recover further, given that pandemic-related unemployment support has been largely eliminated, but continuing Covid outbreaks (and resulting child care constraints) will limit this recovery. Meanwhile, job openings are at an extreme, up nearly 4.5m compared to pre-pandemic levels. This channel provides an effective path for the Fed to slow inflation: raise the cost of capital sufficiently so as to encourage firms to defer growth plans, thereby closing the jobs-workers gap by reducing the number of job openings and avoiding a large increase in the unemployment rate. Chairman Powell suggested during the May press conference that the Fed was thinking similarly:

Job creation has been… very, very strong, particularly for this stage of the economy. And so we think with fiscal policy less supportive with monetary policy, less supportive we think that job creation will slow as well.

Closing the jobs-workers gap

Currently, the gap between total jobs and workers is about 1.5% of the working age population, or about 3.8m people. Closing this gap will be necessary for wage growth to fall toward more acceptable levels and will likely have to come predominantly from fewer job openings. Historically, for the job openings rate to decline by 1.5% meant growth falling to about 1% below potential, consistent with the notion that growth needs to be below trend in order to see a cooling of the labour market. Given a potential growth rate of 2% in real terms, this gives the Fed a path – albeit a very narrow one – by which they could close the job-workers gap and rein in wage inflation without triggering a recession.

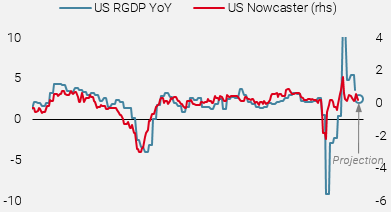

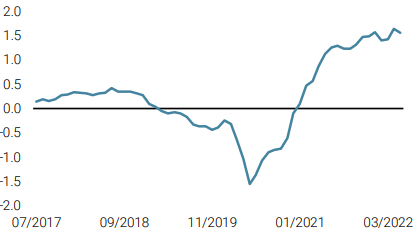

Indeed, monetary policy actions and Fed rhetoric (as well as fiscal policy) have already slowed down the US economy. We can see this from two perspectives: First, our US Growth Nowcaster, which assesses household consumption, business investment, housing, and financing conditions, now shows the US economy already growing near its potential rate. Figure 3 shows the evolution of this indicator against US growth, which are 75% correlated on a coincident basis. We also plot a projection for this quarter’s growth based on the current reading of the Nowcaster: 2.4% y/y, down from the official 3.6% print for Q1 2022. Given its recent trend, it would not be surprising to see the US Nowcaster call for growth at potential within a few weeks.

Figure 3: US Growth vs US Nowcaster

Source: Bloomberg, Unigestion, as of 19 May 2022

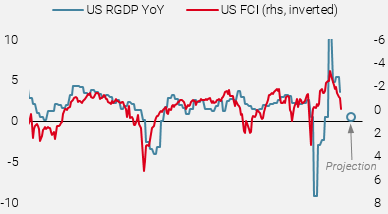

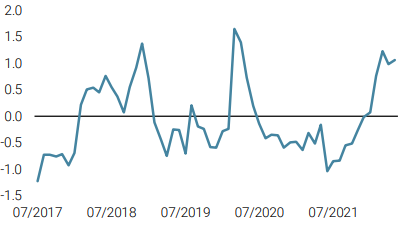

A second perspective is also helpful to gauge the impact of Fed policy and actions, which primarily affect financing conditions. Focusing on solely these conditions in the US – interest rates, corporate spreads, equity prices, and the trade-weighted exchange rate – we can see they have tightened significantly over the last year, as investors increasingly priced in an aggressive Fed. Figure 4 charts the US Financial Conditions Index (FCI) against US growth. Unlike our Nowcaster, which is a coincident indicator, we can readily see that the FCI is a leading indicator about six months ahead of growth. Indeed, changes in the FCI are about 50% correlated to US growth two quarters later. Figure 4 also provides a projection of the level of US growth at the end of the year given the recent changes in the FCI: it calls for US growth falling to about 0.6%.

Figure 4: US Growth vs US Financial Conditions Index

Source: Bloomberg, Unigestion, as of 19 May 2022

These projections are imperfect and do not fully account for the knock-on impacts of monetary policy, nor the peculiar economic circumstances of a post-pandemic world. However, both suggest that the current flow-through of policy action and rhetoric will likely slow US growth significantly to levels within the narrow band the Fed is trying to land: below potential growth but still positive, so as to rein in inflation without triggering a recession. The risks of further hawkishness are tilted to the downside, as this would likely push the US economy into recession. Given that context, we remain cautiously positioned in our dynamic allocation, with low exposures to most assets and a net long US dollar bias.

Unigestion Nowcasting

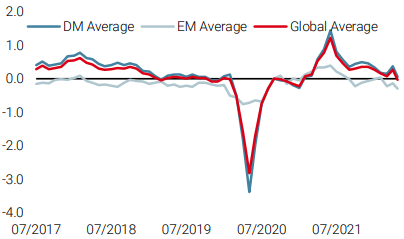

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster fell below zero, reflecting global growth below potential. The drop was driven by worsening conditions in the US and China.

- Our World Inflation Nowcaster was largely unchanged, with most countries continuing to see elevated inflationary pressures.

- Our Market Stress Nowcaster was steady, as underlying components remained elevated.

Sources: Unigestion, Bloomberg, as of 23 May 2022

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).