This year has been extraordinary and it is not over yet. To some extent, October feels like February all over again as the solid growth picture could once more be derailed by lockdown measures. For the moment, this is a European situation but things could spread to the US, and that would be a game changer. The odds of a “W” growth scenario have just increased, although it remains just a risk for now. For that reason, our allocation is becoming less positive now, as we are increasingly concerned about the consequences of potential lockdowns on future growth prospects.

Fear of the Dark

What’s Next?

Growth could be at risk in the case of a second wave

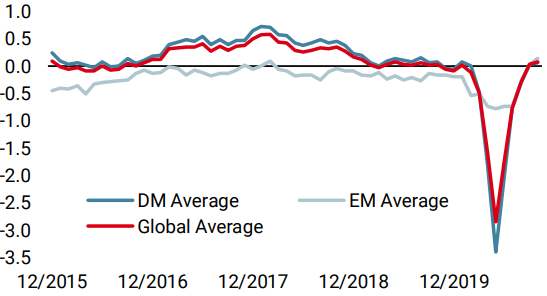

Is it February all over again? Growth is strong and the recovery is underway as a result of the stimulation and the reopening of a majority of economies: that must remind investors of the February situation. Back then, growth was also recovering from the 2018 slowdown and data readings were also pointing to an improving situation. Our Growth Nowcaster was showing 52% of improving data, with an indicator at around -0.1. These levels meant that world GDP was growing at around its potential, and marginally improving. Now, we are seeing 57% of improving data and an indicator around 0.1: from these numbers, the growth situation looks even better today. A generalised lockdown period, like the one we experienced in Q1, would negatively impact growth and would put markets are risk. What are we looking at? And where do we stand?.

Q4 weaker than expected as we lack ammunition

To some extent, risks could be higher now than they were in Q1. First, even if our indicators are showing an economic recovery, growth in 2020 is negative when it was largely positive in 2019. Exiting an expansionary period is clearly not the same thing as returning to a recession. A “W” scenario would weigh heavily on consumption and eventually on earnings and equities. Also, central banks have delivered most of what they can, leaving a smaller room to maneuver should a two or three-week lockdown be necessary again. Rates, both shorter and longer term ones, are as low as possible, while the size of the Fed’s balance sheet is now 34% of US GDP and the ECB’s, 59%. Also, governments – especially European governments – have stretched their deficit limits to levels rarely seen, if not ever seen before. How much more can they provide us with? Overall, the risk of a “W” scenario is increasing with less ammunition to shelter our economies and markets from it. For now, the rise in cases is limited to Europe, but should this wave hit the US, we expect markets to react a lot more violently. Overall, this implies lower Q4 GDP growth readings than expected. These readings would have been lower than Q3’s, but now we expect a deterioration in the economist and analyst forecasts should a genuine lockdown take place.

For now, it is still not February all over again

Having said that, we see three positive differences this time that should bring some balance to the negative picture we just painted.

First, we have complemented our Nowcasters with Newscasters, indicators that look at the news flow on growth rather than economic data. These indicators showed a bearish signal on 28 February this year, while pointing to an improving situation at the end of April. For now, these indicators are still showing a very low recession level, in spite of the rising number of COVID cases. We are keeping an eye on their readings as we believe they should give a clear indication regarding a potentially deteriorating growth situation.

Second, beyond our Newscasters, we are scrutinising signposts that we have learned to watch since the first wave hit our economies. The service vs. industry sector situation is one, the geographic evolution of the shocks is another. Higher frequency macro indicators such as surprise indices are also elements that we think can help us to better understand the economic impact of curfews and potential new waves of lockdowns. For now, we do not see much deterioration there but we do anticipate growth-unfriendly restrictions in the coming weeks that markets will see as a threat to equity valuations.

Finally, authorities have learned and improved their handling of the situation. We now have clear metrics coming alongside triggers as well as a broad spectrum of policy support measures that investors are unlikely to overlook: one of markets’ biggest enemies this year has been uncertainty, and these measures have eliminated a portion of it. Finally, the medical supplies available have nothing in common to what was available in February-March. We have learned to better handle the pandemic while waiting for a vaccine.

This combination of elements – so far – with the lower lethality of this second wave will probably limit the underperformance of growth-related assets, and their influence on the performance of our dynamic allocation. Still, we think the current increase in cases and fatalities is a threat to growth that legitimates a reduction of our positive view on equities. It should also affect market sentiment.

Sentiment is no longer a tail wind

Sentiment has made a strong recovery since its bottom in March. The rapidity of its U-turn when entering the crisis prompted our Market Stress Nowcaster to cut a portion of growth assets. The VIX exploded back then, moving from 14% to 80% in no time. Currently, the VIX is slightly below 30%: a rapid increase is necessary for our Market Stress Nowcaster to pick up on spikes of risk aversion, but it is less likely from these higher levels. Similarly, many quant strategies relying on volatility deleveraged their positions very quickly as volatility increased rapidly in February. This time would be different, as volatility has remained elevated since then, rendering their positioning less aggressive.

Beyond volatility, the positioning of investors is also essential to monitor: hot money and, more broadly, institutional money have been increasing their positioning in equities, from very low levels in March to more neutral positions now. Retail investors are also building up their positions. The AAII investor survey recently pointed to this ramp-up in bullishness. But this more positive attitude towards risk comes with a large demand for hedging: volatility indices are high for equities, while implied volatility levels are largely skewed. On one hand, investors are more bullish, but on the other they are also a lot more prepared for market volatility. Close monitoring of the balance of positioning and hedging demand is essential here.

Valuations are high now

Finally, the last element in this investment puzzle is valuations. In mid-February, in the midst of the recovery from 2018, growth-asset valuations were slightly expensive. Today, our valuation metrics are not capturing such an expensiveness signal: as we have explained in previous editions, lower rates mean higher structural price earnings ratios, and today is not 2001. More bottom-up measures show how credit spreads look priced to perfection, while US stocks look expensive for solid reasons while being vulnerable to profit-taking and market stress periods.

Less positive than before

Our dynamic asset allocation is now less positive than last week, as we see a deterioration in the risk/return balance of growth assets. This is due to the potential stress coming with the US elections and the resulting macro deterioration from the curfews and renewed lockdowns, while sentiment and valuations are not supportive. This fear of the dark could weigh on markets more than expected and we are progressively getting prepared for it. Part of this preparation is seeking convexity in currency markets, as we see the reversal of extreme short USD positioning as an opportunity: in case of a collapse in equities, the rebound in the USD could be stronger than what many are expecting. For that reason, our dynamic allocation now incorporates a long USD position against currencies such as AUD, TWD and NOK.

Unigestion Nowcasting

World Growth Nowcaster

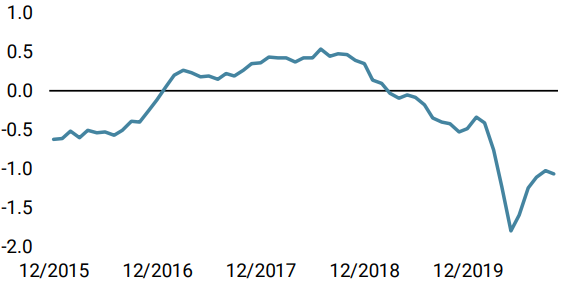

World Inflation Nowcaster

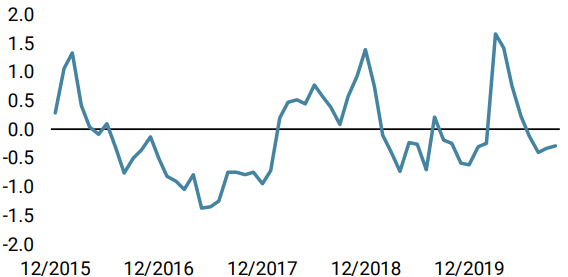

Market Stress Nowcaster

Weekly Change

- Our World Growth Nowcaster decreased last week, as US data drove the indicator lower.

- Our World Inflation Nowcaster increased slightly and broadly.

- Last week, our Market Stress Nowcaster did not move much as volatility evolved within a range.

Sources: Unigestion. Bloomberg, as of 26 October 2020.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore (MAS). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).