The biggest challenge to navigating the current crisis is finding the right balance between news coming from health and humanitarian concerns, macro dynamics and financial liquidity. Over the last weeks, we have been communicating a lot about our negative view on the economy. Despite macro data coming in significantly below very low consensus expectations, equity markets have rebounded more than 25% off their lows. When stock markets rally on bad news, investors often lose a sense of reality. Currently, overly bearish sentiment, improving virus-related data, some optimism about reopening the economy and backstops from both the Fed and governments seem to be the main drivers of the brisk recovery in financial markets. Phrases that we have heard every day for years disappeared over the last few weeks, but FOMO (fear of missing out) and TINA (there is no alternative) are back in investors’ minds. Fear and greed drive prices more than fundamentals in the short term.The Stock Market Is Not the Economy

Whatever It Takes

The S&P 500 index just experienced the quickest meltdown in history, losing 33.9% in 21 trading sessions. All the leverage that had been built up during the longest expansion ever fed into a vicious and self-perpetuating cycle of volatility, liquidity and “risk-based” forced selling. During these uncertain times, investors are looking for maps to try to match the current situation to an historical crisis. Within a short time frame, the historical comparison went from 9/11, to the GFC and finally to the greatest of all market shocks, the Great Depression. However, looking at the historical data, the Great Depression offers no real comparison. During that time, construction of residential real estate fell by 82%, industrial production dropped 52% and deflationary pressures led to prices falling by 33%. Additionally, its duration (number of quarters) was substantially longer than what we expect for this crisis. President Hoover refused to offer the help of the federal government, putting his main priorities in balancing the budget. The context couldn’t be any different. Today, budget deficits and debt levels do not matter, and central banks are stepping in harder and faster than any previous crisis to backstop funding markets and inject liquidity via repos, swap lines and QE programs. The Fed’s current asset purchase programme has eclipsed every other QE programme in notional terms in a span of less than four weeks. The life-or-death urgency of the situation has sparked an unprecedented monetary and fiscal response in terms of size, force and speed – necessity is the mother of invention. There is little doubt about the ability of governments and central banks to stabilise markets in the short run with their “whatever it takes” approach. However, we remain convinced that the rescue packages and stimulus are not enough to stop the economy from falling into a sharp recession. After the GFC, favourable capital market conditions and the hunt for yield led to a build-up of leverage on the premise that nothing bad would happen. By suppressing volatility and adding fiscal stimulus, these organisations have created a system that is very vulnerable to external shocks. Or said differently: they suppressed volatility, but they increased financial market fragility. COVID-19 unmasked an essential weakness in global finance, created by ten years of artificially cheap credit. And the only way out is to implement even bigger kitchen-sink policy actions, extending a lifeline to almost everyone looking for help. Ideas like helicopter money and modern monetary theory were ridiculed a few months ago, but mainlining liquidity directly into the veins of the global economy will be much more effective at boosting GDP than QE, which has largely injected liquidity only into the veins of the financial markets. Markets got caught totally off guard by an external shock that happened at a time when sentiment was very bullish, systematic positioning crowded and the confidence in central banks very high. After the massive meltdown, which was to a large extent technically driven, the market is now focused on the massive support from the Fed, which is clearly determined to underwrite most risk assets. With its latest action, the Fed has reached a new level of moral hazard – nationalising excessive risk taking. Central banks act as a backstop for government, corporate and municipal bonds, and a move lower in spreads also brought a sharp decline in fixed income volatility. The sharp decline in the volatility of US Treasuries not only reflects lower realised volatilty, but also the potential for the Fed to implement some sort of yield curve control. But if all these actions are not enough, will the Fed start buying the ultimate risk asset: stocks? In the short run, fighting the Fed is a losing proposition. The recent upswing might end like the bear market rally that started in October 2008 after TARP was passed, and which fully reversed into the market low of March 2009 due to the catastrophic collapse in economic and earnings data that followed. We continue to fear that the deterioration in macro data and earnings is not fully reflected in broad equity valuations. An earnings per share fall of “only” 13% year-on-year, would bring the S&P 500 index price-to-earnings multiple back to the levels last seen at the market peak in February 2020. Another headwind for equities is that the biggest buyer of the last decade, corporates, will be much less equity-friendly once their focus switches to ensuring their credit ratings. The recent moves in credit spreads wwere even more incredible than any other risk asset. Within three weeks, the focus moved from potential defaults of leveraged entities, rating downgrades, margin calls and forced selling to almost exclusively front-running Fed actions. We fear that, at some point, spread levels will need to face the economic reality of a real credit cycle. Valuations for risky assets might not matter in the short term, but it matters greatly on a 5-10 year time frame. The most difficult task is to strike the appropriate balance between offence and defence. Currently, sentiment, technicals and politics are calling for a short-term offencive stance whereas our fundamental view on the macro economy and earnings demands a medium-term defensive positioning. We have faith that after this meltup, driven by a fear of missing out and the belief that “there is really no alternative anymore” after the Fed rate cuts, markets will focus again on the real economy. Despite all the policy support and the positive health-related news, we believe that most investors are underestimating the consequences of the COVID-19 recession and its impact on earnings in a highly leveraged financial environment. Therefore, our portfolio is tilted defensively according to our core macro scenario, but we have increased risk exposures via assets that are supported by central banks to participate in the short-term positive momentum.What’s Next?

Help for markets vs the economy

There is no limit

Valuations remain expensive

Offence vs defence

Unigestion Nowcasting

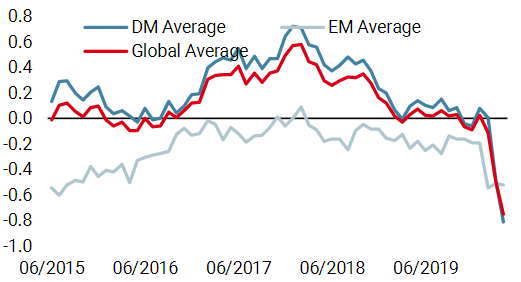

World Growth Nowcaster

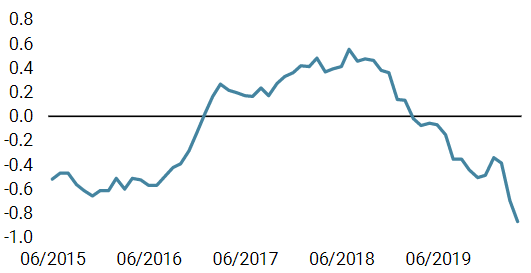

World Inflation Nowcaster

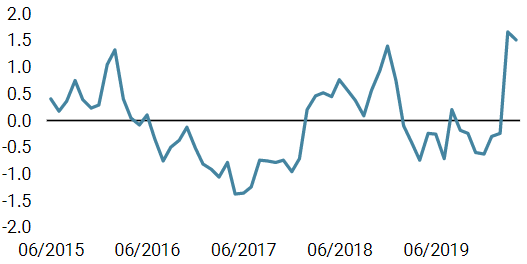

Market Stress Nowcaster

Weekly Change

- Our world Growth Nowcaster decreased again last week. This week’s sharpest decline is for the US and Canada where data was particularly poor. According to our indicators, the risk of a world recession is currently very high.

- Our world Inflation Nowcaster also fell, with the US and Canada again showing the largest decline.

- Our Market Stress Nowcaster remains elevated but retreated marginally last week as credit spreads narrowed and volatility declined.

Sources: Unigestion. Bloomberg, as of 14 April 2020.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore (MAS). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).