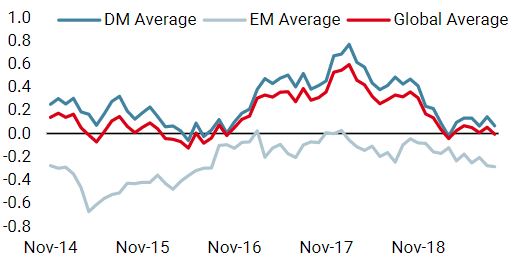

Markets have been hooked on central banks and their very accommodative monetary policies for almost a decade now. What had been a vital antidote to one of the worst financial crises in history has become a hard drug on which most investors have got high and highly dependent. We are seven years on from Mario Draghi’s “whatever it takes” speech and the latest ECB meeting proved that he was ready to do so, even if it was with very little consensus. Currently, the trillion dollar question is whether central bank action is necessary and whether additional stimulus will be successful in tackling recessionary and, more importantly, deflationary forces. At this late stage in the economic cycle, ammunition seems scarce and the market reaction following the ECB announcement could indicate that “the world is not enough”. The reason behind central banks’ headache is not risk of recession (yet?) but undershooting inflation, which in turn could lead to damaging deflation. In most speeches, policy makers reckon that economic growth has been downward sloping from early 2018’s above-potential peak and that the balance of risks are tilted to the downside. Yet, they remain confident that recession is not near (in spite of yield curve pricing), particularly the Fed. Conversely, the lack of inflation is the focal point. Is it normal to have so little price pressure when growth has been strong for such a prolonged period and the influx of money mostly unlimited? There are secular forces at work weighing on inflation globally, like demographics (the effects of aging on consumption habits), automation (putting pressure on wages) and digitalisation. There are also cyclical elements missing this time around: the commodity cycle and investment. Usually, after sustained periods of growth, commodity prices reach their peak on the back of supply and demand imbalances, and negatively affect both consumers and companies suffering from higher input costs. Our proprietary Inflation Nowcaster not only indicates a deterioration in inflation conditions, it also indicates that not a single inflation component is showing signs of strength: from wages to input prices, imported and expected inflation, all are low and going lower. And it is happening all across the developed and emerging world. As a result, it provides central banks with breathing space and allows them to ease and pump as much money as possible into the system, helping the world to prolong growth and revive inflation. Expectations have climaxed and it looks like there can only be disappointment ahead. Looking at interest rates pricing, a total of 250bps cuts are currently priced in the G10 12 months ahead, with at least one to two cuts expected in every country, apart from the Nordics. In the US, investors are still factoring in three cuts 12 months ahead (from four recently). The market reaction on the ECB meeting highlights the shape and form of disappointment. Sentiment reversal hit bonds hard, sending bund yields up 10bps intraday to close the day higher, on the very day Draghi announced a rate cut and revived asset purchases. Positioning in hedging assets, especially bonds, reached extreme levels, and the fact that the decision was reached with a low consensus outweighed any satisfaction from the promise of fresh accommodation. There are now two possible outcomes that could arise from the mismatch in perception between the patients and the doctors. Sentiment could lift as macro conditions remain around potential and easing remains in place (our scenario); or a lack of confidence in the ability of policy makers to avoid the end of the cycle could prompt a correction in the price of financial assets. Regarding asset prices, valuations are rich across the investment spectrum, with hedging assets leading. Government bond yields have plummeted to historical lows, the Japanese yen has appreciated back to February 2018 high stress levels and implied volatility remains expensive, in spite of rising risk appetite. The question now is whether to think in “normative” or “pragmatic” terms when assessing if this year’s market rally is near the end and if we are getting closer to a valuation reversal. It usually needs a catalyst to trigger valuation squeezes and large-scale sector/asset rotation, and central bank surprises can be a game changer in that respect. It might be too early to call for a sell-off in overcrowded/rich positions. Indeed, the truth is that central banks have created buckets of expensiveness that some would even call asset bubbles. It is crucial to be mindful of this factor now that incremental action from policy makers (on top of what is already in prices) remains to be seen. Investors will start paying attention to the level of asymmetry and dry powder left in every asset class, and the most expensive ones could suffer heavy losses to benefit once overlooked, cheaper, out-of-favour opportunities. For now, monetary support is alive and well, and expensive risk premia could remain so while it lasts.“The World Is Not Enough” – Garbage, 1999

What’s Next?

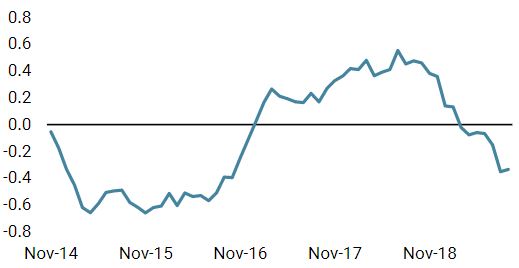

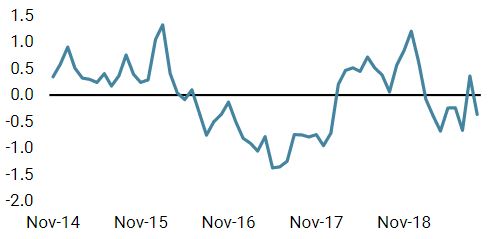

Macro: The First Negative Inflation Surprise Ever

Sentiment: When You Reach for the Moon, the World is Not Enough

Valuation: Expensive for Longer

Asset Allocation: Risk ON, but Vigilant

The biggest fear for asset allocators is correlation distortions, if not shocks. Diversified portfolios rely on historical interaction between assets, which have been largely manipulated by quantitative easing. So far, it has been a supportive driver to most assets but mean reversion in correlations are to be anticipated, even temporarily. At the moment, hedging assets seem the most vulnerable to the combination of resilience in economic growth, extreme positioning and tense valuations. For that reason, we have reduced substantially our exposure to the asset class and have reallocated to growth-related assets, credit first. For the same reasons, corporate spreads will be supported by the quest for yield and carry, the lack of recession and positive developments in sentiment and appetite for risk. More generally, the current environment is benign for risky assets, and we have increased exposure to equities and volatility (on the short side). Our attention is geared toward assessing if the disappointment on the ECB front will follow from other central banks, which could indicate that the world will no longer be enough to keep investor optimism afloat, prompting us to trim market exposure globally.

The World Is Not Enough

Our medium-term view is currently more constructive, as we are still overweight growth assets and underweight real assets. We are also complementing our exposures with options to protect the portfolio in the case of equity drawdowns. In September so far, the Uni-Global – Cross Asset Navigator fund has gained 0.8% versus 3.4% for the MSCI AC World Index and -1.6% for the Barclays Global Aggregate (USD hedged). Year-to-date, the Uni-Global – Cross Asset Navigator has returned 10.0% versus 17.6% for the MSCI AC World index, while the Barclays Global Aggregate (USD hedged) index is up 7.6%.Strategy Behaviour

Performance Review

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Our world Growth Nowcaster decreased last week as most countries on our radar showed softer macro data.

- Our world Inflation Nowcaster stabilised last week, after a long period of decline.

- Market stress decreased last week, as volatility and credit spreads decreased.

Sources: Unigestion. Bloomberg, as of 16 September 2019.

Navigator Fund Performance

| Performance, net of fees | 2018 | 2017 | 2016 | 2015 |

| Navigator (inception 15 December 2014) | -3.6% | 10.6% | 4.4% | -2.2% |

Past performance is no guide to the future, the value of investments can fall as well as rise, there is no guarantee that your initial investment will be returned.

Important Information

Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed by recipients to any other person. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in the investment vehicles to which it refers. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Please contact your professional adviser/consultant before making an investment decision.

Where possible we aim to disclose the material risks pertinent to this document, and as such these should be noted on the individual document pages. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors.

To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of this information. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Uni-Global – Cross Asset Navigator is a compartment of the Luxembourg Uni-Global SICAV Part I, UCITS IV compliant. This compartment is currently authorised for distribution in Austria, Belgium, Denmark, Finland, France, Germany, Ireland, Italy, Luxembourg, Netherlands, Norway, Spain, UK, Sweden, and Switzerland. In Italy, this compartment can be offered only to qualified investors within the meaning of art.100 D. Leg. 58/1998. Its shares may not be offered or distributed in any country where such offer or distribution would be prohibited by law.

No prospectus has been filed with a Canadian securities regulatory authority to qualify the distribution of units of these funds and no such authority has expressed an opinion about these securities. Accordingly, their units may not be offered or distributed in Canada except to permitted clients who benefit from an exemption from the requirement to deliver a prospectus under securities legislation and where such offer or distribution would be prohibited by law. All investors must obtain and carefully read the applicable offering memorandum which contains additional information needed to evaluate the potential investment and provides important disclosures regarding risks, fees and expenses.

All investors must obtain and carefully read the prospectus which contains additional information needed to evaluate the potential investment and provides important disclosures regarding risks, fees and expenses. Unless otherwise stated performance is shown net of fees in USD and does not include the commission and fees charged at the time of subscribing for or redeeming shares.

Unigestion UK, which is authorised and regulated by the UK Financial Conduct Authority, has issued this document. Unigestion SA authorised and regulated by the Swiss FINMA. Unigestion Asset Management (France) S.A. authorised and regulated by the French Autorité des Marchés Financiers. Unigestion Asia Pte Limited authorised and regulated by the Monetary Authority of Singapore. Performance source: Unigestion, Bloomberg, Morningstar. Performance is shown on an annualised basis unless otherwise stated and is based on Uni Global – Cross Asset Navigator RA-USD net of fees with data from 15 December 2014 to 16 September 2019.