Tightening Expectations Too Aggressive as Inflation Likely to Cool Next Year

A new coronavirus variant combined with hawkish comments from Fed Chairman Powell to the Senate Banking Committee soured market sentiment at the end of November. The world knows little about the omicron variant at this time, and it will be a few more weeks until we understand its contagiousness, virulence, and resistance to existing vaccines. Uncertainty is never good for markets, and in the meantime, the virus will spread and likely trigger restrictions and headline risk. The outlook for monetary policy seems more certain for markets, with Powell apparently confirming market pricing of sustained rate hikes next year. However, we see the macroeconomic context in 2022 as challenging for a major hiking cycle to start, putting us at odds with current market expectations.

Gone Till November

What’s Next?

Omicron and Powell: A double whammy

Growth and inflation premia repriced starkly in November, especially at the end of the month with news on the omicron variant and Chairman Powell making the case to lawmakers that the Fed was ready to tame prices. Global equities were broadly lower, with the MSCI AC World index falling -2.4%, but emerging markets suffered more, as they struggled throughout the month and finished down -4.1%. Dispersion was significant: the MSCI World Tech sector was up 2.6% on the month while the Energy sector was down -6.9%. Bonds rallied, with the yield on US 10-year T-notes down -11bps to 1.45% and the Barclays Global Aggregate up 0.7%. Real assets suffered with breakeven inflation rates falling and the Bloomberg Energy index down -17%. The US dollar rose 1% on a trade-weighted basis and the JP Morgan EM Currency index fell -4%. A broadly risk-on month transformed into risk-off in the span of just a few days.

Market expectations are clear: at least two hikes next year

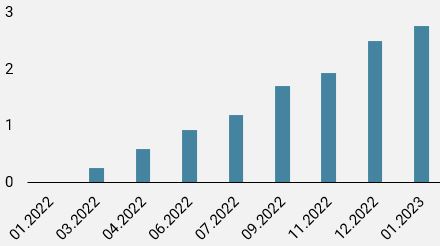

While uncertainty about the omicron variant makes it challenging to form strong views following the volatile end of month, the outlook for monetary policy seems clearer to us. Powell’s hawkish comments to members of Congress, which seem to have been prepared ahead of time, look aligned with market expectations, pricing interest rate lift-off for the middle of next year. As Figure 1 shows, the first hike is essentially completely priced in for the June meeting and the market expects somewhere between two to three hikes for 2022. While Fed members’ expectations could change, the market is pricing significantly tighter policy than the median projection of one hike from the September meeting.

Figure 1: Number of Hikes/Cuts Priced for Fed Meetings

Source: Bloomberg, Unigestion, as of 02.12.2021.

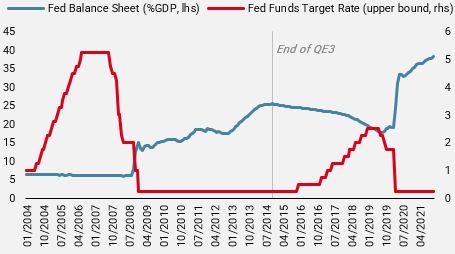

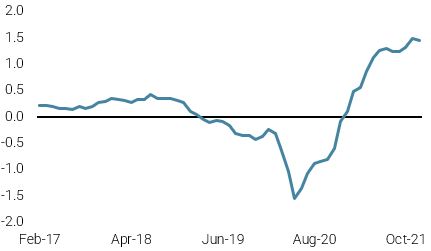

It is helpful to put such a tightening cycle in the all-too-recent context of asset purchase tapering and rate hikes. As Figure 2 shows, the Fed waited a year after ending quantitative easing (QE3) before its first rate hike at the December 2015 meeting. It then waited another year before the second hike. Of course, the macro picture in 2015-2016 was markedly different from today, in particular, inflation pressures were muted and the job market was quite robust. However, the takeaway from this historical context is that the Fed has largely shown cautiousness over the last few years, letting shifts in policy flow through and assessing the outcome before engaging further. Put another way, they tend to “tap the brakes” rather than slam their foot down.

Figure 2: Fed Balance Sheet and Target Rate

Source: Bloomberg, Unigestion, as of 01.12.2021

So how concerning is inflation?

We have been communicating since the end of last year that inflation would be a key macro force in 2021 and drive market returns, as the post-crisis demand recovery would meet supply and labour constraints. We reiterated that it would prove more durable than central bankers expected and not simply the result of base effects. Heading into the next year, however, we believe inflationary forces will peak through a combination of slower (though still healthy) demand and a gradual . This does not necessarily mean inflation will fall back to the 2% target, but rather that it will ease considerably, thereby relieving pressure on the Fed to tighten too fast.

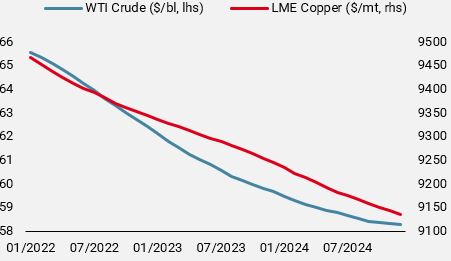

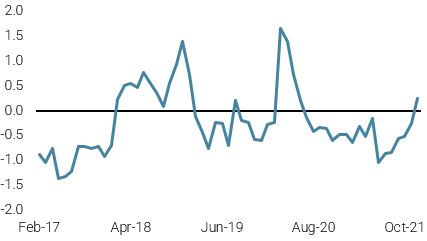

Savings rates have declined significantly, so we do not see a massive source of pent-up demand. At the same time, new capacity is being brought online and supply issues are expected to be in the early part of next year. Moreover, as we mentioned last week, food, energy and other commodities are responsible for over half of headline inflation this year while less volatile components such as shelter and medical care grew at an elevated but more sustainable pace and only contributed 1.9% to the 6.2% y/y rise in the CPI. Absent an extraordinary surge in these core components, food and energy prices would need to see another upswing like the one in 2021 to keep inflation at these levels, implying oil trading at over 125 USD/bl. Indeed, market pricing suggests that commodity prices are set to fall in 2022, as shown in Figure 3, which aligns with lower demand and increased supply expected next year.

Figure 3: Commodity Futures Curve Pricing

Source: Bloomberg, Unigestion as of 01.12.2021.

Positive in the medium-term but cautious short-term

With the market having absorbed two, possibly three, rate hikes next year, the question for investors is whether they expect more or fewer hikes. We are squarely in the camp of fewer: we expect the inflationary pressures that are pushing the Fed toward tightening to ease, even if inflation remains above the 2% target in their new AIT framework. That being said, if inflation fails to cool early next year – perhaps due to persistently high wage inflation a price spiral or a geopolitical shock that pushes energy commodities still higher – we are ready and willing to adapt to this new context. In the meantime, we await more clarity on the threat of the omicron variant or further position clearing to re-engage risk, as the de-pricing of rate hikes would prove to be broadly supportive to markets next year.

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster declined slightly, largely due to slowing momentum in the Eurozone.

- Our World Inflation Nowcaster moved slightly lower as inflationary pressures in China eased modestly.

- Our Market Stress Nowcaster remained stable in elevated territory last week.

Sources: Unigestion, Bloomberg, as of 3 December 2021.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).