Two weeks into the new year, global equities have continued their upward trajectory. The signing of the “phase one” trade deal between the US and China buoyed markets further, even though it was largely expected and contains provisions China may have difficulty achieving. The strength of the move over the last few months has some remembering January 2018 and wondering if the rally still has legs or whether markets are gearing up for another meltdown. These are important questions for investors to assess as now is no time to be complacent. From our perspective, the parallels to early 2018 are fairly weak at this point and conditions point to more upside potential. Nonetheless, we remain vigilant as market rallies such as these often sow the seeds of their own reversals.Too early to call it quits on equities

Remember Me

What’s Next?

In total return terms, the MSCI All Country index is up 2.5% on the year, as both developed world equities (+2.5%) and emerging market equities (+2.9%) benefit from bullish investor sentiment. US equities have continued to outshine, with the S&P 500 up 3.1% and Nasdaq 100 rising by 5.1%. Growth-oriented assets got a further boost when President Trump and Vice Premier Liu signed the “phase one” trade deal between the US and China, a move widely expected by market participants though by no means guaranteed. Among the provisions in the deal, China agreed to purchase an additional USD 200bn of US goods and services over the next two years, more than double their total purchases of USD 186bn in 2017 before the start of the trade war. While some tariffs were rolled back or eliminated, the US will continue to levy a 25% tariff on USD 250bn of Chinese imports, no doubt a bargaining chip for future negotiations. Continued progress and a potential “phase two” deal will depend heavily on the Chinese following through on their commitments to increase US imports as well as protect intellectual property.

Are we back to 2018? Not yet.

With this upside trigger behind us, some investors are naturally taking stock and feeling a sense of déjà vu: a fourth-quarter rally capping off stellar yearly performance and extending into January with bullish consensus sentiment in spite of an ageing expansion. From our perspective, there were a handful of worrisome signals ahead of the February 2018 sell-off:

- From a macro perspective, above-trend growth was leading to inflationary pressures and pushing central bankers toward monetary policy normalisation;

- Despite the equity rally, the VIX index was rising, especially during the second half of January, and TED spreads were widening, leading our market stress Nowcaster to flash warnings signs that financial market conditions were a risk;

- The momentum of the market rally was especially strong, with S&P 500 returns in the top percentiles over various look-back windows;

- Investor positioning was strongly bullish, with levered strategies exhibiting high beta to global equities, retail investors positioning extremely short volatility through ETFs, and speculators net short US 10-year Treasury futures; and

- Valuations were stretched, with the MSCI All Country index reaching its 85th percentile and the S&P 500 at its 90th percentile, as measured by a broad cross-section of valuation metrics.

These conditions led us to reduce our portfolio’s risk and exposure to equities at the end of January. Today, outside of valuations and elevated but stable TED spreads, many of these signals are not flashing: central banks show no signs of tightening after the Fed cut three times last year versus three hikes in the 12 months preceding February 2018. Moreover, the VIX is down to 12 from 14 at the end of 2019, the equity rally has been strong but has not breached our reversal threshold, and investor positioning does not seem overly exposed.

Within this context, investors will likely focus their attention in the short-term on the upcoming earnings season, which will unfold over the next few weeks. Muted expectations for Q4 2019 earnings, based on revenue contraction and lacklustre margins, is fertile ground for positive surprises and higher equity prices. If corporates are able to capitalise on waning trade war risk – i.e. margin recovery for US firms as peak tariffs are behind them, and a pickup in global trade for European firms – investors will have good reason to reassess their expectations to the upside. We will also be looking closely for signs of a pickup in capex, as fading uncertainty may incentivise firms to deploy cash for investments instead of shareholder payouts. A strong pickup in capex would provide a boost to the global economy, reinforcing some of the positive growth momentum we have observed recently. We therefore remain positive on equities, hedging this view by an underweight in credit, where extreme valuations and positioning suggest downside risk. We are also closely watching out for political risk in the US. The emergence of a progressive Democratic presidential nominee (i.e., Bernie Sanders or Elizabeth Warren) would present a significant challenge to US equity prices as investors reassess their expectations for US corporate profitability. Finally, we are monitoring central banks for any change in rhetoric, as more hawkish monetary policy guidance would certainly remind us of January 2018.Upcoming earnings season could lead to further upside

Unigestion Nowcasting

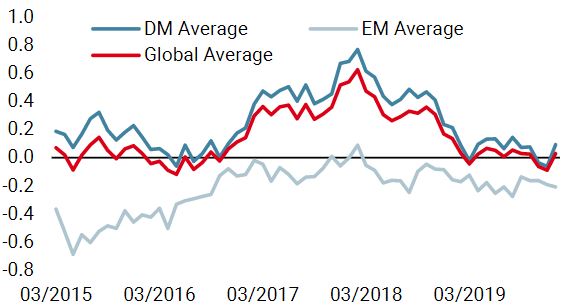

World Growth Nowcaster

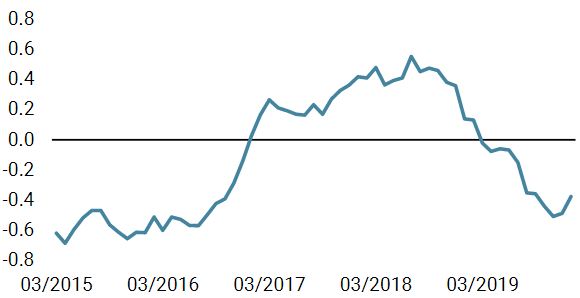

World Inflation Nowcaster

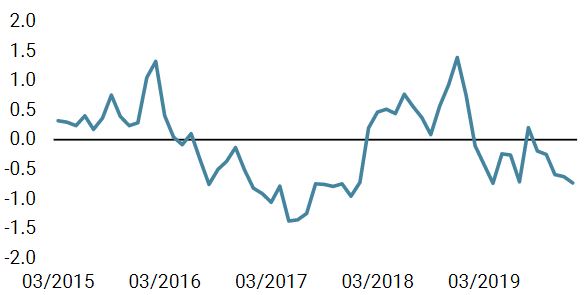

Market Stress Nowcaster

Weekly Change

- Our world Growth Nowcaster is giving a more positive signal, with the US economy showing resilience and over 50% of global data showing improvements.

- Our world Inflation Nowcaster increased last week, largely driven by higher input and supply-side inflation.

- Market stress was steady at low levels over the week.

Sources: Unigestion. Bloomberg, as of 20 January 2020.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore (MAS). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).