Transition Phase

The month of May ended in such a way, that a casual observer looking at final performance numbers would find it hard to believe just how volatile and uncertain it actually was. The end-of-month recovery contrasted with an earlier correction that sent some markets to year-to-date lows (or highs). Behind these erratic moves, the same key factors continue to evolve rapidly: Surging inflation, deteriorating growth, Covid lockdowns in Asia, the war in Ukraine, and central bank hawkishness. However, as often in financial markets, good or bad news can be interpreted in different ways, and investor sentiment can shift in a matter of days, as was the case last month. Let us take a look at the various driving forces that moved markets in the past few weeks.

Waiting on the World To Change

What’s Next

Macro: Lower Growth and Toppish Inflation

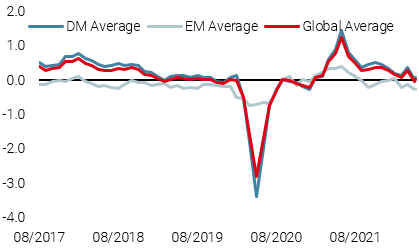

High inflation, lower growth, and tighter financial conditions are the key takeaways from May, and this is not a good omen to say the least. Our proprietary Nowcasters, through the aggregation of hundreds of macro data, have sent an unequivocal signal: economic momentum has faltered across the globe to such an extent that the risk of recession is now on top of everyone’s mind, from investors to politicians, central bankers and most importantly, households.

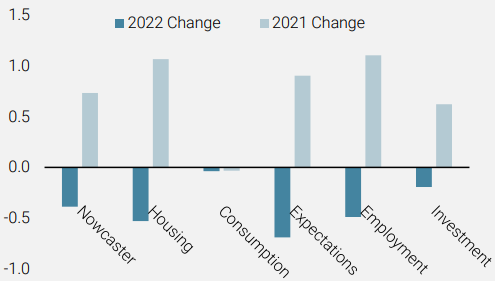

Even more striking is the global nature of the slowdown, as all GDP components are trending lower in 2022, with the exception of consumption, so far more resilient, at the expense of savings. In our opinion, the triggers behind such a rapid and continuous downturn in growth dynamics are numerous, but the greatest impact seems to be coming from tighter fiscal and monetary conditions on the one hand, and from inflation’s effect on demand on the other hand.

Higher input prices are damaging corporate profitability, forcing companies to reduce investment and capex, while higher final prices are hitting consumers even harder. While the amount of money needed to operate a company or a household keeps on rising, what remains for non-vital consumption and investment is shrinking. This has led to rapidly decreasing GDP numbers, which turned negative in a few countries for the first time since the Covid crisis.

Figure 1: Global Growth Nowcaster component changes

Source: Bloomberg, Unigestion as of 31.05.2022

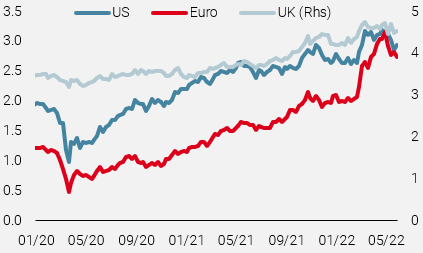

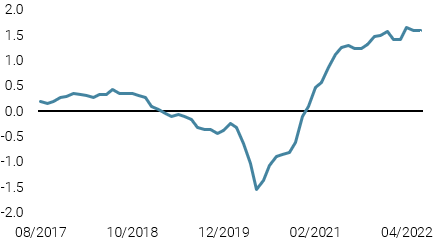

Inflation has shown early signs of plateauing, although it is too early to call it a win. The global rate of increase has been fading, and investors’ long term expectations followed through, as reflected in long term inflation breakevens. As financial markets remain driven by a subtle combination of current conditions and medium term expectations, the inflation situation stays challenging: record high numbers and improving future prospects make it difficult to position oneself properly in this challenging environment, leading to the very fragile and highly volatile price movements that have characterized 2022 so far, with May being no exception. Consequently, the negative implications of the evolution in the growth/inflation duo have pushed the odds of a monetary policy mistake even higher. Central bankers vowed to fight inflation as hard as they possibly can, conscious that their actions will weigh on the shoulders of Main Street. The question is whether they will manage to achieve a soft or a hard landing of the economy, and the divided sentiment on this key question is behind the erratic behaviour shown by the investment community of late. If anything, the combination of tighter fiscal and monetary conditions has historically led to large equity corrections, and it seem to us that recent bouts of optimism can only be short lived for now, as they were based on the wrong assumptions, that lower growth would push central bankers to ease their aggressive path toward monetary contraction.

Figure 2: Inflation breakevens

Source: Bloomberg, Unigestion as of 31.05.2022

Market Action, False Optimism, Buy the Dip and Sell the Rallies

Although global equities posted slightly positive returns in May (MSCI AC +0.12%), this stability hid a volatile month in terms of both the spread between monthly highs and lows and the dispersion across sectors and styles. After touching a new yearly low on May 20th, US equities rebounded sharply following the Fed minutes and recouped their losses. To illustrate the amplitude of intra-month moves, the S&P500 was down more than -6% on a month-to-date basis at its mid-May low, before ending the month in positive territory (+0.2%). Monthly performance dispersion remained large across styles and sectors. The MSCI Energy delivered the best performance in May, up +13.5%, while the Tech sector lagged with another monthly loss of -1.5%. In terms of styles, the difference in monthly performance was more moderate than between sectors. The Value factor outperformed most others styles, with a positive monthly return (+2.2% for MSCI World Value). Overall, US equities lagged the rest of the world in May, while emerging equities outperformed developed ones.

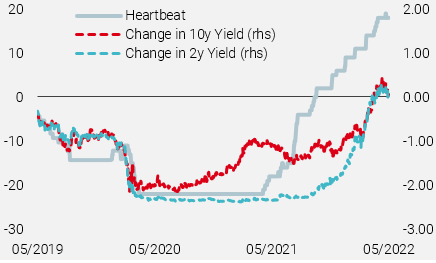

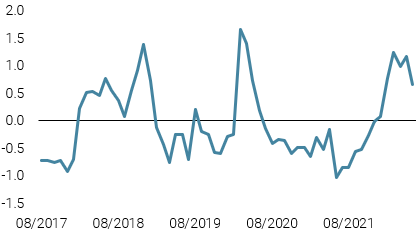

In the credit space, following four consecutive months of widening, US HY credit spreads stabilised at 461 bps, after reaching a new yearly high at 520 mid-May. Dispersion was not limited to growth-oriented assets. In the fixed-income markets, differences in market price action was significant. Lower momentum in the growth dynamic, as illustrated by the sharp decline in our US Growth Nowcaster, pushed US 10yr bond yields lower, from 2.93% to 2.84%, while European bond yields increased by 18 bps, reaching a new high for German 10yr Bunds at 1.12%. This tightening in transatlantic spreads led to a rebound of European currencies, up 1.8% over the month. Overall, the stabilisation in Fed hawkishness, measured through our “heartbeat indicator” that tracks Fed members’ comments and speeches, caused the greenback to weaken across the board last month. Finally, commodities were mixed, as the energy sector benefited from unresolved geopolitical risk and a ban of European countries on Russian oil, while industrial metals declined, following new lockdowns implemented in China.

Figure 3: Fed’s Heartbeat

Source: Bloomberg, Unigestion as of 31.05.2022

Positioning: Sails Down to Face Uncertainty, Remain Selective

After a month of “transition”, marked by reversed rotation in most assets, cautiousness is still key while uncertainty prevails. Current market pricing in risk assets may be deemed complacent, if the economic landing turns out harder than expected, or exaggerated, if growth is to remain positive, around potential.

We still think that inflation is close to the peak (even though stabilisation does not mean that prices will fall and relieve the burden on firms and households) as well as Fed hawkishness, which should deliver what they have telegraphed, but no more than that. These factors, while positive, are still assumptions rather than facts and need to be confirmed before we can become more constructive and redeploy risk more confidently.

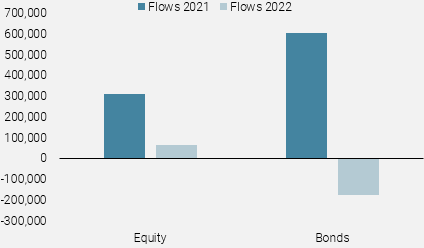

Figure 4: ICI Mutual Fund and ETF Flows

Source: Bloomberg, Unigestion as of 31.05.2022

We believe that risks remain tilted to the downside, mainly due to the inflation induced demand contraction that still needs to bottom. Deleveraging by institutional investors has been large this year, and retail flows are the final missing piece, so far muted but not negative, after a record year of inflows in 2021. The global macro and market context have transited from all negative – which we met in April and May with a defensive stance – to more balanced, leading to a cautious, yet less defensive tactical positioning.

We will be looking for a further stabilisation in central bank rhetoric and/or dislocations between asset prices (to the downside) and growth/inflation paths (to the upside) to deploy a more constructive pro-risk portfolio. This would alter the market dynamic from current bear market rallies and range trading into a true risk-on environment. Patience remains a virtue for now, as it will enable us to seize opportunities as they appear.

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster rose slightly thanks to a modest improvement in the US and China.

- Our World Inflation Nowcaster was steady with most economies continuing to see sustained inflationary pressures.

- Our Market Stress Nowcaster moved lower, primarily driven by an easing in liquidity conditions.

Sources: Unigestion, Bloomberg, as of 07 June 2022.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).