Uni-Global Alternative Risk Premia 2019 Performance Review

2019 was on average a much better year for alternative risk premia strategies relative to 2018, but it was not a year without dispersion amongst our peers. In this paper, we take a deeper dive into the drivers of performance of UniGlobal Alternative Risk Premia in 2019 and since inception, and how it compares to the competition.

Key Takeaways from this Paper:

- Uni-Global Alternative Risk Premia delivered attractive risk-adjusted performance in 2019, outperforming the SG Multi Alternative Risk Premia index.

- Trend following and most carry strategies performed well, as expected in a supportive macroeconomic and sentiment context.

- Dynamic allocation contributed strongly in 2019.

- Since inception, the fund has achieved positive asymmetry in different market conditions, with very low sensitivity to traditional asset classes.

2019 in Review

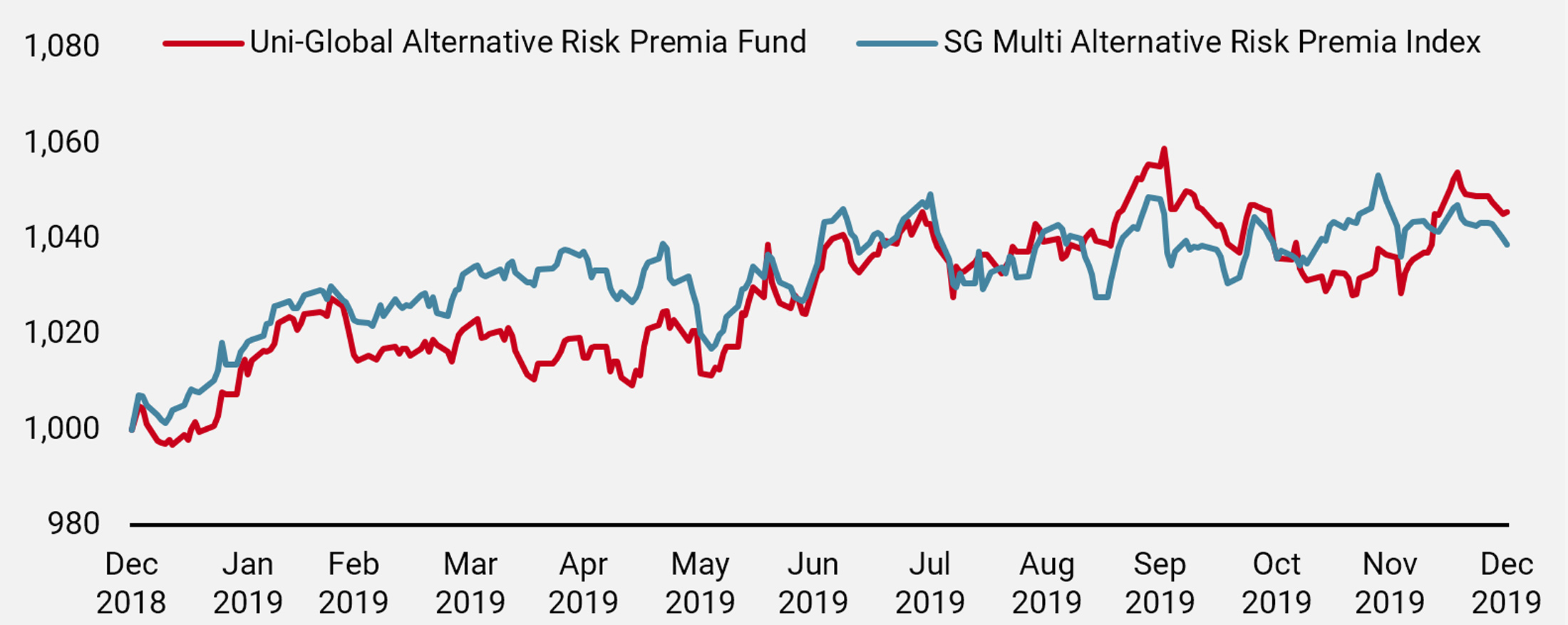

Despite slower global growth, unchanged earnings per share, and a rise in geopolitical uncertainties, 2019 saw the MSCI World Net Total Return index return 27.7% in USD. A key difference this year was a globally coordinated central bank shift to a more stimulative stance that served to push growth assets higher. Against this backdrop, Uni-Global Alternative Risk Premia delivered 4.6% in 2019 (net of fees), outperforming the SG Multi Alternative Risk Premia index, which returned 3.9% over the year (Figure 1). Similarly, Morgan Stanley shows that the average alternative risk premia fund returned 2.4% in 2019. In Kepler’s latest report, eight of the ten “Bottom 10 performing funds” in the “MultiStrategy” category for 2019 were alternative risk premia funds, with returns ranging from 2.4% to -16.5%, highlighting the huge dispersion amongst key players in the market despite a positive year on average.

Figure 1: 2019 Performance vs. SG Multi Alternative Risk Premia Index

Our investment process consists of two main building blocks. The strategic book aims to harvest returns from a broad, diversified universe of alternative risk premia using a macro-risk based framework to provide consistent returns on average across economic regimes. The dynamic book adapts the strategic portfolio to the current macroeconomic, sentiment and valuation environment, in the form of active allocation across risk premia. In addition, the fund applies a risk control overlay to limit portfolio sensitivity to traditional assets.

This kind of portfolio construction provides full diversification: firstly across time horizons (long-term vs. medium-term); and further, across risk dimensions with a close monitoring of macro risks, market sentiment and valuation, the three main drivers of asset returns over the long term.

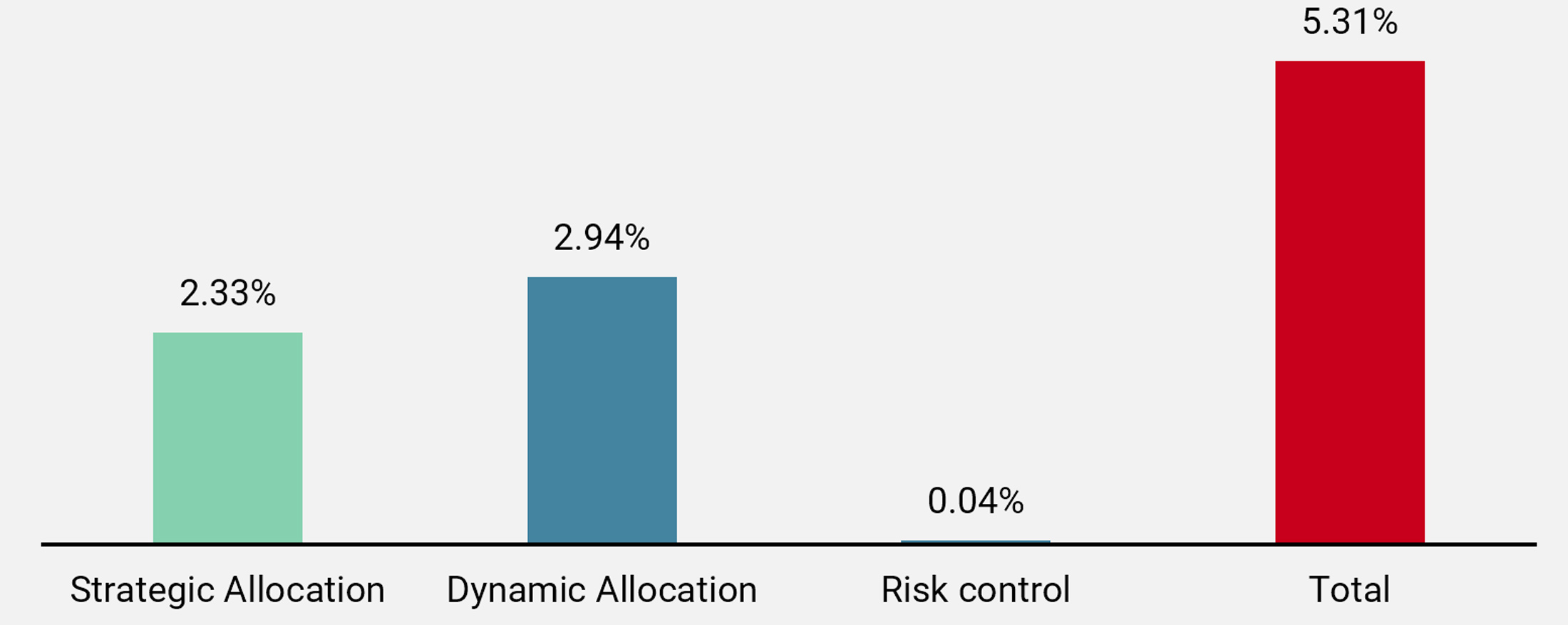

As can be seen below (Figure 2), each component contributed positively to performance in 2019.

Figure 2: 2019 Uni-Global Alternative Risk Premia Fund Performance by Books

The dynamic book performed strongly over the year, contributing positively in nine out of the 12 months.

In August 2019, the MSCI World index lost almost 2%. Heightened market stress risk indicated by our proprietary market stress Nowcaster led us to overweight Trend Following, which had some very long bond positions at the time. This overweight position was beneficial as the risk premia was by far the strongest performer in the month of August. The dynamic book returned 0.5% in the month of August while the strategic book returned -0.11%.

Conversely, in September 2019, our Nowcasters suggested that we were going into a more benign market and macroeconomic environment. This led us to underweight the Trend Following strategy, and overweight the Equity Index Value and FX Carry strategies. The dynamic book contributed another 0.7% in the month of September.

Since inception, the dynamic book has continued to help the portfolio deliver smoother returns with a negative correlation to the strategic book. Indeed, as shown in Figure 3, while the dynamic book has delivered strong risk-adjusted performance since inception, the performance is even more positive when the strategic book is down versus when the strategic book is up.

Figure 3: Dynamic Book Performance Since Inception (13.12.2016)

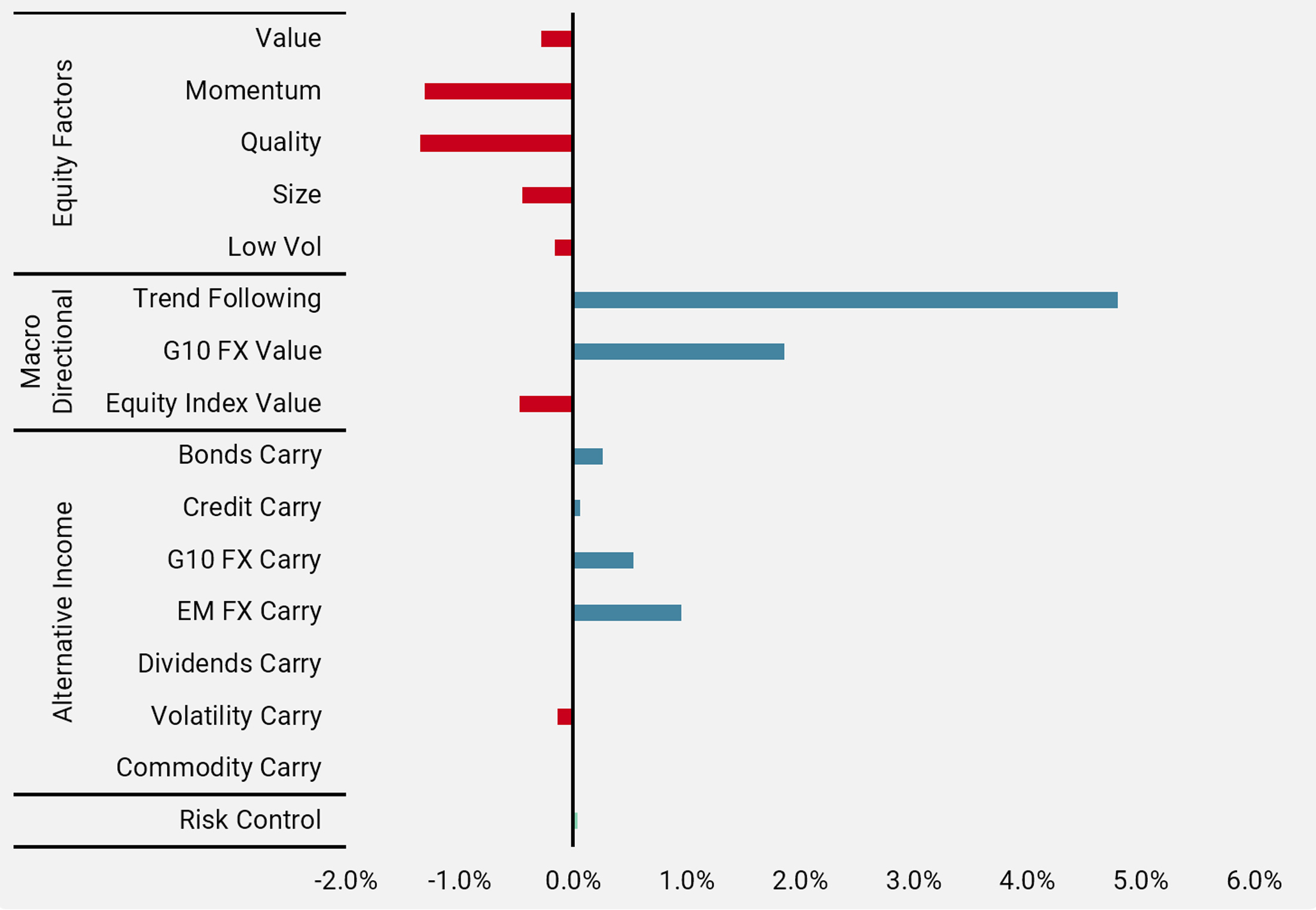

At the risk premia level, the strongest performer was Cross-Asset Trend Following, contributing 4.8% to performance in 2019. This is followed by G10 FX Value which contributed 1.9%. Most alternative income strategies, including Bonds Carry, Credit Carry, G10 and Emerging Markets FX Carry and Dividends Carry also contributed positively. Equity factors suffered to varying magnitudes over this period. For most of 2019, Equity Value continued its downtrend from 2018, but saw a very strong recovery in the last four months of the year. Indeed, the rotation from Equity Momentum to Equity Value over these four months has been quite impressive. Figure 4 shows the performance contributions from each alternative risk premia in 2019.

Figure 4: 2019 Uni-Global Alternative Risk Premia Fund Performance Contributions by Risk Premia

Three-year Fund Anniversary

December 2019 also marks the third anniversary of the Uni-Global Alternative Risk Premia fund. While a low volatility environment means that most alternative risk premia funds have not reached their target volatilities during this period, the Uni-Global Alternative Risk Premia fund has outperformed the average peer tracked by the SG Multi Alternative Risk Premia index on an absolute and risk-adjusted basis. Since-inception fund and index performance results are shown in Figure 5 below.

Figure 5: Risk-adjusted Performance Since Inception (13.12.2016)

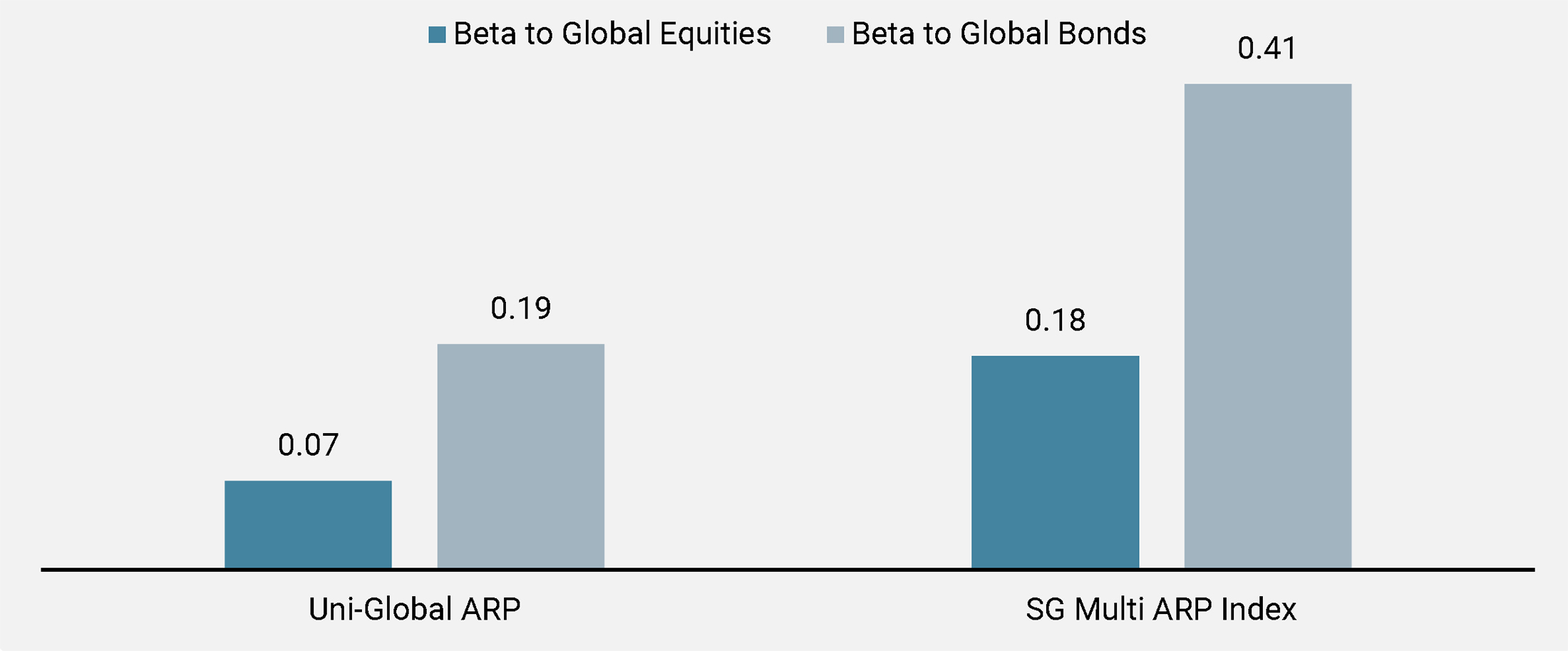

The fund aims to achieve its return objectives with limited sensitivity to traditional assets classes such as equities and bonds. As illustrated in Figure 6, since inception, the fund has achieved a lower sensitivity to global equities and bond markets than the SG Multi Alternative Risk Premia index.

Figure 6: Beta to Global Equities and Global Bonds Since Inception

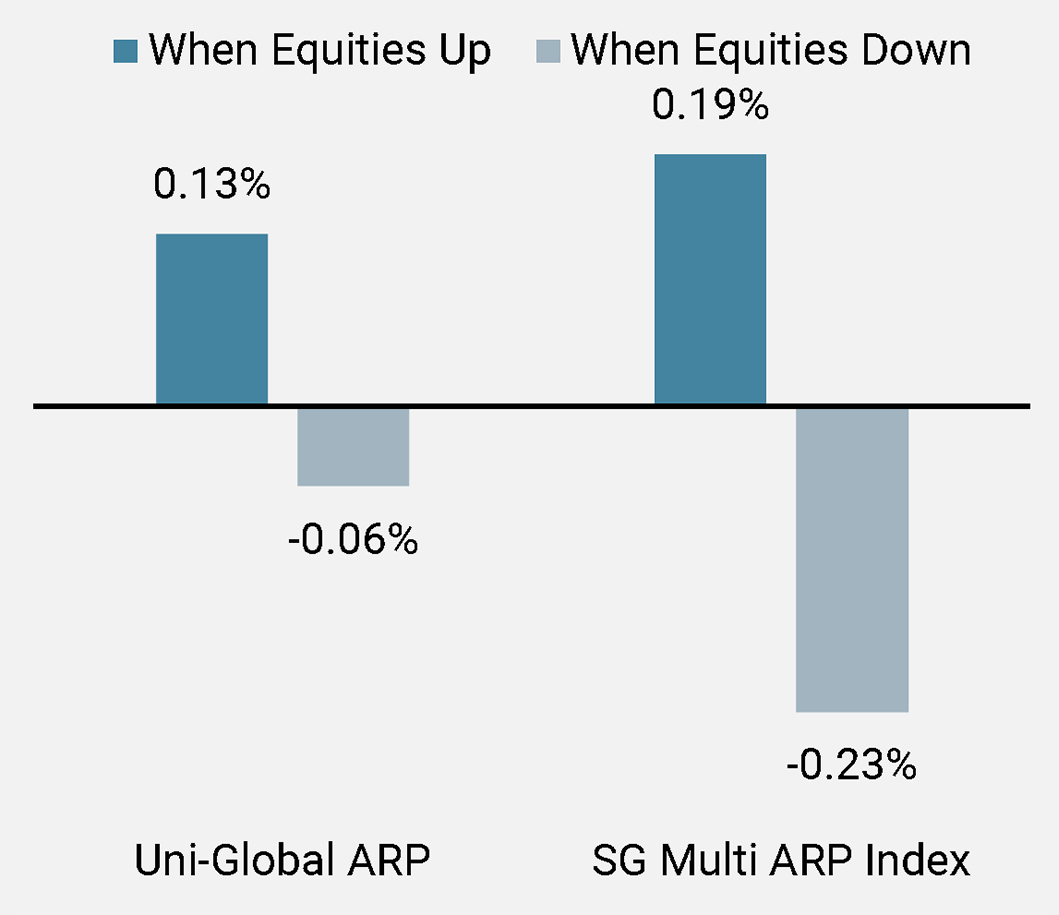

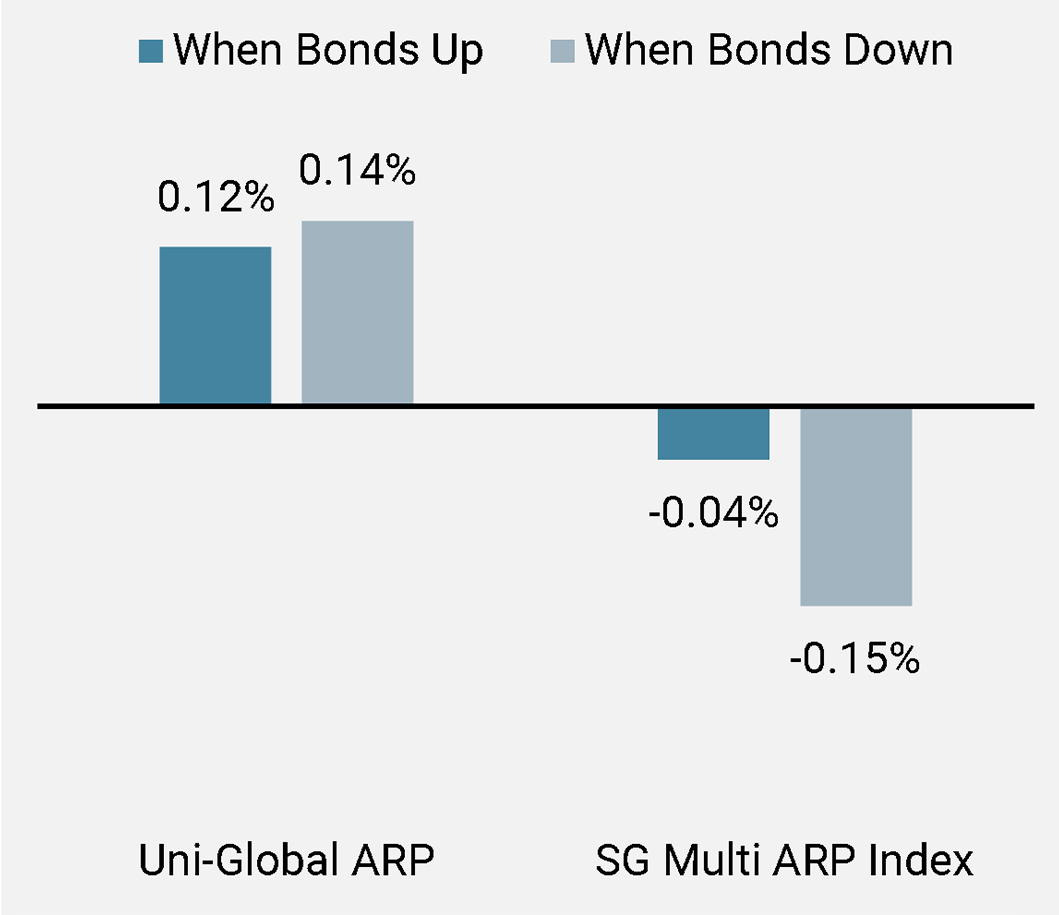

Further, as illustrated by Figures 7a and 7b, the fund has delivered upside-to-downside participation ratios that are greater than one on an absolute basis, and higher than those delivered by the SG Multi Alternative Risk Premia index.

Figure 7a: Performance in Rising and Falling Equity Markets Since Inception

Figure 7b: Performance in Rising and Falling Bond Markets Since Inception

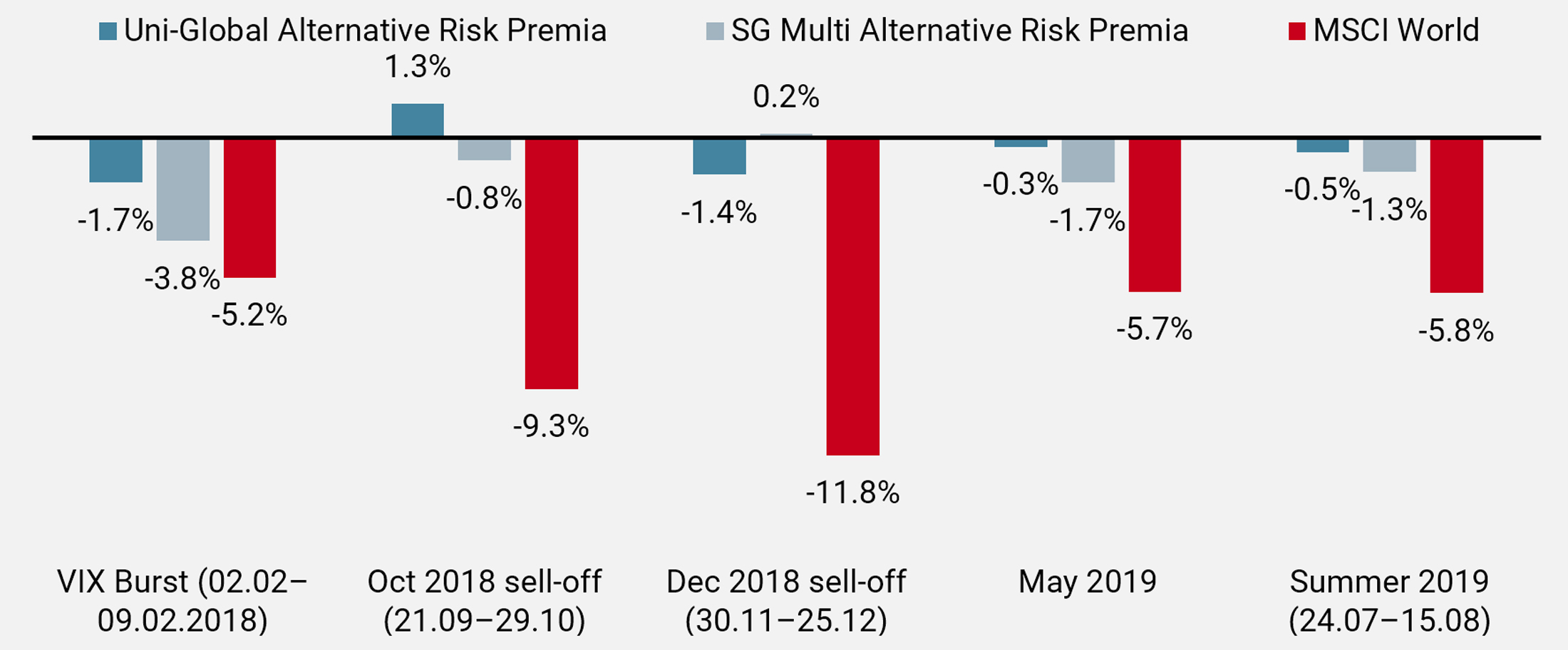

As illustrated by Figure 8, during large equity market downturns since fund inception, the fund suffered limited losses relative to equity markets, and relative to the SG Multi Alternative Risk Premia index over most of these periods.

Figure 8: Fund and Index Performance During Equity Downturns Since Inception

2020 Outlook

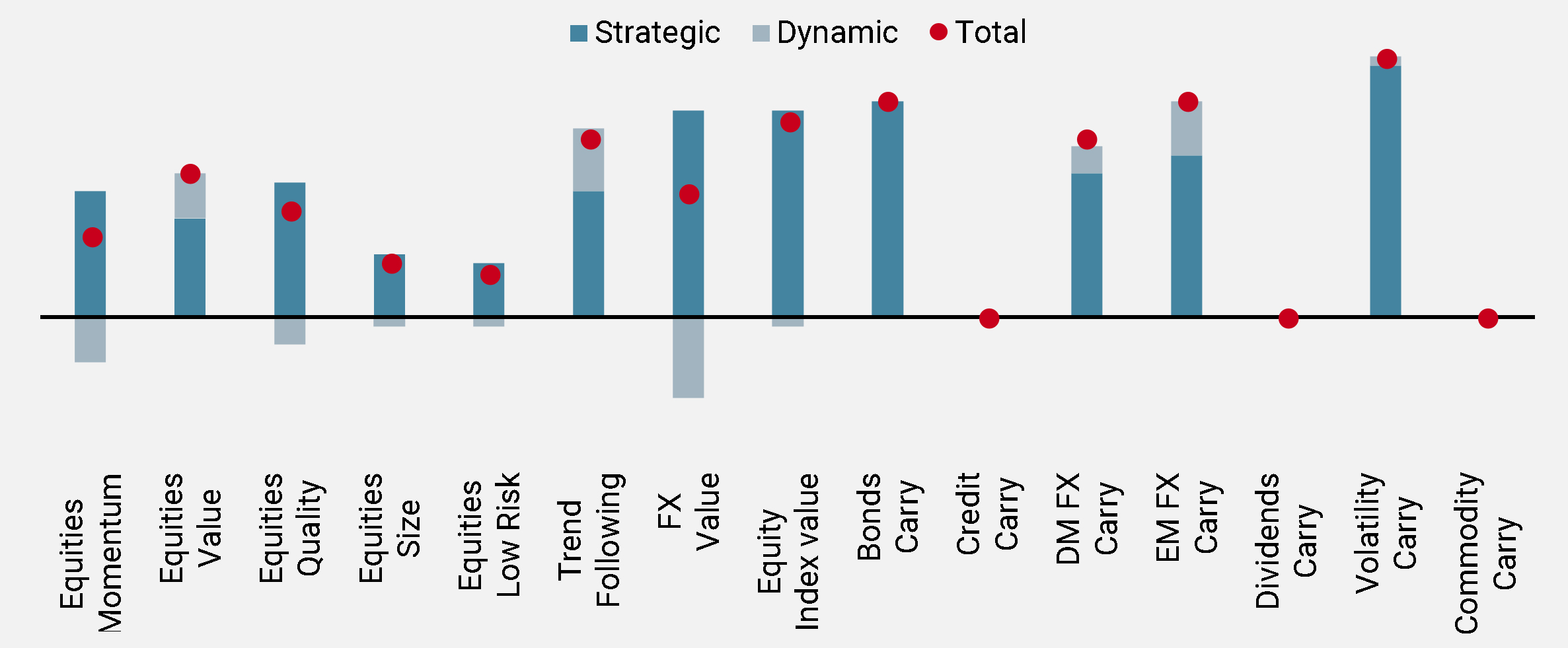

As of 2019 year-end, the fund is positioned with a growth tilt as our proprietary macroeconomic and sentiment Nowcasters suggest low risks of recession, inflation and market stress. Figure 9 illustrates our positioning as of 31 December. Credit, Dividends and Commodity Carry were not allocated due to negative carry.

Figure 9: Growth Tilts for Starting 2020 (Capital Allocation as of 31.12.2019)

We believe that central bank policy is likely to remain supportive in 2020, in light of muted inflation pressures that show no signs of increasing. However, the sustained rally has pushed valuations up to levels that we believe are concerning in some areas. In addition, investors will need to contend with an upcoming US election and an anticipated global slowdown. These factors will likely weigh heavily on investor sentiment. As such, we believe that now is a crucial time to highlight the benefits of a macro risk-based solution that aims to deliver smooth returns in different market conditions.

Read more

Read moreImportant Information

Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed by recipients to any other person. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in the investment vehicles to which it refers. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Please contact your professional adviser/consultant before making an investment decision.

Where possible we aim to disclose the material risks pertinent to this document, and as such these should be noted on the individual document pages. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors.

To the extent that this report contains statements about the future, such statements are forwardlooking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of this information. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission. Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore. Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN). Unigestion SA has an international advisor exemption in Quebec, Saskatchewan and Ontario. Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion SA’s assets are situated outside of Canada and, as such, there may be difficulty enforcing legal rights against Unigestion SA.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission. Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore.

Uni-Global – Alternative Risk Premia is a compartment of the Luxembourg UniGlobal SICAV Part I, UCITS IV compliant. The compartment is currently authorised for distribution in Austria, Belgium, Denmark, Finland, France, Germany, Ireland, Italy, Luxembourg, Netherlands, Norway, Spain, UK, Sweden, Switzerland. In Italy, the compartment can be offered only to qualified investors within the meaning of art.100 D. Leg. 58/1998. The shares may not be offered or distributed in any country where such offer or distribution would be prohibited by law. All investors must obtain and carefully read the relevant prospectus which contains additional information needed to evaluate the potential investment and provides important disclosures regarding risks, fees and expenses. Unless otherwise stated performance is shown net of fees in USD and does not include the commission and fees charged at the time of subscribing for or redeeming shares.

No prospectus has been filed with a Canadian securities regulatory authority to qualify the distribution of units of this fund and no such authority has expressed an opinion about these securities. Accordingly, their units may not be offered or distributed in Canada except to permitted clients who benefit from an exemption from the requirement to deliver a prospectus under securities legislation and where such offer or distribution would be prohibited by law. All investors must obtain and carefully read the applicable offering memorandum which contains additional information needed to evaluate the potential investment and provides important disclosures regarding risks, fees and expenses.