Unintended Consequences Of Higher Commodity Volatility

Surging commodities over the past months have largely contributed to higher inflation expectations and the resulting “normalisation” by the world’s major central banks, now engaged in an aggressive rate hike cycle for 2022 and beyond. Higher commodity volatility has also led to other secondary effects, from depressed market sentiment and lower liquidity across asset classes to a shift from economic to social issues governments are facing in the light of persistently higher inflation. Last but not least, given the increased constraints countries have to contend with in shaping their policy mix, the risk of a policy mistake continues to rise, and by extension the risk of a recession.

Shake, Rattle and Roll

What’s Next?

Commodities VaR shock

Rising commodities in the first quarter not only triggered higher and longer lasting inflation risks but also injected more uncertainty across the board. The higher inflation numbers imply:

- A higher risk of policy mistake with rising fears of recession,

- A larger right tail event on the inflation front with an increasing threat of de-anchoring in long-term inflation expectations.

As a result, the asset risk premium widened considerably, reflecting a jump in both realised and implied volatility. Figure 1, which charts the percentile of current 90-day realised volatility for the main traditional assets classes, illustrates how large and broad the recent rise in the risk premium has been.

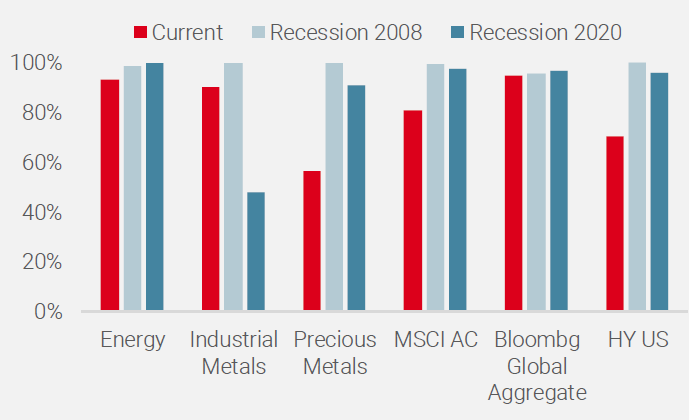

Figure 1: 90-day Realised Volatility (Percentile, 2000-2022)

Source: Bloomberg, Unigestion, as of 22 April 2022

Energy, Industrial Metals and global bonds represented by the Bloomberg Global Aggregate index display a 3-month realised volatility above the 90th percentile. Since 2000, we have seen a similar pattern only on two occasions: following the GFC crisis in January 2009 and during the Covid crisis in July 2020.

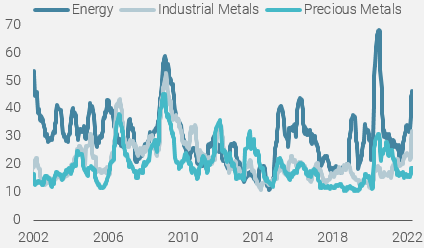

The current situation in the commodities complex is quite unusual. Historically, there is a negative relationship between realised volatility and the change in underlying prices. As shown in Figure 2, which exhibits the historical 90-day realised volatility for the three Bloomberg Commodities sub sectors, the previous spikes in volatility for Energy and Industrial Metals from 2008, 2016 and 2020 were associated with sharp falls in prices. This is not the case today, since both have respectively returned 65.5% and 23.1% since the beginning of the year. We are thus witnessing higher prices with higher volatility, which is an exceptional event.

Figure 2: 90-day Realized Volatility for Commodities Sectors (%)

Source: Bloomberg, Unigestion, as of 22 April 2022

Macro implications

This situation has several implications. On the macroeconomic front, the higher volatility of elements representing more than 50% of inflation for major economies raises the question about the policy mix stance and the higher risk of a policy mistake.

Regarding monetary policy, the stance cannot be clearer, as aggressive tightening is expected from the major central banks over the next 12 months. This normalisation of monetary policy will be implemented through a combination of interest rates tools and balance sheet reduction. This removal of accommodation, never seen before in terms of both scale and timing, leads investors to question the path of the global economy’s “landing” and warrants a cautious stance in the tactical allocations. As an example, market sentiment declined to multi-decade lows (AII % Bulls reading currently at 15.8 vs 21 in March 2020 and 24 in February 2009) and most systematic risk-based strategies trimmed their global exposures, taking the higher risk into account. This rise in assets’ expected shortfall comes from a combination of lower diversification from changes in correlation pairs such as bonds/equity or real rates/gold and weaker liquidity in various markets, which amplifies any moves.

Concerning fiscal policy, higher volatility in food and energy prices implies a shift in the nature of the issue. We believe that for major governments, persistent high inflation changes the problem from an economic to a social one, which could be more challenging to manage ahead of key elections. Indeed, the negative impact of higher consumer and producer prices doesn’t affect household and corporates in the same way. Moreover, within households and corporates, the shock is unevenly distributed, because their sensitivity to price changes and the weight of food and energy in their respective consumption differs significantly, depending on revenues or sectors. Given current debt to GDP ratios in major developed economies, it seems difficult for many administrations to offset this inflationary shock through higher public spending or a massive redistributive fiscal policy.

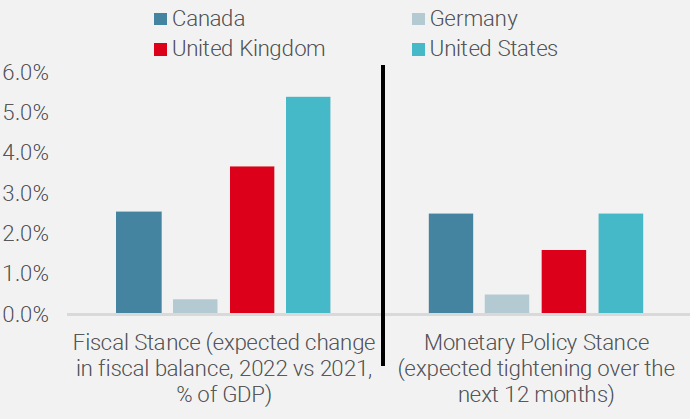

To simply summarise the current macroeconomic situation, higher volatility in commodities strongly limits the effectiveness of a policy mix. Contrary to 2008 and 2020, current constraints in inflation targets and debt sustainability are simply too high as presented in the Figure 3, reflecting how restrictive the policy mix currently is in major countries.

Figure 3: Policy Mix Stance for Major Economies

Source: IMF, Unigestion, as of 22 April 2022

Micro implications

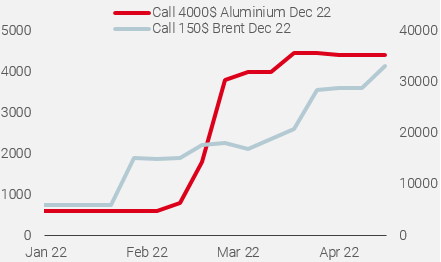

In their recent communications on earnings, some corporates such as VW and JPM mentioned a large impact in their income from spikes in commodities prices (positive for VW and negative for JPM). While neither the German carmaker nor the US bank are producer of commodities, these effects illustrate how the globalised supply chain and its financing have created interdependence across and within sectors. Last week, VW announced “positive fair value measurements on hedging instruments outside hedge accounting have a significant impact on earnings totalling 3.5 billion Euro. A large part of these valuation effects is attributable to commodity hedges and is not cash-effective”. VW, like other major commodities consumers use hedging instruments to shield against volatile price moves on the raw materials they depend on. As an illustration of this trend, open interest on call options for key commodities has recently jumped for out-of-the-money strikes (Figure 4).

Figure 4: OTM Options Open Interest for Brent and Aluminium Dec 2022

Source: Bloomberg, Unigestion, as of 22 April 2022

The second source of concern regarding the jump in realised and implied volatility in the commodities complex is its impact on financial conditions and the intermediation of commodity markets. As recently highlighted by the Dallas Fed1, higher volatility tends to reduce liquidity and then increase the risk of sudden moves in market. Indeed, when prices abruptly increase, firms that rely on bank credit must seek more in order to finance the commodities that they store, ship, trade and/or process. More broadly, the financing needs for global commodities increase significantly as prices surge. Moreover, the recent jump in prices in the Nickel or Natural Gas markets means that trading firms need additional credit to not only finance the goods they purchase, but also the margin they must post. This also creates a higher risk for banks, as they are the main source of credit to commodity trading firms. The Dallas Fed highlights that “there are some reports of banks paring back and being unwilling to increase their exposures to these firms”, increasing the risk of a negative feedback loop, implying lower liquidity and higher volatility. At this stage, the various indicators monitoring systemic risk for the financial sector such as the OIS/Libor spread, Dollar funding cost or Financial CDS do not point to a material risk of disruption in financing the commodities complex. Nevertheless, any negative development on the geopolitical front pushing commodities prices even higher could exacerbate the situation and create a bigger problem than its direct effect on inflation expectations.

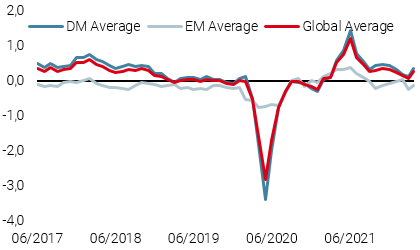

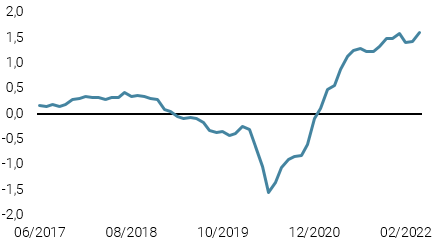

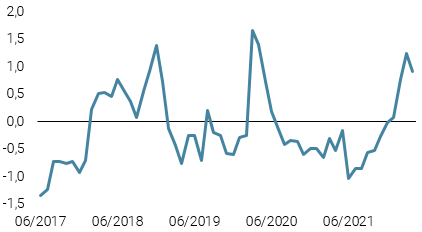

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster was largely unchanged, with most economies seeing stable growth data.

- Our World Inflation Nowcaster was also steady, as nearly all countries continue to see elevated inflation pressures.

- Our Market Stress Nowcaster rose as market volatility picked up.

Sources: Unigestion, Bloomberg, as of 25 April 2022.

1https://www.dallasfed.org/research/economics/2022/0414

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).