The US election proved to be much closer than expected and the prospect of a ‘Blue Wave’ has largely evaporated. While the market may have overestimated Democrats’ chances and the resulting fiscal impulse, the ebbing uncertainty as former Vice President Joe Biden forged a path to victory and the prospect of stable corporate and capital gains tax rates were welcomed by risky markets. Looking ahead, there are key supports for growth-oriented assets, in the US and elsewhere, if the current results hold. The latest unemployment numbers confirm what we have been seeing in our indicators: growth in the US has recovered strongly. Recent positive news on a coronavirus vaccine is encouraging, however we continue to watch the increase in new coronavirus cases, especially in the US.

Born in the U.S.A.

What’s Next?

Policy impacts of a Biden presidency and split Congress

While expectations had built for a Democratic ‘Blue Wave’ that would bring Biden to the presidency, flip the Senate, and provide Democrats with a mandate for major reforms, the US election last week turned into a nail-biter. Biden crossed the 270 electoral vote threshold on Saturday after his lead in Pennsylvania was firmly established. Control of the Senate however remains undecided as two races in Georgia will be decided during a January run-off. However, Republicans will likely have at least 50 seats, with the Georgia run-offs giving them a good chance of holding onto their majority.

The policy impact of the likely result – a Biden presidency with a split Congress – may be a fairly positive one for markets. Without a majority in the Senate, key Democratic policies such as rollbacks in corporate and capital gains tax rates are highly unlikely. Health care reform or other major spending measures like a Green New Deal will also likely lack sufficient support in the new Congress. A major fiscal stimulus, such as the USD 2tn measure that Democrats already passed in the House of Representatives, also seems unlikely, though Senate Republicans seem open to a smaller stimulus (in the USD 1tn range) sometime this year. Overall, we do not expect major domestic policy changes, absent a coronavirus-induced double-dip of the US economy.

At the same time, foreign policy seems likely to be supportive for financial markets. While Democrats share some of the same protectionist viewpoints as the Trump administration, we expect trade policy to normalise, if not return to its pre-Trump form. Thus, although the trade war (specifically with China) may not be over, we expect it to ease. This should help support global trade and corporate earnings growth. Moreover, we do not expect trade policy to be the headline risk it has posed previously, where a tweet could throw markets into disarray. This should provide a less volatile context for markets overall and perhaps remove some of reticence on the part of investors to take on risk.

A favourable context for the medium term

Overall, the US election looks to be a fairly positive result for markets over the medium term in our view. We were concerned that the market was overly optimistic on a Blue Wave-induced stimulus, and thus could be disappointed by a split result. However, the market action thus far suggests the outcome is still regarded as quite favourable. In addition to equities rallying strongly, the yield on the US 10-year bond fell below its pre-election peak as investors priced out the large stimulus. The fading uncertainty was vivid in the VIX index, which fell 35% from its pre-election level of 38 to 25 on Friday, before Biden was declared president-elect. The current context – stable yields, lower geopolitical uncertainty, and upward pressure on earnings – is a healthy one for putting on broad risk. Emerging market (EM) assets should be well-supported thanks to a more normalised trade policy as well as a lower US dollar due to ebbing uncertainty. Indeed, since 3 November, the US dollar has fallen 2.5% against a broad basket of EM currencies. This should continue to support inflows into EM debt and equities.

The recovery of the US economy also bodes well for the broader global growth context. Both our US Growth Nowcaster and Newscaster have pointed to a strong and so far persistent recovery in the US, despite consumption (both durable and non-durable) remaining constrained. The jobs report on Friday was one more supportive data point, with the unemployment rate falling to 6.9% versus a consensus expectation of 7.6%. Non-farm payrolls added 638,000 new jobs versus an expectation of 580,000. Importantly, the largest contributors were in the accommodation and food services industries while retail trade was the third largest contributor, a reversal of the post-COVID trends. Moreover, 70% of sectors created jobs in October (and even more if you exclude the counter-cyclical public sector, which saw the largest job destruction), indicating the breadth of the recovery in employment. This job growth should feed into consumption as households start to feel they are on solid footing again.

Coronavirus cases rising strongly though vaccine prospects are encouraging

Over the short-term, however, the picture is less rosy due to the continuing surge in coronavirus cases. Many European countries are now seeing the number of new cases dwarf their March/April peaks and the numbers of deaths continue to climb to previous highs as well. Restrictions there have been enacted, and the next few weeks will be critical to assessing if more stringent measures will be necessary. The US has also entered a third period of rising cases, with the 7-day moving average of new cases growing by 25% on Friday. So far, the largest contributors to the growth in new cases are states such as Illinois, Minnesota, Michigan, and Ohio, which together account for about 12% of US GDP. But Texas (9% of US GDP) is seeing new cases grow by 15% and California (15% of US GDP) has seen cases rise by 20%. The trends are worrisome, which is why we are monitoring the situation closely. The recent news on the efficacy of a vaccine is encouraging, and the market reaction has been swift. Combined with the post-election moves, investors have already started to meaningfully price-in the medium-term supports. However, investor disappointment, either due to an impasse on further stimulus or a setback to a vaccine rollout while cases continue to surge, could expose fragilities in the market.

Unigestion Nowcasting

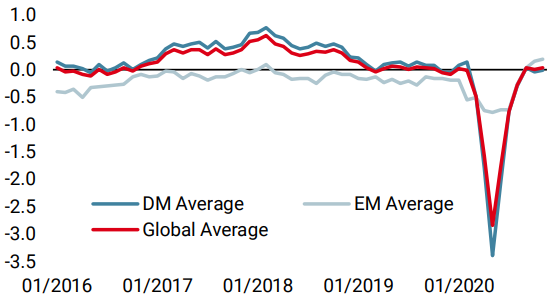

World Growth Nowcaster

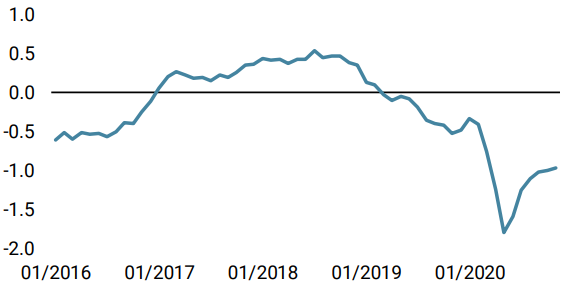

World Inflation Nowcaster

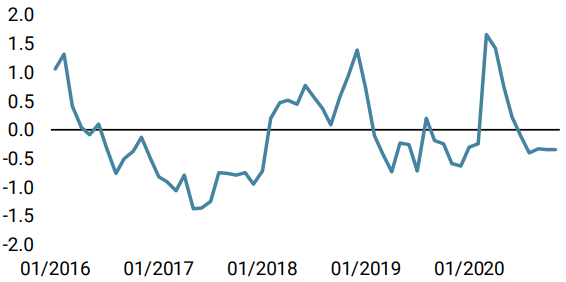

Market Stress Nowcaster

Weekly Change

- Our World Growth Nowcaster decreased last week, mainly due to softer readings in the US and Japan. The economic data has however been improving in Europe broadly.

- Our World Inflation Nowcaster decreased also, mainly as European data took a plunge. Overall, inflation risk is not significant for now.

- Last week, our Market Stress Nowcaster decreased, as volatility dropped and credit spreads contracted.

Sources: Unigestion. Bloomberg, as of 6 November 2020.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore (MAS). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).