Once again, a sustained increase in volatility failed to materialise in 2019 despite heightened geopolitical risk (Brexit, trade wars, Hong Kong, Iran, Latam). These well-flagged events do not seem to scare the market anymore: investors are slowly growing more accustomed to the constant presence of these risks and react to them in a less emotional way. We believe that the bigger risk is coming from central banks and the explicit (directly selling optionality) and implicit (replicating the exposure of a portfolio that is short optionality) carry trade they have kick-started. Central banks have been, and remain, the key driver of cross-asset volatility. We enjoyed a “free central bank put” for some years and there is a risk than investors are becoming complacent. Will central banks save financial markets again…or is the free option losing its convexity?Volatility: a confidence game

Confidence Trick, Culture Club, 1999

Confidence Trick

Volatility trading provides exposure to human insecurity regarding an unknowable future. A short volatility trade expresses confidence in the current market environment, whereas a long volatility position is a way to express fear that change is coming. Since Draghi’s “whatever it takes” speech in July 2012, the average yearly VIX level has ranged between 11.1 to 17.9, whereas the yearly average since records began in 1990 is 19.3. These numbers clearly reflect investor conviction that central banks can defend the status quo. If we look at the volatility of volatility, which represents the uncertainty of moving from the status quo to a period of change, we see a very different picture. The volatility of VIX has moved steadily higher since 2012, reaching higher levels in August 2015 and February 2018 than during the GFC. Hedging has fallen out of favour, but we do not think that investors are suffering from real “hedging fatigue” yet. Although the long volatility trade has been painful for an extended time, the steep volatility term structure (short-term vs long-term), the rich volatility skew (downside vs upside strikes) and expensive volatility of volatility (VVIX) in the equity space indicate that volatility traders have not become complacent yet. Long volatility trades have faced two challenges recently. First, phases of high volatility have been very infrequent since the GFC. Second, volatility spikes have been very short-lived. The VIX future has traded one day above 30 and 22 days above 25 since July 2012. The aggressive buy-the-dip mentality and accordingly, the fast volatility mean reversion, have been very painful for portfolio hedges. Investors seem to have understood that if they do not monetise their hedges right away, the window of opportunity is gone. This behaviour accelerated the phenomena even more. In order to move into a higher volatility environment, we need an elevated “fear factor” to replace the “greed factor”. The main driver of greed has been yield starvation, and low volatility in financial markets and in macro data. Selling volatility is nothing more than an alternative form of yield – and low realised volatility makes this “yield” look very attractive. It creates an illusion that markets are safer than they are and a dangerous feedback loop. Lower volatility begets lower volatility, rewarding strategies that systematically bet on market stability so they can make even bigger bets on that stability (Risk parity, Var Control, CTA, VIX ETN’s etc.). Before the February 2018 “Volmageddon”, the S&P 500 went for the longest period in history without a 5% dip (405 trading days). The longer this period went on, the more confident investors became and the more crowded the positions got. The consensus view that central banks have defeated volatility was mistaken. They tamed volatility for some time but by doing that, they have increased the tail risks and the likelihood of future market fragility. The second volatility spike in 2018 followed as the market began to feel the discomfort of Fed normalisation. Even though Powell refused to protect the markets initially, the pain of higher interest rates coupled with increasing market stress in Q4 was too high and finally drove the Fed to make a U-turn in January. Once central banks were back in easing mode, credit spreads tightened and equities rallied despite corporate earnings estimates from analysts falling almost every week this year. This anomaly strongly resembles the previous QE era of 2012-2016. Unlike equities, lower-rated segments in credit markets are starting to show some signs of distress. A strong sign is the performance differential within the high yield credit market where the riskiest portion has heavily underperformed higher quality papers despite a very positive year for risky assets. Understanding the credit cycle and its interdependency with central bank action is key for timing volatility trades. This is not only because it was a leading indicator for the last two recessions where high yield spreads started to widen while equity indices kept on making new highs, but also because volatility regime shifts are driven by the credit cycle. When credit is easily available and rates are low, volatility remains suppressed, but as credit contracts, volatility rises.What’s Next?

Are investors complacent?

Starving the market for yield creates crowding and increases market fragility

Liquidity drives markets

This year, even though cross-asset volatility feels very compressed, rates, equities and commodity volatility (but not FX volatility) have traded higher than 2018 despite global central banks cutting rates 68 times. We do not see this as evidence that central banks’ ability to control risk is fading (yet). As long as investors believe in the narrative surrounding the “central bank put”, it will be self-fulfilling. Even though we do not consider the Fed’s latest purchase programme as QE4, it is integral to the promotion of easy financial conditions and it undermines central bank willingness to do “whatever it takes”. Therefore, we are convinced that the combination of supportive central banks, high valuations in traditional asset classes and yield starvation offers a great environment for harvesting the volatility premium. The volatility premium is simply the compensation that investors earn for providing protection against unexpected market volatility. The spread between implied and realised volatility has deteriorated together with the other yield proxies, but it still provides a decent and sustainable return solely driven by investors’ risk aversion and their tendency to overestimate the probability of significant losses. Three things are key to successfully playing the volatility carry trade. First, be aware of the fragility of the markets and their tail risks (implementation). Second, measure and understand the positioning in implicit and explicit short volatility strategies (crowding). Lastly, assess the risk of changes in central bank stance and the stability of the credit market (confidence). Investors still have faith in the central bank narrative and therefore the volatility carry trade will keep on adding value in a portfolio as an uncorrelated, stable and profitable income stream.The central bank narrative will keep on distorting financial markets

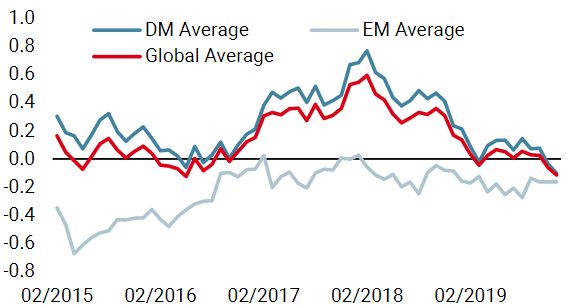

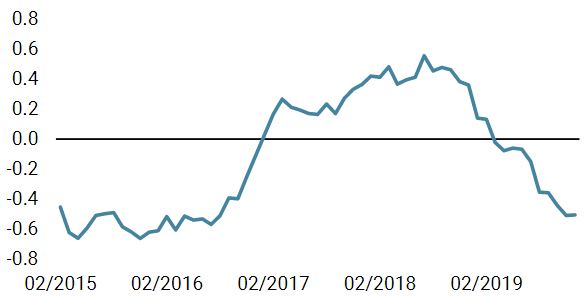

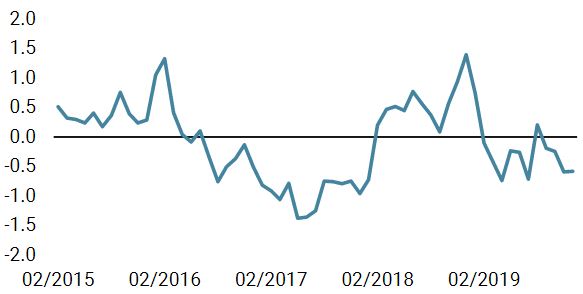

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Our world Growth Nowcaster declined last week. 45% of the data is improving with 43% in the developed world. Growth stabilisation remains on the cards but this is a new negative signal.

- Our world Inflation Nowcaster stabilised last week and inflation risk remains very low.

- Market stress remained stable last week: market stress risk is low.

Sources: Unigestion. Bloomberg, as of 09 December 2019.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore (MAS). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).